Car insurance sounds like a safety net that never budges and most South Africans trust their coverage to be there when it matters. Surprising, right? More than 15 percent of car insurance policies are cancelled each year, and not always because the customer wants out. The real shock is your insurer can show you the door for reasons you might never see coming and even a missed payment or a small white lie could leave you uninsured when you least expect it.

Table of Contents

- When And Why Car Insurance Can Be Cancelled

- How To Cancel Your Vehicle Insurance Properly

- What Happens After Your Insurance Is Cancelled

- Tips To Avoid Car Insurance Cancellation Issues

Quick Summary

| Takeaway | Explanation |

|---|---|

| Understand involuntary cancellation reasons | Familiarize yourself with triggers like non-payment, fraud, and risky behavior to protect your policy. |

| Follow clear cancellation procedures | Ensure you provide written notice and confirm cancellation with your insurance provider to avoid lapses. |

| Recognize post-cancellation consequences | Be aware of potential higher premiums and legal penalties for driving without insurance coverage. |

| Maintain proactive financial management | Set up automatic payments and keep a financial buffer to ensure timely premium payments. |

| Regularly review your insurance policy | Conduct annual reviews and communicate changes with your insurer to prevent unintentional cancellations. |

When and Why Car Insurance Can Be Cancelled

Car insurance cancellation is a complex process that can catch many vehicle owners off guard. While most people assume their insurance coverage is permanent, there are several critical scenarios where an insurer might terminate a policy. Understanding these potential reasons can help you protect your coverage and avoid unexpected financial risks.

To help you quickly compare reasons for car insurance cancellation, here is a summary table outlining both involuntary and voluntary triggers discussed above.

| Type of Cancellation | Specific Reasons |

|---|---|

| Involuntary | – Fraudulent activities (false info, misleading claims) |

- Non-payment of premiums

- High risk behaviour (traffic violations, at-fault accidents)

- Vehicle modifications without notification |

| Voluntary | – Switching providers - Selling the vehicle

- No longer needing coverage |

Reasons for Involuntary Policy Cancellation

Insurers may cancel your car insurance policy for various significant reasons. Fraudulent activities top the list of immediate cancellation triggers. This includes providing false information on your initial application, making misleading claims, or attempting to manipulate the insurance system. According to insurance regulatory reports, deliberate misrepresentation can result in immediate policy termination.

Other critical grounds for involuntary cancellation include:

-

Non Payment: Consistent failure to pay premiums creates significant risk for insurers. Most companies provide a grace period, but prolonged non-payment will trigger automatic cancellation.

-

High Risk Behavior: Accumulating multiple traffic violations, at-fault accidents, or demonstrating consistently dangerous driving patterns can prompt insurers to cancel coverage.

-

Vehicle Modifications: Substantial changes to your vehicle that increase risk without proper notification can lead to policy termination.

Voluntary Cancellation Options

Policyholders also possess the right to voluntarily cancel their car insurance. This might occur when switching providers, selling a vehicle, or no longer requiring coverage. However, strategic timing and understanding potential consequences are crucial. Our guide on policy transitions can help you navigate these complex decisions.

When considering voluntary cancellation, car owners should carefully evaluate:

- Potential financial penalties

- Gaps in continuous coverage

- Implications for future insurance rates

- Contractual obligations with current provider

It is essential to provide formal written notice to your insurance company and follow their specific cancellation procedures. Unexpected lapses in coverage can result in legal complications and potential financial exposure.

Understanding the nuanced landscape of car insurance cancellation requires proactive communication with your insurer. Always review your policy documents, maintain transparent communication, and address any potential issues promptly to prevent unexpected termination of your vehicle coverage.

Remember that each insurance provider has unique policies and procedures. What might trigger cancellation with one company could be handled differently by another. Staying informed and maintaining a clean driving and payment record remains the most effective strategy for maintaining continuous car insurance protection.

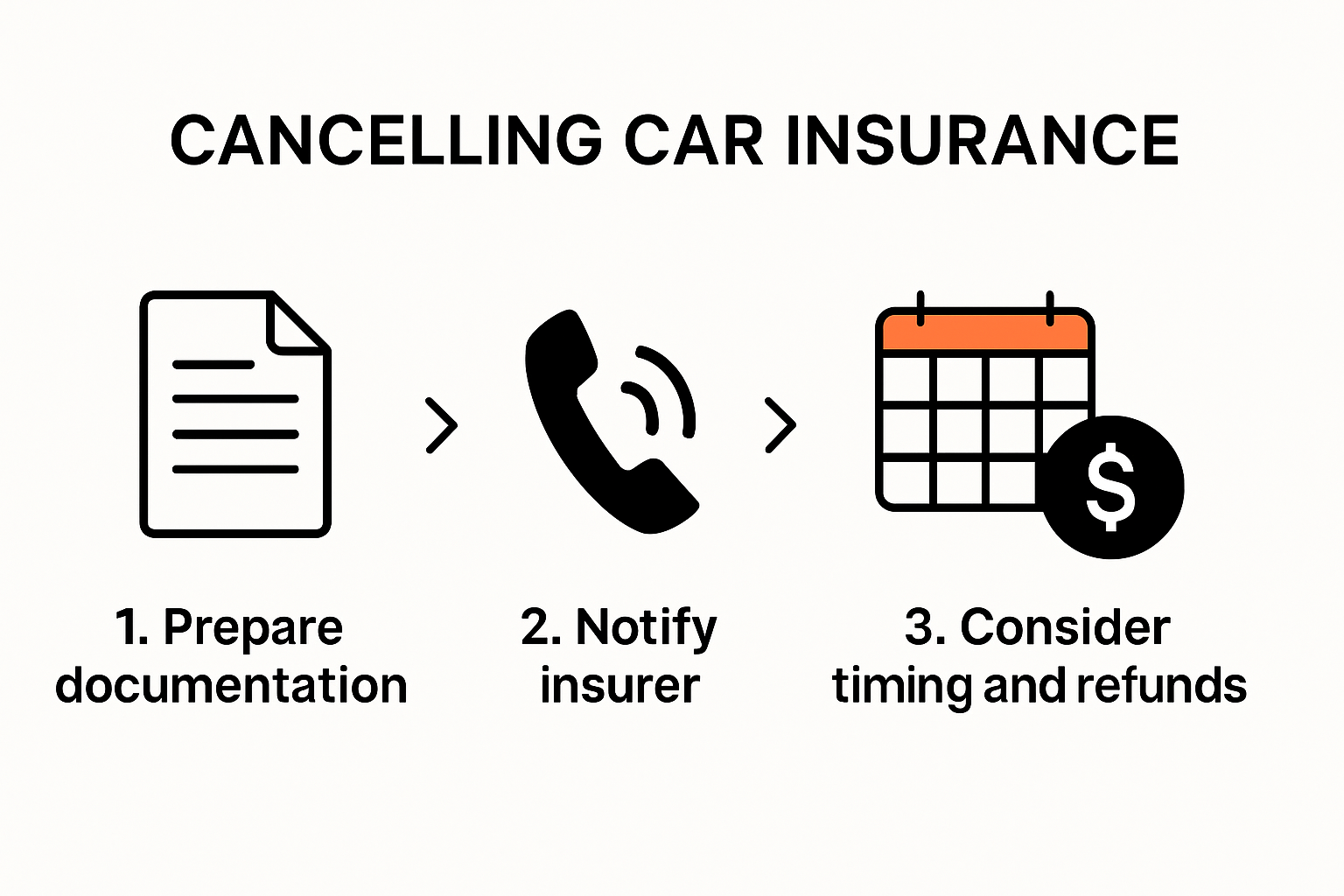

How to Cancel Your Vehicle Insurance Properly

Canceling vehicle insurance requires careful planning and strategic execution to avoid potential financial and legal complications. While the process might seem straightforward, there are several critical steps and considerations that car owners must understand to ensure a smooth transition between insurance providers or policy termination.

Preparing for Insurance Policy Cancellation

Before initiating the cancellation process, car owners must gather essential documentation and information. The National Association of Insurance Commissioners recommends preparing the following items:

-

Current Policy Details: Collect your existing insurance policy number, effective dates, and contact information for your current insurer.

-

New Insurance Documentation: If switching providers, have your new policy documentation ready to ensure continuous coverage.

-

Vehicle Registration: Prepare your vehicle registration documents to verify ownership and provide necessary details during the cancellation process.

Understanding the timing of cancellation is crucial. Most insurance providers require written notice, and cancellations typically become effective on a specific date. Consumers should aim to coordinate the end of one policy with the start of another to prevent potential gaps in coverage.

Executing the Cancellation Process

The cancellation process involves several precise steps to protect your interests. Contact your insurance provider directly through official channels such as their customer service line or written communication. When canceling, be prepared to:

- Provide specific cancellation instructions

- Request written confirmation of the cancellation

- Understand any potential refund or penalty processes

Our guide on switching insurers can help you navigate this complex transition smoothly. Insurance experts recommend maintaining documentation of all communications and ensuring you receive official confirmation of policy termination.

It is essential to time your cancellation strategically. Canceling mid-policy might result in financial penalties or pro-rated refunds. Some insurers charge cancellation fees, which can offset potential savings from switching providers. Carefully review your current policy’s terms and conditions to understand the financial implications.

Additionally, inform your vehicle financing institution if applicable, as they may have specific requirements or preferences regarding insurance coverage. Some financial agreements mandate continuous comprehensive insurance, so coordination is crucial.

After cancellation, request a formal cancellation letter for your records. This document serves as proof of intentional policy termination and can be valuable if disputes arise in the future. Keep this documentation safely stored with your other important vehicle and insurance records.

The cancellation process can seem daunting, so here is a step-by-step table outlining the main actions to take based on the guide above. This table will help ensure you do not miss any critical steps when cancelling your vehicle insurance.

| Step | Action | Key Details/Notes |

|---|---|---|

| 1 | Gather documentation | Policy details, new coverage (if switching), vehicle registration |

| 2 | Review timing | Coordinate policy dates to prevent coverage gaps |

| 3 | Notify insurer | Written notice through official channel |

| 4 | Confirm cancellation | Request written confirmation from provider |

| 5 | Check for penalties/refunds | Review for applicable fees or refund policies |

| 6 | Notify vehicle financier (if applicable) | Ensure financing requirements for continuous coverage are met |

| 7 | Store confirmation | Save cancellation letter & related documents |

Remember that maintaining continuous insurance coverage is not just a legal requirement in many jurisdictions but also a critical aspect of responsible vehicle ownership. A momentary lapse in coverage can result in significant financial risks and potential legal complications.

By following these systematic steps and maintaining clear communication with your insurance provider, you can navigate the vehicle insurance cancellation process confidently and efficiently. Always prioritize thorough research, careful planning, and meticulous documentation to ensure a smooth transition between insurance policies.

What Happens After Your Insurance is Cancelled

When car insurance is canceled, the consequences extend far beyond the immediate loss of coverage. Vehicle owners must understand the complex legal, financial, and practical implications that can significantly impact their driving capabilities and future insurance prospects.

Legal and Regulatory Consequences

Immediate legal ramifications follow an insurance cancellation. The Texas Department of Insurance emphasizes that driving without insurance can trigger severe penalties. These typically include substantial fines, potential license suspension, and even vehicle impoundment. Car owners must recognize that operating an uninsured vehicle is not just financially risky but also legally prohibited.

The legal landscape varies by jurisdiction, but common consequences include:

- License Suspension: Automatic revocation of driving privileges

- Registration Restrictions: Potential inability to renew vehicle registration

- Financial Penalties: Significant monetary fines for driving uninsured

Financial and Insurance Implications

Beyond immediate legal challenges, insurance cancellation creates long-term financial complications. Insurance regulatory experts highlight that a canceled policy can dramatically increase future insurance premiums. Insurers view policy cancellations as indicators of high risk, which often translates to substantially higher rates when seeking new coverage.

The financial impact extends to multiple areas:

- Higher insurance premiums for future policies

- Potential difficulty obtaining new insurance coverage

- Increased scrutiny from insurance providers

Rebuilding Insurance Eligibility

Our guide on insurance transitions provides insights into navigating post-cancellation challenges. Rebuilding your insurance profile requires strategic approaches:

- Maintain a clean driving record

- Address underlying issues that led to cancellation

- Shop around with multiple insurance providers

- Consider high-risk insurance options if standard coverage is unavailable

It is crucial to secure new insurance coverage immediately. Even a short lapse can create significant long-term complications. Some insurers specialize in providing coverage for individuals with previous cancellations, though typically at higher rates.

Vehicle owners should also proactively communicate with potential insurers, explaining the circumstances of their previous cancellation. Transparency can help mitigate perceived risks and potentially secure more favorable terms.

The process of recovering from an insurance cancellation requires patience, financial discipline, and a commitment to demonstrating responsible driving behavior. While challenging, it is entirely possible to rebuild your insurance profile and return to standard coverage rates.

Remember that prevention remains the most effective strategy. Maintaining consistent premium payments, avoiding high-risk behaviors, and regularly reviewing your insurance needs can help you avoid cancellation and its consequential challenges.

Tips to Avoid Car Insurance Cancellation Issues

Preventing car insurance cancellation requires proactive management and strategic planning. Vehicle owners must understand that maintaining continuous, reliable coverage is not just a legal requirement but a critical aspect of responsible vehicle ownership.

Financial Management Strategies

The Pennsylvania Insurance Department emphasizes the importance of consistent financial management in preventing policy cancellation. Premium payments represent the most fundamental aspect of maintaining insurance coverage.

Key financial strategies include:

- Automated Payment Setup: Configure automatic monthly payments to ensure timely premium settlements

- Payment Reminders: Utilize banking or insurance app notifications to track upcoming due dates

- Emergency Payment Fund: Maintain a dedicated financial buffer for insurance expenses

Understanding your policy’s grace period and communicating proactively with your insurer during potential financial challenges can prevent unnecessary cancellations. Many insurers offer flexible payment arrangements for customers experiencing temporary financial difficulties.

Risk Mitigation and Documentation

Reducing your risk profile is crucial in maintaining continuous insurance coverage. Our guide to securing cheaper insurance provides insights into managing your insurance profile effectively.

Risk mitigation strategies include:

- Maintaining a clean driving record

- Promptly reporting vehicle modifications

- Completing defensive driving courses

- Regularly updating personal information

- Installing approved vehicle security systems

Documentation plays a critical role in preventing cancellations. Keep comprehensive records of:

- Vehicle maintenance receipts

- Driving course certifications

- Communication with your insurance provider

- Updated personal contact information

Proactive Insurance Management

Effective insurance management goes beyond simple premium payments. Regular policy reviews and open communication with your insurer can prevent potential cancellation issues.

Recommended proactive steps:

- Conduct annual policy reviews

- Compare insurance rates periodically

- Understand your policy’s specific terms and conditions

- Address potential risk factors immediately

- Communicate transparently with your insurance provider about any changes in circumstances

If you anticipate challenges meeting policy requirements, contact your insurer before issues escalate. Many providers offer supportive solutions for customers experiencing temporary difficulties.

Remember that insurance is a collaborative relationship. Insurers prefer maintaining long-term relationships with responsible clients. By demonstrating reliability, financial discipline, and proactive risk management, you significantly reduce the likelihood of policy cancellation.

Continuous learning about insurance requirements, maintaining a responsible approach to vehicle ownership, and staying informed about potential risk factors are your best strategies for ensuring uninterrupted car insurance coverage.

Use the table below as a quick oral checklist for financial, risk, and proactive management strategies to avoid common car insurance cancellation pitfalls, as suggested throughout this section.

| Strategy Area | Actions/Best Practices |

|---|---|

| Financial Management | – Set up automatic payments |

- Use payment reminders

- Maintain emergency fund |

| Risk Mitigation | – Maintain clean driving record - Report modifications

- Defensive driving courses

- Update personal info |

| Proactive Management | – Annual policy review - Compare rates

- Know policy terms

- Communicate changes promptly |

Frequently Asked Questions

Can my car insurance be cancelled involuntarily?

Yes, your car insurance can be cancelled involuntarily for reasons such as non-payment of premiums, fraudulent activities, high-risk behaviour, or significant vehicle modifications without notification.

What steps should I take to properly cancel my car insurance?

To properly cancel your car insurance, gather your policy details, provide written notice to your insurer, confirm the cancellation, and be aware of any potential penalties or refunds.

What happens if my car insurance is cancelled?

If your car insurance is cancelled, you may face legal consequences such as fines or license suspension for driving uninsured, and you could encounter higher premiums or challenges obtaining new coverage in the future.

How can I avoid my car insurance being cancelled?

To avoid cancellation, ensure timely premium payments, maintain a clean driving record, communicate any changes to your insurer, and conduct regular policy reviews to stay informed about your coverage.

Protect Yourself from Unexpected Car Insurance Cancellation

Worried about losing your car insurance just when you need it most? After reading about the risks of involuntary cancellations, payment lapses, and the steep consequences of driving without proper cover, it’s clear that car owners in South Africa face very real threats to their financial security. The article highlights fears around policy termination, disruptive coverage gaps, and facing higher premiums if things go wrong.

Take action today to make sure your cover never lets you down. Get trusted guidance and easy tools with Insurance King Price, where you can find smart solutions for everything from third party car insurance to comprehensive policies that match your needs. Unsure about the best way to keep continuous cover or want help switching insurers without ever missing a day? Visit https://insurance.kingprice.co.za now to protect your vehicle, your finances, and your peace of mind before another day passes.

Recommended

- Renewing Car Insurance Policy: A Quick Guide for Owners – Savvy Insurance

- Insured Events Definition: What Car and Home Owners Need to Know – Savvy Insurance

- Car Insurance Fraud Risks in 2025: What Car Owners Must Know – Savvy Insurance

- Can You Transfer Car Insurance? Guide for South Africans 2025 – Savvy Insurance