Car insurance renewal feels like just another admin task, but there’s a lot more at stake for South Africans than you might think. Wait until you hear this. Almost 70 percent of South Africans do not compare quotes before renewing their car insurance. Most people leave thousands of rand on the table every year. The trick is, your renewal gives you a golden chance to save money and actually improve your cover at the same time.

Table of Contents

- Key Documents Needed For Renewal

- Factors Affecting Your Renewal Premium

- Comparing And Upgrading Your Cover Options

- Tips To Save Money On Car Insurance Renewal

Quick Summary

| Takeaway | Explanation |

|---|---|

| Key Documents Required | Ensure you gather essential personal and vehicle documentation, such as your South African identity document, proof of address, and motor vehicle licence notice, to streamline your renewal process. |

| Factors Impacting Premiums | Understand that your personal risk profile (age, claims history), vehicle characteristics (make, model, safety features), and geographical usage patterns significantly influence your renewal premiums. |

| Comparing Coverage Options | Assess different coverage types: comprehensive, third-party fire and theft, and third-party only, to choose a plan that fits your vehicle’s value and your financial needs. |

| Money-Saving Strategies | Improve vehicle security with advanced systems, consider higher voluntary excess to lower premiums, and explore bundling policies for discounts on insurance expenses. |

| Regular Quote Comparison | Regularly compare quotes from various providers to ensure you are not overpaying and to find the most cost-effective insurance options that suit your needs. |

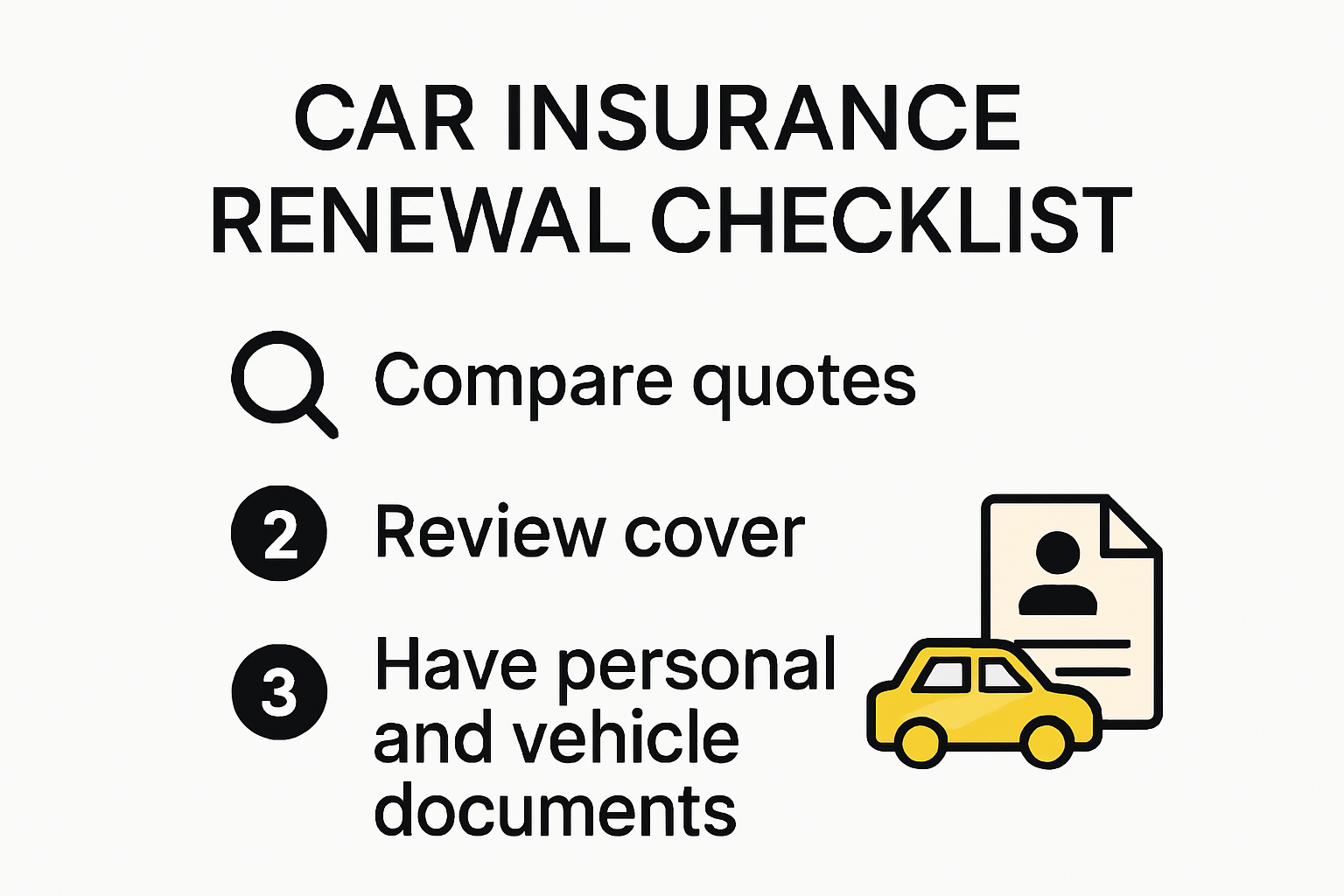

Key Documents Needed for Renewal

Renewing your car insurance requires careful preparation and gathering of essential documentation. Understanding the precise documents needed can streamline your renewal process and prevent unnecessary delays or complications.

Personal Documentation Requirements

When preparing for car insurance renewal, you will need several key personal documents to validate your identity and vehicle ownership. The primary documents include your valid South African identity document and proof of residential address. These documents serve as critical verification tools for insurance providers to confirm your personal details and assess risk.

Proof of address can typically be demonstrated through recent utility bills, bank statements, or official correspondence not older than three months. South African Government Services recommends ensuring these documents are current and clearly legible to expedite the renewal process.

For individuals whose vehicles are registered under a company or organization, additional documentation becomes necessary. This includes the business registration certificate, a formal letter of proxy, and the identity document of the designated proxy representative. These supplementary documents help insurance providers validate corporate vehicle ownership and ensure proper coverage.

Vehicle Documentation Essentials

Beyond personal identification, specific vehicle-related documents play a crucial role in the insurance renewal process. The most important document is your existing motor vehicle licence renewal notice (MVL2) or a completed Application for Licensing of Motor Vehicle (ALV) form. These documents provide critical information about your vehicle’s registration status and legal compliance.

Additionally, certain vehicle types require extra documentation. For public transport vehicles or heavy-load vehicles, a current roadworthiness certificate becomes mandatory. This certificate confirms that your vehicle meets the necessary safety and operational standards required by regulatory authorities. South African Road Traffic Management Corporation emphasizes the importance of maintaining updated roadworthiness documentation to ensure both legal compliance and insurance eligibility.

Digital Submission and Documentation Tips

With the increasing digitalization of administrative processes, many insurance providers now offer online renewal options. When submitting documents electronically, pay special attention to document quality and certification. Online Vehicle Licensing Portal recommends uploading certified copies of identification documents, ensuring all signatures are present, and verifying that proof of address documents are not older than three months.

To maximize efficiency during your car insurance renewal, create a comprehensive checklist of required documents beforehand. Organize your paperwork systematically, make clear digital copies, and double-check all information for accuracy. By being proactive and thorough in your document preparation, you can significantly reduce potential processing delays and ensure a smooth insurance renewal experience.

Remember that while these guidelines provide a general framework, specific insurance providers might have unique documentation requirements. Always consult directly with your insurance company to confirm the exact documents needed for your specific renewal process.

Here is a checklist table to help you organize the personal and vehicle documents required for car insurance renewal:

| Document Type | Description / Example | Required For |

|---|---|---|

| SA Identity Document | Valid green barcoded ID or smartcard | All vehicle owners |

| Proof of Address | Utility bill, bank statement (<3 months old) | All vehicle owners |

| Business Registration Certificate | CIPC document | Company/organization-owned vehicle |

| Letter of Proxy | Formal nomination letter | Company/organization-owned vehicle |

| Proxy ID Document | ID of designated company proxy | Company/organization-owned vehicle |

| MVL2 or ALV Form | Motor vehicle licence renewal notice / completed ALV | All vehicle owners |

| Roadworthiness Certificate | Current test certificate | Public transport/heavy vehicles |

Factors Affecting Your Renewal Premium

Car insurance renewal premiums are not static numbers but dynamic calculations based on multiple interconnected factors. Understanding these elements can help you anticipate potential changes in your insurance costs and potentially strategize ways to manage your premiums effectively.

Personal Risk Profile Considerations

Your individual risk profile plays a significant role in determining insurance renewal premiums. Insurance providers meticulously assess various personal characteristics to evaluate potential financial risk. Money Magazine highlights that driver demographics such as age, driving experience, and claims history are critical factors.

Younger drivers typically face higher premiums due to statistically higher accident rates and limited driving experience. Your claims history acts as a crucial indicator of future risk potential. Drivers with multiple previous claims are often perceived as higher-risk clients, which can result in increased renewal premiums. Maintaining a clean driving record and avoiding frequent claims can help manage your insurance costs.

Vehicle-Specific Pricing Factors

The characteristics of your vehicle significantly influence your insurance renewal premium. Factors such as the vehicle’s make, model, age, and market value directly impact insurance calculations. High-performance vehicles or luxury cars generally attract higher premiums due to elevated repair costs and increased theft risks.

Vehicle safety features can potentially offset some premium increases. Modern vehicles equipped with advanced security systems, tracking devices, and robust anti-theft mechanisms might qualify for insurance discounts. South African Road Traffic Management Corporation recommends documenting all vehicle safety enhancements to potentially negotiate more favorable renewal terms.

Geographic and Usage Considerations

Where and how you use your vehicle significantly impacts your insurance renewal premium. Geographical location plays a crucial role in risk assessment. Areas with higher crime rates, increased accident frequencies, or challenging road conditions typically result in higher insurance costs. Urban environments often attract higher premiums compared to rural areas due to increased traffic density and potential security risks.

Vehicle usage patterns also influence premium calculations. Vehicles used for business purposes or those with higher annual mileage are considered at greater risk of potential incidents. Insurers assess the probability of accidents based on how frequently and extensively the vehicle is driven. Savvy Insurance offers practical strategies for managing insurance costs related to vehicle usage.

To effectively manage your car insurance renewal premium, maintain a clean driving record, invest in vehicle safety features, and be transparent about your vehicle’s usage. Regular communication with your insurance provider and understanding these key factors can help you make informed decisions during the renewal process.

Remember that while these factors provide general guidance, individual insurance providers may have unique assessment criteria. Always consult directly with your insurance company to understand the specific factors influencing your particular renewal premium.

To help you understand how different factors impact your insurance renewal premium, here is a summary table of the key considerations:

| Factor | Example Impact | Effect on Premium |

|---|---|---|

| Age & Driving Experience | Young/inexperienced driver | Increases |

| Claims History | Multiple prior claims | Increases |

| Vehicle Make & Model | Luxury/high-performance cars | Increases |

| Vehicle Safety Features | Advanced alarms, tracking | Potentially decreases |

| Geographic Location | High-crime urban area | Increases |

| Vehicle Usage | Business use/high mileage | Increases |

| Roadworthiness Certification | Up-to-date certificate | Favourable for premium |

Comparing and Upgrading Your Cover Options

Renewing your car insurance presents an excellent opportunity to reassess and optimize your coverage. Understanding the nuanced differences between insurance options can help you make informed decisions that balance comprehensive protection with cost-effectiveness.

Understanding Basic Coverage Types

Car insurance in South Africa typically offers three primary coverage levels. Comprehensive insurance provides the most extensive protection, covering damages to your vehicle from accidents, theft, fire, and natural disasters, as well as third-party property damage. This option offers the most robust financial security but comes with higher premiums.

Third-Party, Fire, and Theft Insurance represents a middle-ground option. It covers damages to third-party property, protects against vehicle theft, and provides fire damage coverage. This option balances affordability with essential protection for vehicle owners who want more than basic third-party coverage but cannot afford comprehensive insurance.

Third-Party Only Insurance represents the most basic and typically least expensive option. It covers damages to third-party property but provides no protection for your own vehicle. While this option minimizes immediate costs, it leaves vehicle owners financially vulnerable in many scenarios.

To simplify the differences between basic car insurance coverage types, here is a comparison table:

| Coverage Type | What’s Covered | Typical Premium Level |

|---|---|---|

| Comprehensive | Own vehicle (accident, theft, fire, natural disasters), third-party property | Highest |

| Third-Party, Fire, & Theft | Third-party property, theft of own vehicle, fire | Moderate |

| Third-Party Only | Third-party property damage only | Lowest |

Evaluating Your Personal Insurance Needs

Choosing the right insurance coverage requires a careful assessment of your personal circumstances. Consider factors such as your vehicle’s age, market value, and your financial capacity to handle potential repairs or replacements. Newer or high-value vehicles typically benefit more from comprehensive coverage, while older vehicles might be better suited to third-party options.

Personal risk factors play a crucial role in coverage selection. If you live in an area with high crime rates or frequently drive in challenging road conditions, more comprehensive coverage becomes increasingly important. Insurance risk assessment emphasizes the importance of matching your coverage to your specific environmental and personal risk profile.

Strategies for Upgrading Your Coverage

When approaching your insurance renewal, consider several strategic approaches to optimize your coverage. Start by requesting quotes from multiple providers to compare options comprehensively. Pay attention to not just the premium costs, but also the specific inclusions, excess amounts, and additional benefits offered.

Additional coverage options can provide valuable protection. Consider add-ons like roadside assistance, car rental during repairs, or extended warranty coverage. While these increase your premium, they can offer significant financial protection in unexpected situations. Savvy Insurance provides insights into finding the most suitable insurance package for your specific needs.

Technology can also play a role in reducing your insurance costs. Many insurers now offer usage-based insurance programs that track driving behavior. By demonstrating safe driving habits through telematics devices or smartphone apps, you might qualify for reduced premiums.

Remember that insurance is not a one-size-fits-all solution. Your coverage should evolve with your changing life circumstances, vehicle condition, and financial situation. Annual renewal provides the perfect opportunity to reassess and adjust your insurance strategy, ensuring you maintain optimal protection while managing costs effectively.

Tips to Save Money on Car Insurance Renewal

Managing car insurance costs is a critical concern for vehicle owners seeking to balance comprehensive protection with financial practicality. Strategic approaches can help you significantly reduce your insurance renewal expenses without compromising essential coverage.

Vehicle Security and Risk Reduction Strategies

Improving your vehicle’s security profile can directly impact insurance premiums. Insurers assess risk based on the likelihood of theft or damage, so investing in robust security measures can translate to meaningful cost savings. Advanced security systems, such as GPS tracking devices, immobilizers, and sophisticated alarm systems, demonstrate to insurance providers that you are proactively mitigating potential risks.

Consider installing additional safety features like steering wheel locks, dashboard cameras, and secure parking solutions. These enhancements not only protect your vehicle but can also signal to insurers that you are a low-risk client. Some insurance providers offer specific discounts for vehicles equipped with recognized security technologies.

Smart Policy Management Techniques

Your approach to policy management can significantly influence renewal costs. Increasing your voluntary excess – the amount you agree to pay before insurance coverage kicks in – can substantially lower your monthly premiums. However, ensure the excess remains financially manageable in case of an actual claim.

Bundling insurance policies with a single provider often results in attractive discounts. Many insurers offer reduced rates for customers who combine car insurance with home or contents insurance. Savvy Insurance provides comprehensive insights into effective insurance bundling strategies that can help you maximize potential savings.

Technology-Driven Cost Optimization

Modern insurance providers are increasingly leveraging technology to offer personalized pricing models. Usage-based insurance programs, which track driving behavior through telematics devices or smartphone applications, can reward safe drivers with reduced premiums. By demonstrating consistent responsible driving habits such as maintaining moderate speeds, avoiding sudden braking, and driving during low-risk hours, you can potentially qualify for significant discounts.

Regularly comparing quotes from multiple insurance providers is another critical strategy. Insurance markets are competitive, and rates can vary substantially between providers. Conducting an annual review of available options ensures you are not overpaying for coverage. Many online platforms now offer quick comparison tools that can help you identify the most cost-effective options tailored to your specific needs.

Remember that while cost is important, the cheapest option is not always the most appropriate. Prioritize finding a balance between affordable premiums and comprehensive coverage that adequately protects your vehicle and financial interests. Consider consulting with insurance professionals who can provide personalized advice based on your unique circumstances.

Ultimately, proactive management, technological awareness, and strategic decision-making can help you optimize your car insurance renewal process, potentially saving significant amounts while maintaining robust protection.

Frequently Asked Questions

What documents do I need to renew my car insurance in South Africa?

To renew your car insurance in South Africa, you need a valid South African identity document, proof of address (like a recent utility bill), and your motor vehicle licence renewal notice (MVL2) or completed ALV form. If your vehicle is owned by a company, you will also need a business registration certificate and a letter of proxy.

How can I save money on my car insurance renewal?

You can save money on your car insurance renewal by improving your vehicle’s security features, increasing your voluntary excess, bundling policies with the same insurer, and regularly comparing quotes from different providers to find the best rates.

What factors affect my car insurance renewal premium?

Several factors can affect your car insurance renewal premium, including your personal risk profile (age, claims history), the specifics of your vehicle (make, model, safety features), and your geographic location and usage patterns. High-risk areas and high annual mileage typically result in higher premiums.

How do I compare different car insurance coverage options?

When comparing car insurance coverage options, consider the type of coverage you need: comprehensive, third-party fire and theft, or third-party only. Evaluate your vehicle’s value and your financial situation to choose the best coverage that balances your protection requirements and budget.

Make Your Next Car Insurance Renewal the Smartest Yet

Does renewing your car insurance in South Africa feel confusing or costly every year? If you are tired of overpaying or worrying that your documents are not correct, you are not alone. The checklist above highlighted how missing paperwork and not comparing options can leave you frustrated and out of pocket. Many South Africans are caught off-guard by rising premiums or unclear cover choices when it comes time to renew.

You do not have to struggle for another year. Take control with expert advice and fresh tips directly from the team at Insurance King Price. Our free guides help you manage personal documents, understand your risk profile, and compare cover options like comprehensive and third party car insurance. Ready to stop paying too much? Visit Insurance King Price today for all the tools you need to protect your car the smart way. Do not wait. Get personalised quotes and expert support before your next renewal deadline sneaks up on you.

Recommended

- Saving Money on Car Insurance: Top Tips for 2025 – Savvy Insurance

- Top Tips for Cheaper Car Insurance in South Africa 2025 – Savvy Insurance

- Top Car Insurance Tips South Africa 2025: Save and Stay Covered – Savvy Insurance

- Top Tips for Cheaper Car Insurance in South Africa 2025

- How to Switch Insurers in 2025: A Simple Guide for Car and Home Owners – Savvy Insurance

- What Is Car Insurance? A Simple Guide for 2025 – Savvy Insurance