Owning a car or home in South Africa means juggling serious risks and real financial decisions. Only about 30% of households have adequate home insurance according to recent market data, yet millions drive and live without the proper cover. You might think a basic policy is enough. The reality is ignoring hidden risks can cost you far more than just monthly premiums.

Table of Contents

- Understanding Your Unique Insurance Risks

- Key Factors When Reviewing Your Cover

- Tips for Choosing Suitable Car and Home Insurance

- Regularly Updating and Adjusting Your Policy

Quick Summary

| Takeaway | Explanation |

|---|---|

| Evaluate unique risks regularly. | Assess the specific risks related to your home and vehicle to tailor possible insurance needs effectively. |

| Review policies after life changes. | Significant events like marriage or renovations impact your insurance needs and should prompt a policy review. |

| Understand policy components thoroughly. | Know the coverage types, included risks, and claims processes to make informed insurance choices. |

| Monitor financial and risk landscapes. | Stay aware of broader economic and environmental factors that could influence your insurance requirements. |

| Strategically adjust your coverage over time. | Make informed adjustments to your insurance as necessary rather than making changes on impulse. |

Understanding Your Unique Insurance Risks

Evaluating your insurance needs is more than a simple checkbox exercise. Each car and home owner faces a unique set of risks that demand careful, personalized assessment. Understanding these risks requires a comprehensive approach that goes beyond standard coverage templates.

Personal Risk Profile Assessment

Every property and vehicle comes with its own risk landscape. Your specific circumstances dramatically influence the type and extent of insurance protection you require. According to Deloitte’s Risk Management Research, personal risk factors can include location, property type, vehicle usage, local crime rates, and individual lifestyle patterns.

For instance, a home in a high-flood zone requires different insurance considerations compared to a property in a low-risk area. Similarly, a car used for daily commuting in urban traffic presents different risk profiles than a weekend leisure vehicle. These nuanced differences mean that a one-size-fits-all insurance approach is fundamentally flawed.

Comprehensive Risk Evaluation Strategies

To effectively evaluate your insurance needs, you must conduct a thorough risk analysis. The South African Insurance Association recommends a multi-dimensional approach that considers several key factors:

- Geographic Location: Assess regional risks like natural disaster frequencies, crime statistics, and infrastructure challenges.

- Asset Value: Calculate the precise replacement cost of your vehicle and property, not just market value.

- Personal Liability Exposure: Consider potential legal and financial risks associated with property ownership and vehicle operation.

This strategic evaluation helps read more about avoiding coverage gaps and ensures you are not left vulnerable in critical moments.

Here’s a summary table outlining the key risk factors to consider when evaluating your insurance needs as discussed in the article:

| Risk Factor | Car Owners: Key Considerations | Home Owners: Key Considerations |

|---|---|---|

| Location | Urban traffic, crime rates, commuting routes | Flood zones, crime statistics, infrastructure |

| Asset Value | Vehicle replacement cost, depreciation | Replacement cost, renovations, market value |

| Usage Patterns | Daily vs. occasional use | Owner-occupied vs. rental property |

| Personal Liability Exposure | Accident risk, third-party liability | Guest injuries, legal risks, public liability |

| Security Measures | Anti-theft systems, parking conditions | Alarm systems, crime prevention features |

This table helps clarify the different aspects each owner should assess to tailor their insurance effectively.

Financial Protection Beyond Basic Coverage

Most car and home owners underestimate the potential financial impact of unforeseen events. Comprehensive risk understanding means looking beyond immediate, visible threats. Your insurance needs to account for indirect consequences such as temporary relocation costs, income disruption, or legal expenses.

Effective insurance is about creating a financial safety net that adapts to your evolving life circumstances. This requires periodic reassessment and willingness to adjust coverage as your personal and professional landscape changes. Regular insurance reviews ensure your protection remains relevant and robust against emerging risks.

Remember, understanding your unique insurance risks is not about purchasing the most expensive policy, but about crafting a tailored protection strategy that provides genuine peace of mind and financial security.

Key Factors When Reviewing Your Cover

Regularly reviewing your insurance coverage is crucial for ensuring comprehensive protection that matches your evolving life circumstances. While many car and home owners tend to set their policies and forget them, strategic and periodic assessments can save you significant financial stress and potential vulnerability.

Assessing Coverage Adequacy and Value

Insurance is not a static concept but a dynamic protection mechanism that must adapt to changing personal and financial landscapes. The Insurance Information Institute recommends conducting a thorough review of your policy at least annually, focusing on several critical aspects.

Key evaluation points include examining your property’s current replacement cost, which can change dramatically due to market fluctuations, renovations, or local infrastructure developments. For car owners, this means considering vehicle depreciation, technological upgrades, and changing usage patterns. Understanding the precise value of your assets ensures you are neither over-insured nor dangerously underinsured.

Life Changes and Insurance Alignment

Significant life transitions directly impact your insurance requirements. Marriage, divorce, having children, career changes, or purchasing new assets are pivotal moments that demand a comprehensive policy review. South African Insurance Experts emphasize that personal transformations often create new risk profiles that your existing coverage might not adequately address.

Consider scenarios like:

- Home Improvements: Major renovations can increase your property’s value and require adjusted coverage.

- Vehicle Changes: Upgrading to a newer or more expensive vehicle necessitates re-evaluating your insurance strategy.

- Personal Liability: Changes in professional status or lifestyle can introduce new potential risk exposures.

These transitions are not just administrative updates but critical financial protection mechanisms. learn more about comprehensive insurance strategies to ensure you remain fully protected.

Financial Risk Management

Effective insurance review goes beyond mere policy renewal. It’s a strategic financial risk management process. Analyze your current excess levels, understand potential out-of-pocket expenses, and evaluate how different coverage options balance premium costs against potential claim scenarios.

This approach requires a holistic view of your financial ecosystem. Consider your emergency savings, potential income disruptions, and the broader economic environment. A well-structured insurance policy should provide not just compensation, but genuine financial resilience.

Remember, insurance is ultimately about peace of mind. By conducting regular, thoughtful reviews, you transform your coverage from a mandatory expense into a proactive financial protection strategy that evolves alongside your life journey.

Tips for Choosing Suitable Car and Home Insurance

Selecting the right insurance coverage requires more than simply comparing prices. It demands a strategic approach that balances comprehensive protection with financial practicality. Car and home owners must navigate a complex landscape of policy options, ensuring their unique needs are met without unnecessary financial strain.

Understanding Policy Components

The South African Insurance Association highlights that effective insurance selection involves understanding the intricate components of different policy types. For car insurance, this means distinguishing between comprehensive, third-party, fire, and theft coverage. Home insurance similarly offers varied protection levels, from basic structural coverage to comprehensive plans that include personal belongings and liability protection.

Key considerations include:

- Coverage Scope: Evaluate what specific risks are included and excluded

- Claim Process: Understand the documentation and procedural requirements

- Network Support: Check the insurer’s reputation for customer service and claims handling

The following table compares the main types of car and home insurance policies, summarising the differences in coverage and typical inclusions as described in the article:

| Policy Type | Coverage Scope | Typical Inclusions |

|---|---|---|

| Car: Comprehensive | Broad (accidents, theft, fire, third-party, etc.) | Damage, theft, liability, fire |

| Car: Third-Party, Fire and Theft | Limited (liability, fire, theft only) | Third-party liability, fire, theft |

| Car: Third-Party Only | Basic (damage to others) | Third-party liability |

| Home: Basic Structural | Building structure only | Structural damage |

| Home: Comprehensive (incl. content) | Structure, belongings, personal liability | Structure, contents, liability |

This table provides a quick reference for the types of policies available and what protection they generally offer.

Potential policyholders should avoid the common mistake of choosing insurance based solely on price. read more about understanding car insurance fundamentals to make an informed decision.

Assessing Personal Risk Factors

Effective insurance selection requires a deep understanding of your personal risk profile. According to Consumer Reports, this involves carefully evaluating factors that influence your insurance needs.

For car owners, this means considering:

- Driving History: Previous accidents or traffic violations

- Vehicle Type: Age, model, and potential replacement cost

- Usage Patterns: Daily commuting versus occasional use

Home insurance requires similar nuanced assessment, including:

- Property Location: Proximity to natural disaster zones

- Home Construction: Building materials and age of the property

- Security Measures: Existing safety systems and crime prevention features

Maximizing Value and Protection

Choosing insurance is about finding the optimal balance between cost and comprehensive protection. This requires a holistic approach that goes beyond simple price comparisons. Look for policies that offer flexible options, allowing you to customize coverage to your specific needs.

Consider additional factors such as:

- Excess Levels: Higher excess can reduce premiums but increases out-of-pocket expenses during claims

- Additional Benefits: Look for value-added services like emergency assistance

- Payment Flexibility: Explore various payment options that suit your financial situation

Remember that the cheapest option is not always the most cost-effective. A slightly more expensive policy might provide significantly better protection and long-term financial security. The goal is to create a safety net that provides genuine peace of mind, protecting you from potential financial catastrophes while remaining financially sensible.

Regularly Updating and Adjusting Your Policy

Insurance is not a set-and-forget financial instrument. As life evolves, your insurance policy must adapt to reflect changing circumstances, risks, and personal circumstances. Proactive policy management ensures you maintain optimal protection while avoiding unnecessary financial strain.

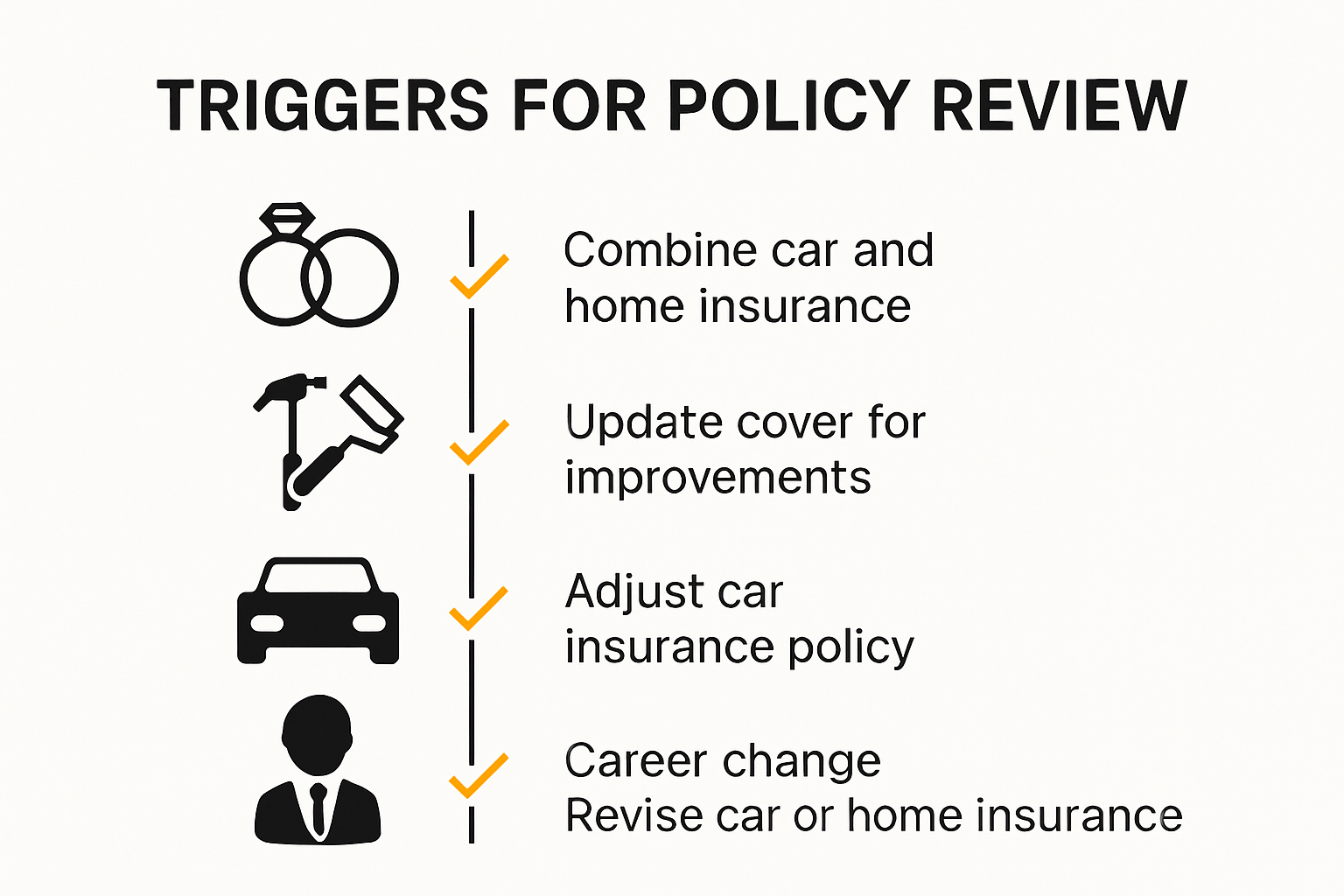

Triggers for Policy Review

The National Association of Insurance Commissioners emphasizes the importance of recognizing key life events that necessitate insurance policy adjustments. These triggers are critical moments when your existing coverage might no longer provide adequate protection.

Significant life events that demand immediate policy review include:

- Marriage or Divorce: Changes in household composition and shared assets

- Property Renovations: Increased home value or structural modifications

- Career Changes: Shifts in income, work-related risks, or professional status

- Vehicle Upgrades: Purchasing a new car or significant modifications

learn more about annual insurance review strategies to stay ahead of potential coverage gaps.

Financial and Risk Landscape Monitoring

Beyond personal life changes, broader economic and environmental factors can impact your insurance needs. According to Risk Management Expert Reports, car and home owners must remain vigilant about evolving risk landscapes.

Key areas to monitor include:

- Climate Change Impact: Increasing frequency of natural disasters

- Urban Development: Changes in local infrastructure and neighborhood risks

- Technology Advancements: New security systems or vehicle safety features

- Economic Fluctuations: Property value changes and replacement cost variations

Strategic Policy Adjustment Approach

Effective policy management is not about constant changes but calculated, strategic adjustments. Conduct a comprehensive review annually, but be prepared to make interim modifications when significant life events occur.

Consider these strategic approaches:

- Comparative Analysis: Regularly compare your current policy with market offerings

- Incremental Coverage: Adjust coverage limits progressively

- Bundling Opportunities: Explore combined car and home insurance options

- Excess Management: Reassess excess levels based on financial capacity

Remember, an outdated insurance policy can leave you financially vulnerable. Regular, thoughtful reviews transform insurance from a mere compliance requirement into a dynamic financial protection strategy that grows and adapts with your life journey.

Frequently Asked Questions

How often should I evaluate my insurance needs as a car or home owner?

Regularly reviewing your insurance needs at least annually is recommended, especially after significant life changes such as marriage, renovations, or vehicle upgrades.

What factors should I consider when assessing my insurance coverage adequacy?

Consider the current replacement cost of your home and vehicle, any changes in your assets, and your personal liability exposure to ensure you are adequately covered.

How do personal life changes affect my insurance needs?

Life events like marriage, divorce, or having children can alter your risk profile, necessitating a review of your insurance policies to ensure they align with your new circumstances.

What types of car and home insurance policies are available?

There are various types of policies, including comprehensive coverage, third-party liability, and structured home insurance. Understanding each type helps you choose the best fit for your needs.

Reimagine Your Insurance Strategy with Local Know-How

Worried about the real risks facing your car or home that a generic policy might miss? As explored in this article, many South Africans underestimate what it takes to get insurance that actually shields you from sudden loss, unexpected liability or costly life changes. Evaluating your exact risk profile, understanding the fine print, and making sure your cover stays relevant as your world evolves is more than a formality. It is your safety net. If you have found yourself uncertain about whether your current plan truly protects you or if you want a smart way to quickly align your cover with your needs, you are not alone.

Take the guesswork out of safeguarding your assets. Visit Insurance King Price to unlock hands-on tips and products tailored for South African car and home owners. Compare proven solutions or learn how comprehensive car insurance and home contents cover can adapt to your changing circumstances. Now is the time to put your insurance review into action and secure protection that moves with you. Start today and let your peace of mind match your lifestyle.

Recommended

- How to Avoid Underinsurance: Tips for SA Car and Home Owners 2025 – Savvy Insurance

- Annual Insurance Review Tips for Car and Home Owners 2025 – Savvy Insurance

- Insured Events Definition: What Car and Home Owners Need to Know – Savvy Insurance

- How to Lower Premiums: Easy Steps for Car and Home Owners 2025 – Savvy Insurance