Gap cover insurance seems like an afterthought until you see the numbers. Specialists in South Africa can charge up to 300 percent more than what your medical aid will pay. Most people reckon their medical aid will foot the whole bill, yet countless families end up with surprise medical debts that drain their savings. Turns out, the real risk isn’t the procedure itself but the massive shortfall you never knew was coming.

Table of Contents

- Understanding Gap Cover Insurance In South Africa

- Who Needs Gap Cover Insurance And Why

- How Gap Cover Insurance Works With Existing Policies

- Tips For Choosing The Right Gap Cover Plan

Quick Summary

| Takeaway | Explanation |

|---|---|

| Gap Cover is Essential | Gap cover insurance provides crucial financial protection by bridging the gap between what medical aid schemes reimburse and actual healthcare costs, significantly reducing out-of-pocket expenses for patients. |

| Eligibility Requirements | To qualify for gap cover, individuals must be active members of a registered medical aid plan, ensuring that it complements existing healthcare coverage. |

| Key Demographics | Various groups, including families with children, individuals with chronic conditions, and professionals in high-stress jobs, should consider gap cover due to their higher vulnerability to unexpected medical expenses. |

| Coverage Assessment is Crucial | When selecting a gap cover plan, consumers should assess their specific medical needs, existing coverage limitations, and understand policy exclusions and waiting periods to find the most suitable option. |

| Provider Reputation Matters | Evaluating the financial stability and customer satisfaction of gap cover providers is vital for ensuring reliable claims processing and overall service quality. |

Understanding Gap Cover Insurance in South Africa

Gap cover insurance represents a critical financial safety net for South Africans navigating the complex healthcare landscape. While many people assume their medical aid will cover all medical expenses, the reality is far more nuanced. Medical aid schemes typically reimburse healthcare services at predetermined rates, often leaving patients with significant out-of-pocket expenses.

How Gap Cover Works in Medical Scenarios

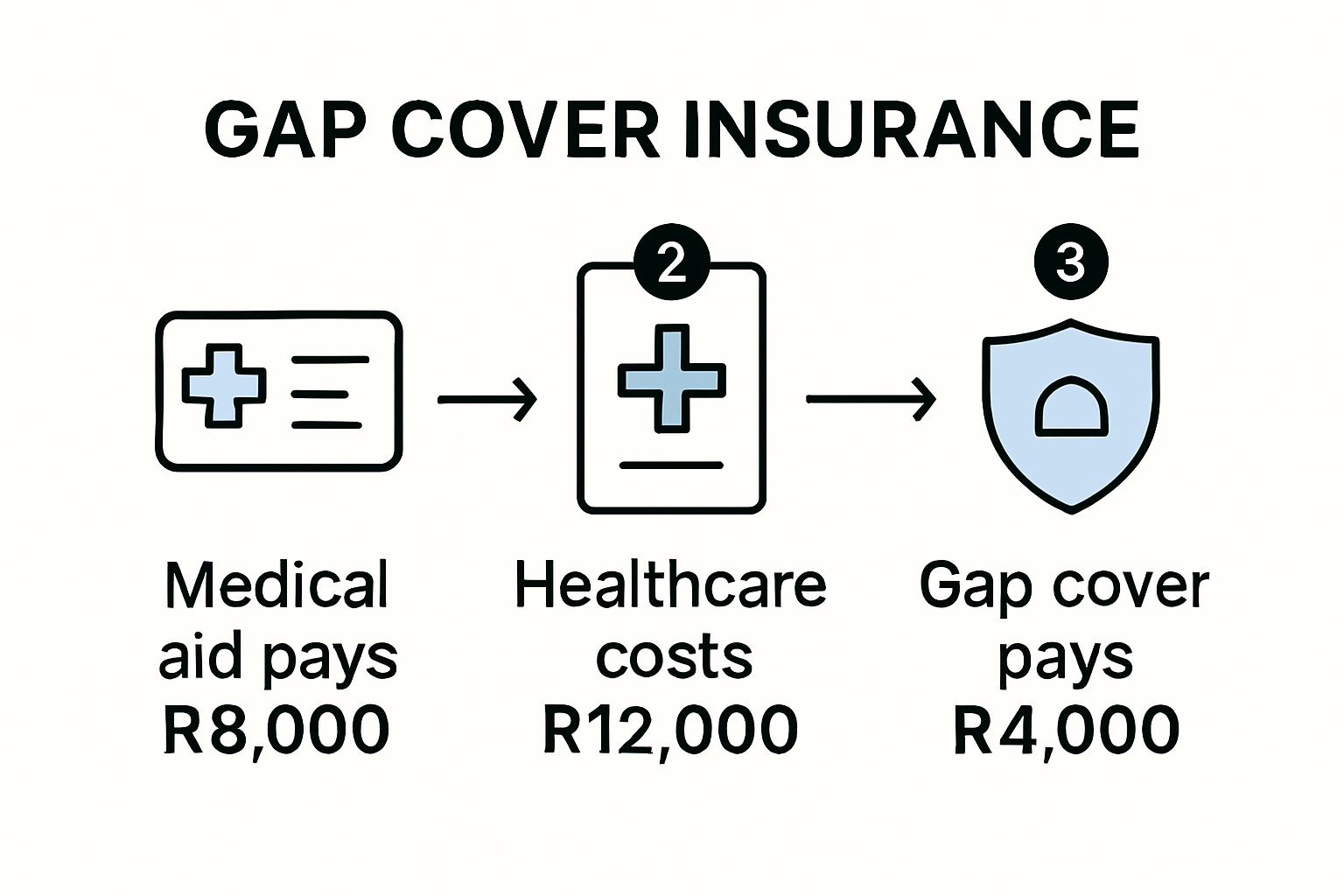

In practical terms, gap cover bridges the financial shortfall between what medical aid schemes pay and the actual costs charged by private healthcare providers. Consider a surgical procedure where a specialist charges R20,000, but your medical aid only covers R12,000 at their standard tariff rate. Without gap cover, you would be responsible for the R8,000 difference. This unexpected expense can create substantial financial strain for many households.

The mechanics of gap cover are straightforward yet powerful. When you have a medical procedure or treatment, gap cover steps in to cover the difference between the medical aid tariff and the actual cost charged by healthcare professionals. Research from the Health Professions Council of South Africa indicates that specialists often charge up to 300% more than medical aid rates, making gap cover an essential financial protection mechanism.

Eligibility and Key Considerations

To qualify for gap cover in South Africa, individuals must be active members of a registered medical aid plan. This requirement ensures that gap cover remains a complementary product designed to enhance existing medical coverage. The premiums are typically affordable, with monthly costs ranging from R150 to R500 per family, depending on the level of coverage and specific provider.

Interested readers can explore comprehensive car insurance strategies that might complement their overall risk management approach. Gap cover is not just about medical expenses but about providing financial peace of mind in unexpected health scenarios.

Key considerations when selecting gap cover include understanding coverage limits, waiting periods, and specific exclusions. Some gap cover providers offer additional benefits like oncology support, casualty cover, and co-payment assistance. Prospective buyers should carefully review policy details and compare offerings from different insurers to find the most suitable protection for their unique healthcare needs.

Ultimately, gap cover insurance represents a smart financial strategy for South Africans seeking comprehensive medical expense protection. By understanding how these policies work and selecting the right coverage, individuals can safeguard themselves against potentially devastating medical cost shortfalls.

Who Needs Gap Cover Insurance and Why

Gap cover insurance is not a luxury but a strategic financial protection mechanism for a wide range of South Africans. Research from News24 reveals that medical expenses can quickly escalate, making gap cover essential for many individuals and families.

Identifying Your Gap Cover Risk Profile

Certain groups are particularly vulnerable to significant medical expense shortfalls. Medical professionals, individuals with chronic conditions, and families with children are prime candidates for gap cover. For individuals undergoing specialized treatments or surgical procedures, the financial risk can be substantial. A single in-hospital procedure could result in out-of-pocket expenses ranging from R10,000 to R50,000, depending on the specialist and treatment complexity.

People with medical aid plans that offer limited coverage are especially at risk. These individuals might find themselves facing unexpected medical bills that can derail their financial stability. The Health Professions Council of South Africa highlights that specialists often charge up to 300% more than standard medical aid rates, creating a significant potential financial burden.

Key Demographics Benefiting from Gap Cover

Multiple demographic groups can benefit from gap cover insurance. Young professionals facing high-stress work environments, middle-aged individuals with increasing health complexities, and seniors managing multiple health conditions are prime examples. Families with children are particularly vulnerable, as pediatric treatments and unexpected medical emergencies can quickly strain financial resources.

Individuals with the following characteristics should strongly consider gap cover:

- Medical aid members with basic or mid-tier plans

- People with a history of medical conditions

- Professionals in high-stress or physically demanding careers

- Families with young children

- Individuals over 40 with potential health risks

Those interested in comprehensive financial protection might explore additional insurance strategies to manage their overall risk profile.

It is crucial to understand that gap cover is not just about covering immediate medical expenses. It provides peace of mind and financial protection against unexpected healthcare costs. The relatively low monthly premiums make it an accessible option for many South Africans seeking to mitigate potential financial risks.

While car and home owners are not the exclusive beneficiaries of gap cover, they often represent a demographic with the financial awareness to understand the importance of comprehensive insurance protection. By investing in gap cover, individuals can safeguard their financial future and ensure that medical emergencies do not become financial catastrophes.

To help identify which profiles and life stages are most likely to benefit from gap cover, below is a summary table of key demographics and their associated risk factors:

| Demographic Group | Typical Risk Factors | Why Gap Cover is Beneficial |

|---|---|---|

| Medical aid members (basic/mid-tier) | Limited scheme coverage, high out-of-pocket risk | Covers shortfalls on major treatments |

| People with chronic conditions | Frequent specialist care, higher treatment costs | Reduces recurring gap expenses |

| Families with young children | Accidental injuries, unexpected paediatric needs | Protects against unpredictable events |

| Professionals in high-stress jobs | Increased risk of illness, hospitalisation | Shields from sudden large expenses |

| Individuals over 40 | Growing health concerns, more complex procedures | Manages higher risk of medical bills |

How Gap Cover Insurance Works with Existing Policies

Gap cover insurance operates as a complementary financial protection mechanism designed to work seamlessly alongside existing medical aid policies. The South African Government’s Demarcation Regulations explicitly outline the parameters within which these supplementary policies function, ensuring clear boundaries and protections for consumers.

Legal Framework and Policy Integration

To qualify for gap cover, individuals must be active members of a registered medical scheme. This requirement ensures that gap cover remains a supplementary product enhancing existing medical coverage. The regulations stipulate that gap cover policies can only provide benefits for medical expenses not fully covered by medical schemes, including both Prescribed Minimum Benefit (PMB) and non-PMB conditions.

The integration process is straightforward. When a medical procedure occurs, the primary medical aid scheme first processes the claim according to its predetermined tariff rates. Gap cover then steps in to cover the remaining shortfall between the medical aid reimbursement and the actual healthcare provider charges. This mechanism protects patients from unexpected out-of-pocket expenses that can potentially derail their financial stability.

Practical Scenarios and Coverage Mechanics

Consider a typical medical scenario: A patient requires a surgical procedure where the specialist charges R30,000, but the medical aid scheme only covers R18,000. In this instance, the patient would traditionally be responsible for the R12,000 difference. Gap cover insurance bridges this financial gap, ensuring the patient is not burdened with substantial unexpected expenses.

Key aspects of how gap cover works with existing policies include:

- Covering co-payments and medical scheme shortfalls

- Providing additional protection for in-hospital treatments

- Offering support for specialized medical procedures

- Complementing existing medical aid coverage without replacing it

Individuals looking to optimize their overall insurance strategy might explore comprehensive protection options to manage their financial risks effectively.

It is crucial to understand that gap cover is not a standalone medical insurance product but a strategic financial tool designed to work in conjunction with existing medical aid schemes. Consumers should carefully review their current medical aid policy and gap cover options to ensure comprehensive protection.

The complexity of medical billing and insurance makes gap cover an increasingly essential consideration for South Africans seeking financial protection against unexpected healthcare expenses. By understanding how these policies integrate and complement existing medical coverage, individuals can make informed decisions about their healthcare financial planning.

Tips for Choosing the Right Gap Cover Plan

Selecting the appropriate gap cover plan requires careful consideration and strategic evaluation of multiple factors. Research from CRUE Insurance highlights the importance of understanding the nuanced details that distinguish different gap cover offerings in the South African market.

Comprehensive Coverage Assessment

A thorough evaluation of potential gap cover plans begins with understanding your specific medical needs and existing medical aid coverage. Consumers should meticulously review their current medical scheme’s limitations and identify potential financial vulnerabilities. Key aspects to examine include co-payment structures, sub-limits for specific treatments, and historical medical expenses that might indicate future healthcare requirements.

Consider the following critical coverage elements:

- Maximum annual cover limits

- Waiting periods for pre-existing conditions

- Specific treatment and procedure coverages

- In-hospital and out-of-hospital benefit ranges

- Oncology and chronic condition support

The following table summarises essential factors to compare when evaluating gap cover plans, making it easier to assess your choices at a glance:

| Coverage Element | What to Look For | Typical Variation Across Providers |

|---|---|---|

| Annual Cover Limit | Maximum total payout per year | R150,000 – R185,000+ |

| Waiting Periods | Delay before certain claims can be made | 3–12 months for pre-existing |

| In-hospital Benefits | Procedures/treatments covered while admitted | Widely included, but limits vary |

| Out-of-hospital Benefits | Some specialist procedures/casualty covered | Sometimes included, sometimes not |

| Co-payment Support | Pays fixed hospital/procedure co-payments | Varies by procedure/type |

| Oncology/Cancer Support | Assistance with cancer treatment shortfalls | Included in high-tier plans |

| Exclusions | Specific treatments not covered | Cosmetic, experimental, etc. |

Financial Stability and Provider Reputation

The Financial Sector Conduct Authority recommends thoroughly investigating the financial stability and reputation of gap cover providers. This involves examining the provider’s claims processing history, customer service quality, and financial ratings. Providers registered with the FSCA offer an additional layer of consumer protection and credibility.

Important factors to investigate include:

- Global Credit Rating (GCR)

- Claims payment track record

- Customer satisfaction ratings

- Regulatory compliance

- Transparency in policy terms

Individuals looking to optimize their insurance strategy might learn more about comprehensive protection options to enhance their overall financial risk management.

Understanding Policy Exclusions and Limitations

Careful examination of policy exclusions is crucial. Many gap cover plans have specific limitations that could significantly impact their practical value. Medical aid quote specialists recommend paying close attention to waiting periods, which typically range from 3 to 12 months for pre-existing conditions.

Common exclusions to watch for include:

- Cosmetic surgical procedures

- Experimental treatments

- Self-inflicted injuries

- Specific chronic conditions

- Treatments outside registered medical facilities

Choosing the right gap cover plan is not just about finding the lowest premium but identifying a comprehensive solution that provides robust financial protection. Consumers should approach this decision as a strategic investment in their healthcare financial security, carefully balancing coverage breadth, cost, and individual medical requirements.

Ultimately, the ideal gap cover plan offers a perfect blend of comprehensive coverage, financial protection, and peace of mind. By conducting thorough research, comparing multiple providers, and understanding the intricate details of each policy, South Africans can make informed decisions that safeguard their financial well-being in an increasingly complex healthcare landscape.

Frequently Asked Questions

What is gap cover insurance?

Gap cover insurance is a financial safety net that covers the difference between what your medical aid pays and the actual cost of healthcare services, reducing unexpected out-of-pocket medical expenses.

Who needs gap cover insurance?

Individuals who are active members of a registered medical aid plan, particularly those with chronic conditions, families with children, and professionals in high-stress jobs, should consider gap cover due to their higher risk of medical expense shortfalls.

How does gap cover insurance work?

Gap cover steps in when medical aid schemes only partially cover healthcare costs. For example, if a medical procedure costs R20,000 and your medical aid covers R12,000, gap cover will cover the remaining R8,000, protecting you from significant financial strain.

What should I consider when choosing a gap cover plan?

When selecting a gap cover plan, assess your specific medical needs, review current coverage limitations, understand policy exclusions, and compare different providers to find the option that best fits your healthcare requirements.

Secure Your Finances Beyond Just Medical Bills

Gap cover insurance can catch you off guard if you are not prepared for medical aid shortfalls. The article showed how quickly healthcare costs add up and why families who believe they are fully protected often end up paying unexpected bills. These financial shocks are not limited to medical emergencies. Unplanned expenses can strike your car or home too. Many South Africans overlook the full picture and end up taking risks that hurt their peace of mind.

If protecting your health is a priority, why leave your home or car exposed? Take control now and get the same peace of mind for your biggest assets. Visit Insurance Tips for South Africans to see how you can cover your car, home, and valuables on top of your medical aid plan. Get a quote or start the process directly from the King Price Insurance official site. Choosing the right cover today means you will not be caught off guard tomorrow. Act now to keep your finances protected from every angle.

Recommended

- Understanding Insurance Coverage Limits for Cars and Homes 2025 – Savvy Insurance

- Beyond Car Insurance: Extra Protection for Vehicles in 2025 – Savvy Insurance

- Top Benefits of Comprehensive Cover for Car and Home Owners 2025 – Savvy Insurance

- What Is Car Insurance? A Simple Guide for 2025 – Savvy Insurance

- Saving Money on Car Insurance: Top Tips for 2025 – Savvy Insurance

- Top Car Insurance Tips South Africa 2025: Save and Stay Covered – Savvy Insurance