Youth driver insurance can feel like a punch to the wallet. Drivers under 25 fork out around 30 percent more for premiums than older folks. Surprise, right? But here’s where it gets interesting. The smartest savings often come from the least expected moves, like choosing the right car or tapping into hidden family insurance loopholes. Get ready to flip the script on what you thought you knew about cutting insurance costs and staying safe behind the wheel.

Table of Contents

- Understanding Youth Driver Insurance Costs

- Why Youth Drivers Pay More

- Financial Impact Of Youth Insurance

- Strategies For Reducing Insurance Costs

- Smart Ways To Lower Your Premiums

- Vehicle Selection And Modification

- Personal Risk Management Strategies

- Technology And Monitoring Solutions

- Top Safety Tips For Young Drivers

- Understanding Road Risk Factors

- Essential Defensive Driving Techniques

- Technology And Personal Responsibility

- How Parents And Homeowners Can Help

- Financial And Insurance Guidance

- Safety Education And Skill Development

- Legal And Risk Management

Quick Summary

| Takeaway | Explanation |

|---|---|

| Young drivers face higher insurance costs | Drivers under 25 are charged approximately 30% more in premiums due to inexperience and higher accident rates. |

| Vehicle choice impacts premiums | Selecting vehicles with smaller engines, advanced safety features, and lower market values can help lower insurance costs significantly. |

| Safe driving reduces premiums | Maintaining a clean driving record, completing advanced driving courses, and using technology like telematics can lead to reduced insurance expenses. |

| Parental guidance is critical | Parents should communicate openly about insurance costs and responsibilities, support skill development, and establish clear rules about vehicle use for young drivers. |

Understanding Youth Driver Insurance Costs

Young drivers face unique challenges in the car insurance landscape, with costs significantly higher than more experienced motorists. Protecting new drivers requires understanding the complex factors that drive insurance pricing for youth.

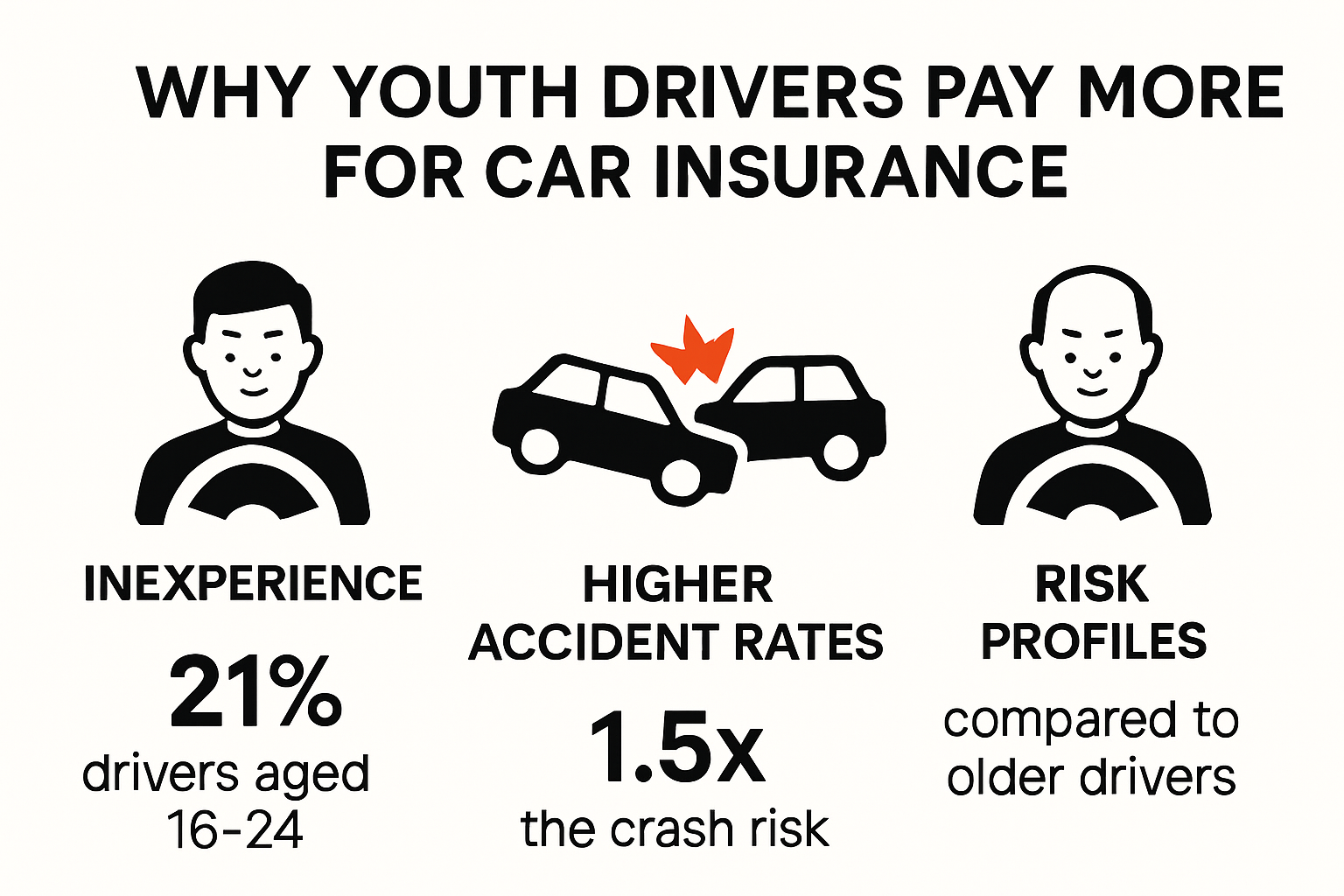

Why Youth Drivers Pay More

Insurance providers assess risk based on statistical data, and young drivers consistently represent a higher risk category. According to business research, drivers under 25 are charged approximately 30% more in insurance premiums compared to older drivers. This increased cost stems from several critical factors:

- Inexperience: Limited driving history means less predictable behavior on the road

- Higher Accident Rates: Statistical evidence shows younger drivers are more likely to be involved in accidents

- Risk Profile: Insurers view younger drivers as more likely to engage in risky driving behaviors

Financial Impact of Youth Insurance

The financial burden of insurance for young drivers is substantial. Research data reveals that in the 2017 financial year, the average insurance claim for drivers aged 18-25 increased to R40,976, up from R36,055 in 2016. This upward trend demonstrates the significant financial risk insurers associate with youth drivers.

Interestingly, approximately 87% of vehicles driven by individuals under 25 are insured under policies where the main policyholders are older than 32. This statistic suggests many young drivers rely on family insurance arrangements to manage costs.

Below is a table summarising key financial and statistical figures about youth driver insurance costs and trends for quick reference.

| Statistic | Figure | Description |

|---|---|---|

| Increased Premium for Under 25 | ~30% higher | Compared to older drivers; due to risk profile |

| Avg Insurance Claim (2016) | R36,055 | Mean claim value for ages 18-25 in 2016 |

| Avg Insurance Claim (2017) | R40,976 | Mean claim value for ages 18-25 in 2017 |

| Vehicles Insured by Older Policyholder | 87% | Share of under-25 vehicles with policyholder older than 32 |

Strategies for Reducing Insurance Costs

Young drivers are not without options. Several strategies can help mitigate the high insurance expenses:

- Complete advanced driving courses to demonstrate responsibility

- Choose a vehicle with lower insurance risk ratings

- Maintain a clean driving record

- Consider adding experienced drivers to the policy

- Opt for higher excess to lower monthly premiums

Understanding these nuanced factors can help young drivers navigate the complex world of car insurance more effectively. While costs remain challenging, informed decisions and proactive risk management can make a significant difference in insurance expenses.

Smart Ways to Lower Your Premiums

Young drivers can significantly reduce their insurance expenses by implementing strategic approaches. Uncover money saving tactics that make insurance more affordable without compromising protection.

Vehicle Selection and Modification

The type of vehicle you drive dramatically impacts your insurance premiums. Insurance providers assess risk based on specific vehicle characteristics. Choosing a car with lower risk factors can substantially reduce your insurance costs. Consider vehicles with:

- Smaller Engine Size: Smaller engines typically translate to lower insurance premiums

- Enhanced Safety Features: Advanced safety technologies can decrease potential claim risks

- Lower Market Value: Less expensive vehicles cost less to replace and repair

Additionally, installing security devices like advanced alarm systems, GPS tracking, and immobilizers can further reduce insurance expenses. These modifications demonstrate proactive risk management to insurance providers.

Below is a table comparing how different vehicle factors impact insurance premiums for young drivers.

| Vehicle Factor | Impact on Premiums | Examples |

|---|---|---|

| Engine Size | Smaller = Lower Premium | 1.2L, 1.4L engines |

| Safety Features | More safety = Lower Premium | Airbags, ABS, lane assist |

| Market Value | Lower value = Lower Premium | Used hatchback vs. new SUV |

| Security Devices | More security = Lower Premium | Alarm, immobilizer, GPS tracking |

Personal Risk Management Strategies

Your personal behavior and driving profile play crucial roles in determining insurance costs. Implementing specific strategies can help lower your premiums:

- Complete advanced driving courses to demonstrate responsible driving skills

- Maintain a consistently clean driving record

- Consider adding an experienced driver to your policy

- Opt for higher excess to reduce monthly premium costs

Insurance providers reward drivers who demonstrate lower risk potential. By showcasing responsible driving habits and investing in personal skill development, you can potentially negotiate more favorable insurance rates.

Technology and Monitoring Solutions

Modern insurance approaches leverage technology to provide more personalized and potentially cheaper insurance options. Telematics devices and smartphone apps can track driving behavior, offering opportunities for reduced premiums based on actual performance.

These monitoring solutions allow insurers to assess individual driving patterns more accurately. Safe drivers who consistently demonstrate careful driving techniques can benefit from usage-based insurance models that reward good behavior with lower premiums.

While insurance costs for young drivers remain challenging, proactive approaches and strategic decision-making can help manage and potentially reduce financial burdens. Understanding insurance dynamics and continuously improving your risk profile are key to securing more affordable coverage.

Top Safety Tips for Young Drivers

Navigating the roads as a young driver requires more than just technical skills. Learn critical safety strategies that can protect both your life and your insurance premiums.

Understanding Road Risk Factors

Young drivers face significant road challenges. According to government research, drivers aged 20 to 39 account for more than half of daily road fatalities. The most common accident types include pedestrian incidents, hit-and-run collisions, single-vehicle rollovers, and head-on crashes.

Distracted driving poses a substantial threat. Research indicates that approximately 25% of road crashes in South Africa result from mobile phone use while driving. This statistic underscores the critical importance of maintaining focus and eliminating potential distractions.

Essential Defensive Driving Techniques

Defensive driving goes beyond basic road rules. Key strategies include:

- Maintain Safe Following Distance: Keep at least three seconds of space between your vehicle and the one ahead

- Anticipate Other Drivers’ Actions: Constantly scan the road and predict potential hazards

- Minimize Distractions: Keep mobile phones out of reach and avoid multitasking

- Adapt to Weather Conditions: Reduce speed and increase caution during rain or low visibility

Safety data reveals that wearing seat belts reduces fatal injury risks by up to 50% for front-seat occupants and 75% for rear-seat passengers. Always ensure all passengers are properly restrained.

Technology and Personal Responsibility

Modern technology offers multiple tools to enhance driving safety:

- Use smartphone apps that block notifications while driving

- Install GPS tracking for emergency assistance

- Consider dash cameras for incident documentation

- Participate in advanced driving courses that teach modern safety techniques

Personal responsibility remains the cornerstone of safe driving. Regular vehicle maintenance, staying alert, and understanding your vehicle’s capabilities can significantly reduce accident risks.

Young drivers who prioritize safety not only protect themselves and others but also demonstrate responsible behavior that can positively impact their insurance premiums. Remember, safe driving is a continuous learning process that requires commitment, awareness, and proactive decision-making.

How Parents and Homeowners Can Help

Parents and homeowners play a crucial role in supporting young drivers through financial guidance, safety education, and strategic insurance planning. Discover comprehensive support strategies that can protect both family members and financial interests.

Financial and Insurance Guidance

Navigating insurance for young drivers requires proactive planning and open communication. According to insurance experts, parents should engage their children in detailed discussions about insurance responsibilities. Simply adding a child’s vehicle to a family policy without clear communication can lead to potential claim rejections and missed opportunities for financial education.

Key financial strategies include:

- Transparently discuss insurance costs and responsibilities

- Explore family policy options that provide comprehensive coverage

- Teach young drivers about excess payments and policy details

- Consider gradual insurance independence for young drivers

Safety Education and Skill Development

Parental involvement research highlights the critical importance of continuous support during the learning phase. Parents should focus on:

- Providing patient and constructive driving instruction

- Sharing personal driving experiences and lessons learned

- Demonstrating safe driving behaviors as role models

- Supporting advanced driving courses and skills training

Consistent guidance helps young drivers build confidence and develop essential road safety skills.

Legal and Risk Management

Legal experts warn that parents must be acutely aware of the significant risks associated with underage and unlicensed driving. Insurance companies strictly honor claims only from sober and licensed drivers, meaning parents could face substantial financial liabilities for unauthorized driving incidents.

Critical risk management steps include:

- Establishing clear family rules about vehicle usage

- Ensuring proper licensing and documentation

- Monitoring driving behavior and vehicle access

- Understanding potential legal and financial consequences

By taking a proactive, supportive approach, parents can help young drivers develop responsible habits, manage financial risks, and establish a solid foundation for safe and secure driving experiences. The investment in education and guidance pays dividends in creating confident, responsible young drivers who understand the complexities of insurance and road safety.

Frequently Asked Questions

Why do young drivers pay more for insurance?

Young drivers typically pay around 30% more for insurance premiums than older drivers due to inexperience and higher accident rates, making them a higher risk category for insurers.

What strategies can young drivers use to reduce insurance costs?

Young drivers can reduce insurance costs by completing advanced driving courses, choosing vehicles with lower risk ratings, maintaining a clean driving record, and potentially adding experienced drivers to their insurance policy.

How can selecting the right vehicle impact my insurance premiums?

Choosing a vehicle with a smaller engine size, enhanced safety features, and lower market value can significantly lower your insurance costs. Security devices like alarms and GPS can also help reduce premiums.

What role do parents play in helping young drivers with insurance costs?

Parents can help young drivers by discussing insurance responsibilities openly, exploring family insurance policy options, and supporting safety education and driving skill development, which can lead to reduced premiums.

Cut the Cost and Drive Protected: Youth Car Insurance Solutions

As a young driver in South Africa, you know the struggle of facing soaring insurance premiums and tighter budgets. This article highlighted how inexperience and higher accident statistics push up costs, while choosing the wrong car or missing out on advanced driving techniques leaves you exposed financially. The pressure to balance safety, affordability, and your independence can feel overwhelming, especially with insurers focusing on risk profiles and claims histories.

Why keep guessing about the best way to safeguard your ride and your future? Visit Insurance Tips and Tricks to discover practical advice tailored for South African youth drivers. Get accurate guidance on selecting the right vehicle, understanding third party vs comprehensive cover, and using technology to lower your premiums. Ready to turn these tips into real savings and proper cover? Get started now with a quote or explore personalised youth insurance options at insurance.kingprice.co.za.

Recommended

- Top Tips for Cheaper Car Insurance in South Africa 2025 – Savvy Insurance

- Top Car Insurance Tips South Africa 2025: Save and Stay Covered – Savvy Insurance

- Top Tips for Cheaper Car Insurance in South Africa 2025

- Saving Money on Car Insurance: Top Tips for 2025 – Savvy Insurance

- What Is Car Insurance? A Simple Guide for 2025 – Savvy Insurance

- Top Insurance Tips for Students: Car, Home & Auto 2025 – Savvy Insurance