Car insurance excess sounds simple but it trips up loads of South Africans every year. Many believe all you have to do is pay your premium and you are covered. Reality check. If you get into an accident, you could still land up paying a chunk out of your own pocket before your insurer even touches the bill. In fact, a higher excess can mean much lower monthly premiums, but at the risk of being hit with a hefty surprise expense at claim time. Most folks focus only on their premiums and miss how excess can quietly drain your wallet when you least expect it.

Table of Contents

- Understanding What Car Insurance Excess Means

- Different Types of Excess in Vehicle Insurance

- How Car Insurance Excess Affects Your Claims

- Tips to Save Money on Car Insurance Excess

Quick Summary

| Takeaway | Explanation |

|---|---|

| Understand your car insurance excess | Knowing the excess amount helps manage financial commitments if a claim arises. |

| Choose the right excess level | Balancing a manageable excess against reduced premiums is crucial for financial stability. |

| Consider compulsory vs. voluntary excess | Compulsory is set by insurers, while voluntary can be adjusted to lower premiums but increases out-of-pocket costs. |

| Maintaining a clean driving record saves money | Insurers tend to offer better excess rates to safe drivers with few or no claims. |

| Use technology to manage excess costs | Usage-based insurance can reduce excess rates based on safe driving behaviours tracked via apps or devices. |

Understanding What Car Insurance Excess Means

Car insurance excess is a fundamental concept that every driver should understand before signing an insurance policy. At its core, an excess is the amount you agree to pay out of pocket when making an insurance claim. Think of it as your financial contribution towards a potential repair or replacement of your vehicle after an incident.

How Car Insurance Excess Actually Works

When you experience a car-related incident that requires an insurance claim, the excess comes into play as a crucial financial mechanism. According to the Insurance Information Institute, a deductible (which is essentially the same as excess) is how risk is shared between you and your insurance provider. For instance, if you have a claim worth R50,000 and your excess is R5,000, the insurance company will pay R45,000 while you cover the initial R5,000.

The amount of excess can vary significantly based on several factors. As New York Department of Financial Services explains, insurers offer different excess levels to provide policyholders flexibility in managing their insurance costs. Generally, choosing a higher excess means lower monthly premiums, but it also means you’ll pay more out of pocket if a claim becomes necessary.

Types of Car Insurance Excess

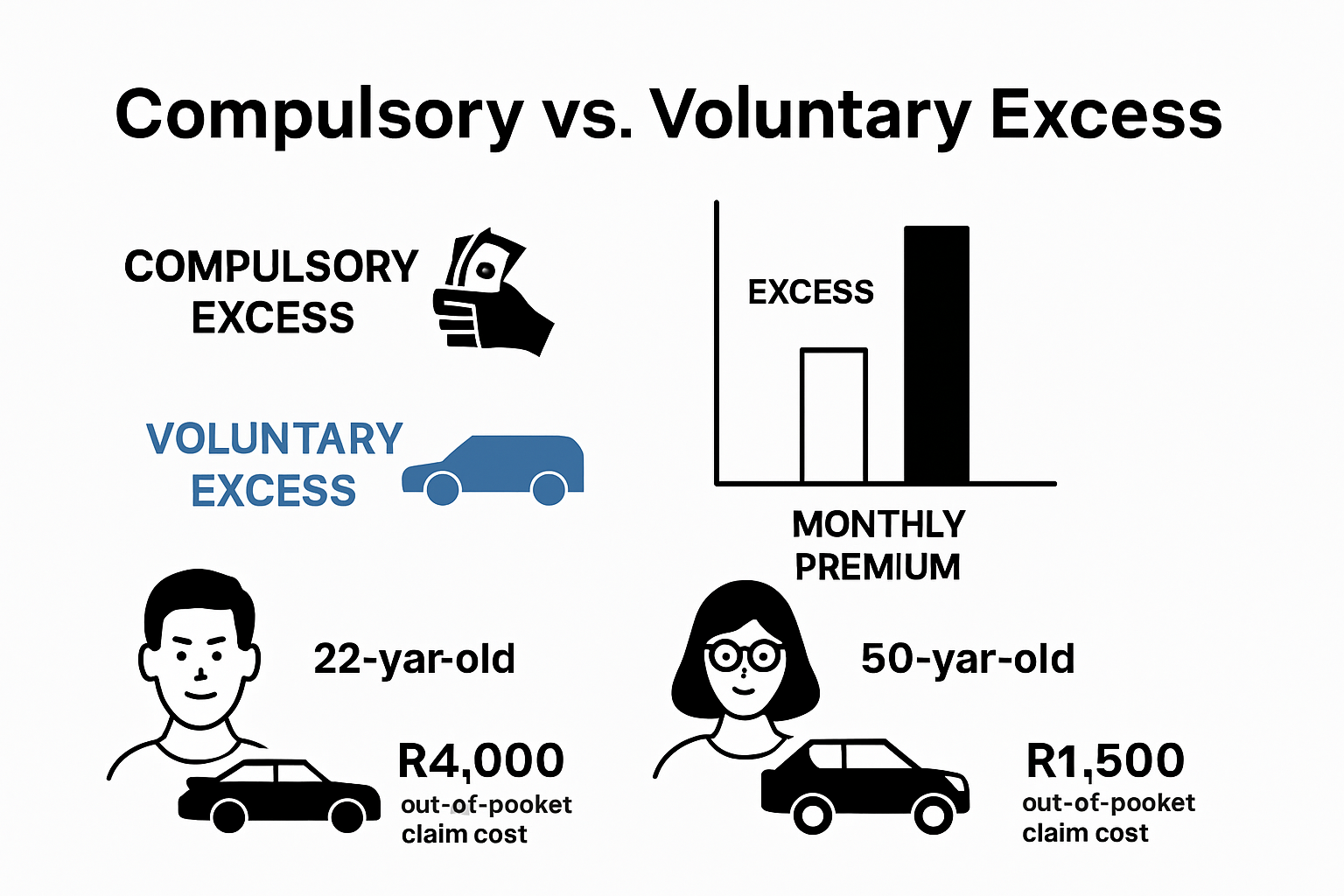

There are typically two primary types of excess in car insurance policies. The first is a compulsory excess, which is set by the insurance company and cannot be changed. This amount is non-negotiable and depends on factors like your age, driving experience, and the type of vehicle you drive. The second type is a voluntary excess, where you can choose to increase your contribution in exchange for lower monthly premiums.

Drivers should carefully consider their financial situation when selecting an excess amount. While a higher excess can reduce monthly costs, it also means being prepared to pay more immediately after an incident. The key is finding a balance that provides financial protection without creating undue strain on your personal budget.

Understanding your car insurance excess is more than just a technical detail—it’s a critical component of your overall financial risk management strategy. By knowing exactly how much you’ll be responsible for in the event of a claim, you can make more informed decisions about your insurance coverage and be better prepared for potential incidents on the road. Learn more about comprehensive insurance coverage to fully protect yourself and your vehicle.

Different Types of Excess in Vehicle Insurance

Vehicle insurance excess is not a one-size-fits-all concept. Different types of excess exist to cater to various risk scenarios and driver profiles. Understanding these variations can help you make more informed decisions about your insurance coverage and financial protection.

Compulsory versus Voluntary Excess

Two primary categories of excess dominate vehicle insurance policies. Compulsory excess is predetermined by the insurance provider and remains non-negotiable. According to the National Association of Insurance Commissioners, this fixed amount depends on factors like driver age, vehicle type, and risk assessment. For younger drivers or those with high-performance vehicles, compulsory excess tends to be higher due to increased statistical risk.

Voluntary excess represents the amount you choose to pay additional to your compulsory excess. As the Oregon Department of Administrative Services explains, this type of excess allows policyholders to customize their coverage. By selecting a higher voluntary excess, drivers can potentially reduce their monthly premiums. However, this strategy requires careful financial planning, as you’ll need to cover a larger initial amount in case of a claim.

Here is a comparison table highlighting the main differences between compulsory and voluntary car insurance excess, as explained in the article. This table can help you quickly understand how each excess type works and their implications.

| Feature | Compulsory Excess | Voluntary Excess |

|---|---|---|

| Set By | Insurance company | Policyholder (driver) |

| Negotiable | No | Yes |

| Influenced By | Driver’s age, car type, risk factors | Driver’s personal choice |

| Impact on Premiums | Fixed impact | Higher voluntary excess lowers premiums |

| Out-of-Pocket Cost at Claim | Required | Adds to compulsory excess amount |

| Flexibility | None | Customisable for financial planning |

| Main Benefit | Standardised coverage | Potential for lower monthly payments |

Specialized Excess Categories

Beyond the standard compulsory and voluntary models, several specialized excess types exist in vehicle insurance. Young driver excess specifically targets drivers under a certain age threshold, typically charging higher excess due to their perceived higher risk. Named driver excess applies when a specific individual listed on the policy makes a claim, often with different excess rates based on their driving history.

Some insurers also offer excess protector options, which allow you to recover your excess payment under certain circumstances. Check out our comprehensive guide on insurance add-ons to understand how these specialized excess protection mechanisms work.

Additionally, the Oklahoma Insurance Department highlights the importance of understanding Guaranteed Asset Protection (GAP) coverage. This specialized excess type pays the difference between a vehicle’s actual cash value and the remaining loan amount in case of total loss, providing an extra layer of financial protection.

The following table summarises specialised types of car insurance excess described in the article. This provides an at-a-glance overview of extra excess roles and their typical triggers for South African drivers.

| Excess Type | Who/What It Applies To | Reason/Purpose |

|---|---|---|

| Young Driver Excess | Drivers under a certain age | Reflects statistically higher risk |

| Named Driver Excess | Specific listed driver on the policy | Varies based on individual’s driving history |

| Excess Protector | All drivers (with add-on purchased) | Recovers excess payment in certain scenarios |

| GAP Excess | Vehicle owners with outstanding loans | Pays shortfall between car value and loan owed |

Choosing the right excess is about balancing risk and affordability. While a higher excess can lower your monthly premiums, it also means more out-of-pocket expenses during a claim. Carefully assess your financial situation, driving history, and risk tolerance when selecting your excess structure. Consulting with an insurance professional can help you navigate these complex decisions and find the most suitable coverage for your specific needs.

How Car Insurance Excess Affects Your Claims

Car insurance excess plays a critical role in the claims process, directly impacting both your financial responsibility and the overall claim settlement. Understanding how excess influences your insurance claims can help you make more informed decisions and manage your financial expectations during stressful situations.

The Financial Mechanics of Claims and Excess

When an insurable incident occurs, the excess becomes your immediate financial contribution towards the total repair or replacement costs. According to the Texas Department of Insurance, if your repair costs are R6,500 and your excess is R500, you will pay the initial R500, with your insurance covering the remaining R6,000. This mechanism ensures that policyholders have a direct stake in managing risk and maintaining their vehicles responsibly.

The Insurance Information Institute emphasizes that your chosen excess amount significantly influences your premium costs. Opting for a higher excess can lower your monthly insurance payments, but it simultaneously increases your out-of-pocket expenses during a claim. This trade-off requires careful financial planning and a realistic assessment of your personal risk tolerance.

Strategic Considerations in Claims Management

Your excess strategy can dramatically affect your claims approach. Some drivers might choose to handle minor damages privately if the repair costs are close to or only slightly above their excess amount. For instance, if a small scratch repair costs R1,200 and your excess is R1,000, it might be more economical to pay out of pocket rather than file a claim that could potentially increase your future premiums.

Explore our comprehensive guide on making insurance claims to understand the nuanced strategies for managing your excess effectively. The decision to claim or not claim involves weighing immediate repair costs against potential long-term premium increases.

The New York State Department of Financial Services recommends selecting an excess amount that aligns with your financial capabilities. While a higher excess can reduce monthly premiums, you must ensure you can comfortably cover that amount in the event of an unexpected incident. This means having an emergency fund that can absorb the excess payment without causing significant financial strain.

Moreover, your claims history and excess interactions can influence future insurability. Frequent claims, even for minor incidents, might signal higher risk to insurers and potentially lead to increased premiums or more restrictive coverage terms. Therefore, your excess is not just a financial mechanism but also a strategic tool in managing your overall insurance profile.

Ultimately, understanding how car insurance excess affects your claims requires a holistic view of risk management. It’s about finding the right balance between affordable premiums, manageable out-of-pocket expenses, and comprehensive protection. Regularly reviewing your excess levels, maintaining a good driving record, and consulting with insurance professionals can help you optimize your coverage strategy.

Tips to Save Money on Car Insurance Excess

Managing your car insurance excess strategically can lead to significant financial savings. While many drivers focus solely on monthly premiums, understanding how to optimize your excess can provide substantial long-term economic benefits. Smart excess management requires a combination of proactive planning, risk assessment, and strategic decision-making.

Choosing the Right Excess Level

Selecting an appropriate excess is a delicate balance between immediate affordability and potential future savings. According to the National Association of Insurance Commissioners, opting for a higher deductible (excess) is a proven strategy to lower monthly premiums. However, this approach requires careful consideration of your personal financial situation.

Consider your emergency savings and risk tolerance when selecting an excess. A higher excess might reduce your monthly payments, but ensure you can comfortably cover that amount if an unexpected incident occurs. Financial experts recommend maintaining an emergency fund that can easily absorb your chosen excess amount without causing financial strain.

Strategic Approaches to Reducing Excess Costs

Multiple strategies can help minimize your car insurance excess expenses. Maintaining a clean driving record is paramount. Insurers typically offer lower excess rates to drivers with fewer claims and traffic violations. Investing in additional vehicle security measures like approved tracking systems, immobilizers, and parking in secure locations can also potentially reduce your excess.

Discover more strategies for reducing insurance costs that go beyond just adjusting your excess. Consider bundling multiple insurance policies, completing defensive driving courses, and regularly reviewing your coverage to ensure you’re getting the most cost-effective protection.

Another effective approach is comparing excess options across different insurance providers. Some insurers offer more flexible excess structures or additional benefits that can help offset potential out-of-pocket expenses. Don’t hesitate to negotiate or request personalized excess packages that align with your specific driving profile and financial circumstances.

Technology can also play a crucial role in managing excess costs. Many modern insurance providers offer usage-based insurance programs that track your driving behavior. By demonstrating safe driving habits through telematics devices or smartphone apps, you might qualify for reduced excess rates or additional discounts.

Remember that the cheapest excess is not always the most economical option. While a high excess can lower monthly premiums, it increases your financial risk during a claim. The goal is to find a balanced approach that provides adequate protection without placing undue financial burden on yourself.

Consulting with an insurance professional can provide personalized insights tailored to your specific situation. They can help you navigate the complexities of excess selection, identify potential savings opportunities, and develop a comprehensive insurance strategy that protects both your vehicle and your financial well-being.

Frequently Asked Questions

What does car insurance excess mean?

Car insurance excess is the amount you agree to pay out of pocket when making an insurance claim. It acts as your financial contribution toward the repair or replacement costs of your vehicle after an incident.

How does car insurance excess work when I make a claim?

When you make a claim, the excess is deducted from the total claim amount. For example, if your repair costs are R6,500 and your excess is R500, you will pay R500, and the insurance company will cover the remaining R6,000.

What is the difference between compulsory and voluntary excess?

Compulsory excess is set by the insurance provider and cannot be changed, while voluntary excess is an amount you choose to pay in addition to the compulsory excess to lower your monthly premiums. Choosing a higher voluntary excess can reduce your ongoing costs but increases your immediate out-of-pocket expenses after a claim.

How can I save money on car insurance excess?

To save money on car insurance excess, consider maintaining a clean driving record in order to qualify for lower excess rates. Additionally, you can choose an appropriate excess level that balances lower premiums with manageable out-of-pocket costs during a claim, and invest in vehicle security measures to potentially reduce your excess costs.

Take Control of Your Car Insurance Excess Today

Worried about hidden costs and surprise payments every time you claim on your car insurance? So many South Africans are caught off guard by high excess amounts because they focus only on monthly premiums. If you have ever felt uneasy about not fully understanding the real out-of-pocket costs when something happens to your car, trust that you are not alone. Managing compulsory and voluntary excess can feel overwhelming, especially if you want peace of mind without blowing your budget.

Now is the perfect time to take the confusion out of car insurance. Visit our main site and use practical tips to save money and feel empowered. Compare your current excess with tailor-made options for comprehensive protection, transparent excess terms, and accessible support. Do not wait until your next accident to discover your excess is too high. Discover clever ways to manage and reduce your car insurance excess so you can protect what matters most.

Recommended

- Understanding Insurance Coverage Limits for Cars and Homes 2025 – Savvy Insurance

- Car Insurance Terms Guide 2025: Simple Tips for SA Drivers – Savvy Insurance

- Car Insurance Basics 2025: Simple Guide for SA Drivers – Savvy Insurance

- How to Add Drivers to Insurance in 2025: A Guide for Car Owners – Savvy Insurance