Every South African with a bank account or a cellphone contract has a credit score ticking away in the background and it holds more power than most people realise. Some think credit scores are only about getting a loan but your credit score can actually make your insurance premiums hundreds of rands cheaper or more expensive every year. And here’s the kicker. Improving your score is often much simpler than you expect and it could save you a fortune without changing anything else about your cover.

Table of Contents

- What Is A Credit Score And How Is It Calculated?

- The Importance Of Credit Score In Insurance Premiums

- How Insurance Companies Use Credit Scores

- Impact Of Credit Scores On Different Types Of Insurance

- Managing Your Credit Score For Better Insurance Rates

Quick Summary

| Takeaway | Explanation |

|---|---|

| Credit scores impact lending decisions. | Financial institutions use credit scores to assess borrowing risks and lending conditions. Higher scores lead to better loan terms. |

| Payment history is crucial for scores. | Approximately 35% of a credit score is derived from payment history, making it essential to pay bills on time. |

| Credit scores influence insurance premiums. | Insurers use credit scores to determine risk, affecting the premiums you pay. Higher scores often result in lower insurance costs. |

| Maintaining a low credit utilization ratio is vital. | Keeping your credit utilization low (under 30%) positively affects your score and financial health, helping to lower insurance premiums. |

| Regular credit monitoring is essential. | Monitoring your credit report ensures accuracy and helps identify areas for improvement, directly impacting your financial opportunities. |

What is a Credit Score and How is it Calculated?

A credit score is a numerical representation of an individual’s financial trustworthiness and creditworthiness, serving as a crucial indicator for financial institutions when assessing lending risks. In South Africa, this three-digit number typically ranges between 300 and 850, with higher scores signaling greater financial reliability.

Understanding Credit Score Fundamentals

Credit scores are calculated using complex algorithms that analyze multiple financial behaviors and historical data points. The primary factors influencing your credit score include:

- Payment history and consistency

- Total debt levels

- Credit utilization ratio

- Length of credit history

- Types of credit accounts

Financial institutions like banks and credit bureaus such as TransUnion and Experian use these metrics to evaluate an individual’s potential risk as a borrower. The National Credit Act provides the regulatory framework that governs how these scores are developed and used.

Credit Score Calculation Process

The calculation of a credit score involves sophisticated statistical models that weigh different financial behaviors. Typically, payment history contributes approximately 35% of the total score, while credit utilization accounts for around 30%. Outstanding debt represents roughly 15%, with the remaining percentage distributed across credit mix and recent credit inquiries.

For South African consumers, maintaining a good credit score requires consistent financial discipline. This means making timely payments, keeping credit card balances low, and avoiding excessive credit applications. A strong credit score can significantly impact your ability to secure loans, negotiate better interest rates, and access financial opportunities.

Below is a breakdown of the main factors contributing to your credit score calculation in South Africa, illustrating their relative importance and what each factor represents.

| Factor | Contribution to Score | Description |

|---|---|---|

| Payment History | 35% | Timeliness and consistency of all credit repayments |

| Credit Utilisation | 30% | Proportion of credit used compared to credit limits |

| Outstanding Debt | 15% | Total value of active debts owed |

| Credit Mix & Types | ~10% | Variety of credit accounts (retail, personal loans, accounts) held |

| Recent Credit Inquiries | ~10% | Number of recent applications for new credit |

Understanding your credit score is not just about numbers but about demonstrating financial responsibility and building a solid economic foundation for your future.

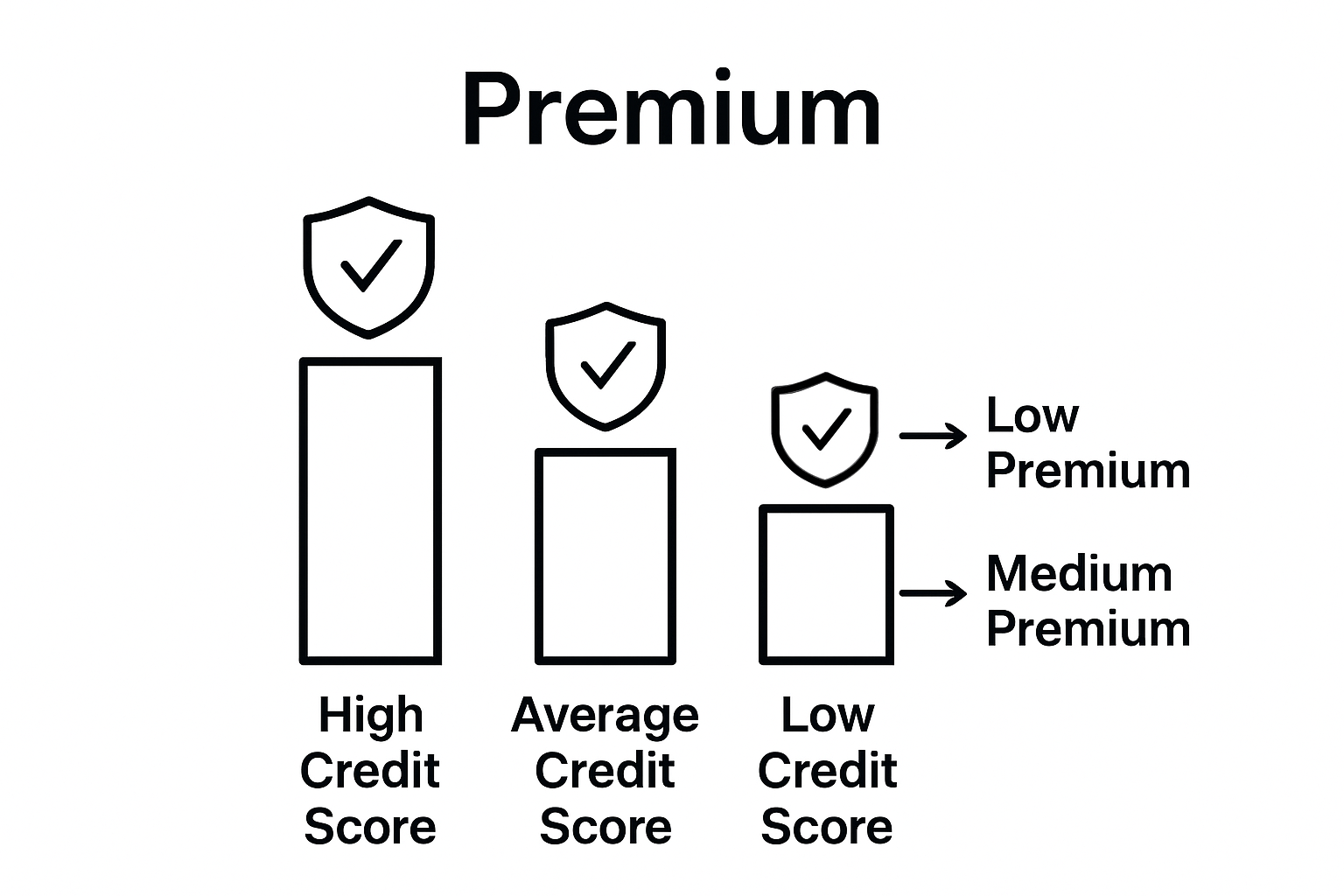

The Importance of Credit Score in Insurance Premiums

In the complex world of insurance, your credit score plays a pivotal role in determining the premiums you pay. Insurers use credit scores as a critical risk assessment tool, viewing them as a reliable indicator of financial responsibility and potential future claims behavior.

How Credit Scores Impact Insurance Risk Assessment

Insurance companies view your credit score as more than just a financial number. It serves as a predictive model that helps them estimate the likelihood of future insurance claims. Individuals with higher credit scores are statistically more likely to:

- Demonstrate responsible financial management

- Maintain their insured assets more carefully

- Have fewer insurance claims

- Present lower overall risk to the insurance provider

This risk assessment directly influences the insurance premiums you are offered.

The South African Credit and Risk Reporting Association confirms that insurers analyze credit profiles to determine potential risk levels and appropriate premium rates.

The South African Credit and Risk Reporting Association confirms that insurers analyze credit profiles to determine potential risk levels and appropriate premium rates.

Financial Behavior and Premium Calculations

Your credit score reflects your financial discipline, which insurers interpret as an indicator of potential insurance risk. A lower credit score might suggest a higher probability of filing claims, leading to increased premiums. Conversely, a strong credit score can translate into more favorable insurance rates.

For South African consumers, this means maintaining a good credit score is not just financially prudent but can also lead to significant savings on insurance premiums. By understanding how car premiums are calculated, individuals can take proactive steps to manage their credit and potentially reduce their insurance costs.

Ultimately, your credit score is a powerful financial tool that extends beyond loan applications, directly impacting your insurance expenses and overall financial health.

How Insurance Companies Use Credit Scores

Insurance companies employ sophisticated algorithms to leverage credit scores as a critical risk assessment tool, transforming numerical data into predictive insights about potential policyholder behavior. This advanced approach allows insurers to develop more nuanced and personalized risk profiles.

Credit Score Risk Modeling

Insurence providers analyze credit scores through complex statistical models that evaluate multiple financial indicators. These models help them understand the probability of future claims and potential financial risks associated with individual policyholders. Key aspects of credit score risk modeling include:

- Assessing historical financial consistency

- Evaluating debt management patterns

- Measuring credit utilization rates

- Analyzing long-term financial stability indicators

- Predicting potential insurance claim likelihood

The National Credit Act provides regulatory guidelines that ensure these credit score assessments remain fair and transparent for consumers.

Premium Calculation Strategies

Insurers translate credit score insights into precise premium calculations. A lower credit score might signal higher financial volatility, potentially resulting in increased insurance rates. Conversely, individuals with strong credit histories often receive more favorable premium structures.

To help consumers make informed decisions, understanding how to choose the right insurer becomes crucial. The connection between credit scores and insurance premiums underscores the importance of maintaining solid financial health.

Ultimately, credit scores serve as a comprehensive financial snapshot, enabling insurance companies to develop more accurate risk assessments and pricing strategies that benefit both insurers and responsible policyholders.

Impact of Credit Scores on Different Types of Insurance

Credit scores play a nuanced role across various insurance categories, influencing premium calculations and risk assessments differently for each insurance type. Understanding these variations helps consumers make more informed financial decisions and manage their insurance portfolios effectively.

Vehicle Insurance Credit Score Dynamics

In vehicle insurance, credit scores significantly impact risk assessment and premium determination. Insurers analyze credit history to predict potential driving behaviors and claim probabilities. Key considerations include:

- Correlation between financial responsibility and driving habits

- Potential for higher claim frequencies with lower credit scores

- Assessment of vehicle maintenance and risk management

- Predictive modeling of potential accident likelihood

- Long-term financial stability indicators

The South African Credit and Risk Reporting Association confirms that credit scores provide critical insights into policyholder risk profiles.

Comprehensive Insurance Category Analysis

Beyond vehicle insurance, credit scores influence multiple insurance domains. Home insurance, life insurance, and personal liability coverage all integrate credit score assessments into their underwriting processes. Individuals with higher credit scores typically receive more favorable terms and lower premiums across these insurance categories.

To help consumers navigate these complex dynamics, understanding car insurance trends becomes essential for making strategic insurance decisions.

Ultimately, maintaining a strong credit score is not just a financial recommendation but a critical strategy for securing comprehensive and cost-effective insurance coverage across different risk categories.

This table compares how credit scores affect different types of insurance policies and the typical impact on premiums and underwriting approaches in South Africa.

| Insurance Type | Role of Credit Score | Typical Effect on Premiums | Notes |

|---|---|---|---|

| Vehicle Insurance | Used in risk and claim probability | Large impact – higher scores mean lower rates | Linked to prediction of driving and claim behaviours |

| Home Insurance | Assesses financial stability | Moderate – good score can lower premiums | Often combined with other safety or location factors |

| Life Insurance | Evaluates reliability and risk | Some impact, but less than short-term covers | Credit history reflects overall financial management |

| Personal Liability | Used for risk assessment | May affect rates if score is low | Strong scores can ease approval for higher cover limits |

| Cellphone/Device Cover | Sometimes checked for contract terms | Credit score influences approval & pricing | Lower score may mean upfront payments or higher excess |

Managing Your Credit Score for Better Insurance Rates

Managing your credit score is a strategic financial approach that can significantly impact your insurance premiums. By understanding and proactively improving your credit profile, you can potentially unlock more favorable insurance rates across multiple coverage types.

Strategic Credit Score Improvement Techniques

Improving your credit score requires consistent financial discipline and targeted strategies. Insurers assess these indicators when calculating risk and determining premium structures. Key techniques include:

- Making consistent and timely bill payments

- Maintaining low credit utilization ratios

- Regularly monitoring credit reports for accuracy

- Avoiding unnecessary credit applications

- Reducing outstanding debt levels

The South African Credit and Risk Reporting Association emphasizes the importance of understanding how financial behaviors influence credit ratings.

Practical Credit Management Approaches

Effective credit score management involves more than just paying bills on time. Developing a comprehensive financial strategy can help you systematically improve your creditworthiness. This might include consolidating debts, negotiating payment plans, and creating a structured budget.

To help consumers optimize their financial strategies, check out our top tips for cheaper car insurance to understand how credit scores interact with insurance pricing.

Ultimately, your credit score is a powerful financial tool that requires consistent attention and strategic management. By implementing these approaches, you can potentially reduce insurance premiums and enhance your overall financial health.

Take Control of Your Credit Score and Pay Less for Insurance

Have you ever felt frustrated by high insurance premiums, even though you try your best to manage your money? As uncovered in our guide to understanding the interaction between insurance and your credit score, your credit history can directly affect what you pay for cover. Many South Africans don’t realise that improving your credit score can lead to real savings on car, home, and even cellphone insurance. Financial decisions today can open the door to better premiums and peace of mind tomorrow.

Now is the perfect time to put knowledge into action. Visit King Price Insurance for practical insurance tips and tricks, trusted coverage for your car or home, and straight answers to your questions about how credit affects your policy. Don’t let your credit score hold your wallet back. Compare options and see how affordable reliable cover can be when you build your financial foundation soundly. Take the first step to smarter insurance choices right now.

Frequently Asked Questions

What is a credit score and how is it calculated?

A credit score is a numerical representation of an individual’s financial trustworthiness, ranging between 300 and 850. It is calculated using factors such as payment history, total debt levels, credit utilization, length of credit history, and types of credit accounts.

How do credit scores impact insurance premiums?

Credit scores significantly influence insurance premiums as they act as a risk assessment tool. Higher credit scores often lead to lower insurance premiums because they are associated with lower claim probabilities and responsible financial management.

Why do insurance companies use credit scores?

Insurance companies use credit scores to predict the potential risk of policyholders filing claims. A strong credit score suggests that an individual is financially responsible, which correlates with fewer claims and lower risks for the insurer.

What strategies can I use to improve my credit score for better insurance rates?

To improve your credit score, consistently make timely payments, maintain low credit utilization ratios, monitor credit reports for accuracy, avoid excessive credit applications, and work to reduce outstanding debt levels.