Everyone feels the pinch when their car insurance goes up and you might think it is out of your control. Here is what stops most people in their tracks: a single serious traffic violation can push your premium up by as much as 50 percent. That is not even the biggest driver of price hikes for 2025 since global part shortages and inflation are reshaping what you pay before you even get behind the wheel.

Table of Contents

- Factors That Cause Car Insurance Increases

- How Tariffs And Repairs Impact Premiums

- Personal Habits That Can Raise Insurance Costs

- Tips To Reduce Your Car Insurance Premium

Quick Summary

| Takeaway | Explanation |

|---|---|

| Economic factors drive premium increases | Inflation and rising repair costs necessitate higher insurance rates. Insurers adjust premiums to cover potential expenses associated with repairs and medical claims. |

| Claim frequency leads to higher rates | More frequent accidents and escalating medical costs result in increased insurance premiums. Insurers adjust rates based on claim frequency and severity patterns. |

| Personal habits influence insurance costs | Driving behavior, credit ratings, and lifestyle choices can significantly impact premiums. Safe driving and good credit can lead to lower insurance expenses. |

| Utilize discounts to lower premiums | Explore bundling policies, completing defensive driving courses, and installing safety devices for potential discounts. These actions can significantly reduce your insurance costs. |

| Review and adjust your policy regularly | Periodically evaluate your coverage and deductibles to ensure you’re not overpaying. Raising deductibles can also lower monthly premiums. |

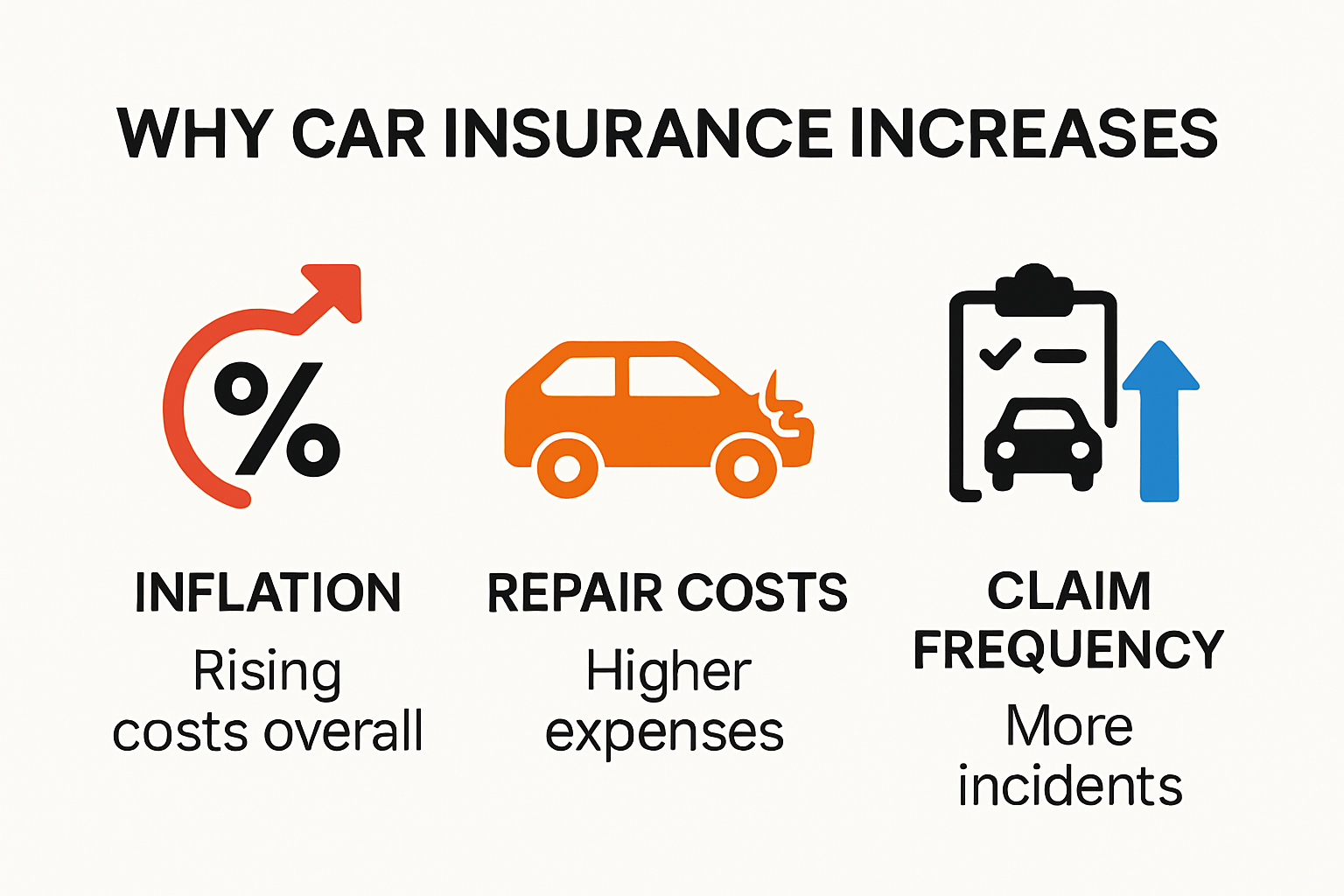

Factors That Cause Car Insurance Increases

Understanding why car insurance increases is crucial for vehicle owners seeking to manage their financial responsibilities. The landscape of car insurance pricing is complex, with multiple interconnected factors driving rate escalations in 2025.

Economic Pressures and Inflation

The National Association of Insurance Commissioners reports that inflation directly impacts insurance premiums. As the cost of vehicle repairs, replacement parts, and medical treatments rises, insurers must adjust their rates to cover potential claim expenses.

Vehicle repair costs have become increasingly expensive due to advanced automotive technologies. Modern cars feature sophisticated electronic systems, sensors, and computerized components that significantly increase repair expenditures. A simple bumper replacement that might have cost R5,000 in previous years could now require R15,000 due to integrated sensors and complex repair processes.

Claim Frequency and Severity

Insurance companies closely monitor claim patterns to determine premium adjustments. The Insurance Information Institute highlights that both the frequency and severity of claims contribute to rate increases. Factors influencing claim trends include:

- Increased Accident Rates: Higher traffic volumes and more complex road conditions lead to more frequent accidents.

- Rising Medical Expenses: Medical treatment costs continue to escalate, making bodily injury claims more expensive.

- Technological Repair Complexities: Advanced vehicle technologies make repairs more intricate and costly.

These claim-related factors directly impact insurers’ risk assessments and pricing models. When claim payouts increase, insurance companies must adjust premiums to maintain financial stability.

Risk Assessment and Technological Innovations

Modern risk assessment techniques have become more sophisticated, allowing insurers to develop more precise pricing models. While this can benefit some drivers, it also means that individual risk factors are scrutinized more closely. Factors such as driving history, vehicle type, geographical location, and even credit scores can influence insurance rates.

Technological innovations like telematics and usage-based insurance are transforming how insurers evaluate risk. Learn more about how car premiums are calculated to understand these emerging assessment methods.

Additionally, external factors such as increased extreme weather events, higher crime rates in certain areas, and global economic uncertainties contribute to the complex pricing environment. Insurers must continuously adapt their models to manage potential financial risks effectively.

Understanding these factors can help vehicle owners make informed decisions about their insurance coverage and potentially mitigate some rate increases through proactive measures like maintaining a clean driving record, choosing vehicles with lower repair costs, and exploring available discounts.

Below is a summary table outlining the main factors contributing to car insurance increases for 2025. Use this as a quick reference to understand what is driving your premium upward.

| Factor Category | Specific Drivers | Impact on Premiums |

|---|---|---|

| Economic Pressures | Inflation, rising repair & medical costs | Increases due to costlier payouts & claims |

| Claim Frequency & Severity | More accidents, higher claim values | Raises rates to offset insurer loss risks |

| Repair Complexity | Technology, sensors, advanced parts | Costlier fixes increase policy costs |

| Tariffs & Parts Costs | Import taxes, global supply chain | Higher parts costs passed to consumers |

| Personal Risk Profile | Driving record, credit, high-risk habits | Directly affects individual premiums |

| External Risks | Extreme weather, local crime | Affects area and vehicle-specific rates |

How Tariffs and Repairs Impact Premiums

The intricate relationship between tariffs, vehicle repairs, and insurance premiums represents a complex economic landscape that directly influences car insurance costs in 2025. Understanding these interconnected factors reveals why insurance rates continue to climb.

Global Trade and Vehicle Part Costs

The Boston Consulting Group reveals that over half of vehicle parts are imported, creating significant cost pressures for insurers. Tariffs on imported automotive components create a cascading effect that ultimately impacts car insurance premiums. When trade barriers increase, the cost of replacement parts rises exponentially, forcing insurance companies to adjust their pricing models.

Imported vehicle components face multiple taxation layers, which compound their overall expense. A simple replacement part might traverse several international borders, accumulating tariffs at each stage. According to PwC, a 25% tariff could potentially result in billions of dollars in additional costs, directly translating to higher insurance premiums for consumers.

Complex Repair Ecosystem

Modern vehicles feature increasingly sophisticated technological systems that complicate repair processes. Electronic components, advanced sensors, and integrated computer systems make repairs more expensive and technically challenging. These technological advancements mean that even minor damages can require extensive and costly interventions.

The American Academy of Actuaries emphasizes the complexity of “tariff stacking,” where parts crossing multiple borders accumulate additional taxation. This intricate process significantly increases the baseline cost of repairs, compelling insurers to adjust their premium calculations.

Strategic Pricing Adaptations

Insurance providers must continuously adapt their pricing strategies to manage escalating repair costs. This involves developing more nuanced risk assessment models that account for technological complexity, global trade dynamics, and potential tariff fluctuations.

Explore how insurers calculate premiums in this evolving landscape to understand the intricate mechanisms driving insurance pricing.

Key considerations for insurers include:

- Technological Complexity: Advanced vehicle systems increase repair costs

- Global Supply Chain Dynamics: Tariffs and international trade regulations impact part prices

- Risk Management: Developing adaptive pricing models to maintain financial stability

Consumers can mitigate some of these cost increases by choosing vehicles with lower repair costs, maintaining comprehensive service records, and exploring insurance options that offer more flexible pricing structures. Understanding these underlying economic factors helps drivers make more informed decisions about their vehicle insurance investments.

Personal Habits That Can Raise Insurance Costs

While many drivers are unaware, personal lifestyle choices and individual behaviors can significantly impact car insurance premiums. Understanding how insurers assess personal risk can help individuals make more informed decisions about their coverage and potential cost reductions.

Driving Behavior and Risk Profile

Forbes Advisor reveals that personal driving habits are among the most critical factors influencing insurance rates. Traffic violations, accident history, and driving frequency create a comprehensive risk profile that insurers use to calculate premiums.

Drivers with multiple speeding tickets, at-fault accidents, or a history of reckless driving can expect substantially higher insurance costs. Insurance companies view these behaviors as indicators of potential future claims. A single serious traffic violation can increase premiums by up to 50%, demonstrating the significant financial impact of driving behavior.

Lifestyle and Personal Characteristics

Insure.com highlights that personal characteristics beyond driving record play a crucial role in insurance pricing. Marital status, for instance, can influence insurance rates. Married individuals often receive lower premiums, as statistical data suggests they are less likely to be involved in accidents.

Additionally, factors such as credit score can dramatically affect insurance costs. The Massachusetts government notes that insurers use credit-based insurance scores to predict claim likelihood. Individuals with lower credit scores may face higher premiums, reflecting the perceived financial risk.

High-Risk Activities and Personal Choices

Certain lifestyle choices can unexpectedly impact insurance rates. Engaging in high-risk activities such as extreme sports, frequent long-distance driving, or working in high-risk professions can trigger premium increases. Insurers assess these factors as potential indicators of increased accident probability.

Learn strategies for reducing your insurance costs to mitigate the impact of personal risk factors.

Key personal habits that can raise insurance costs include:

- Frequent Traffic Violations: Speeding tickets and reckless driving

- Poor Credit History: Lower credit scores indicating financial instability

- High-Risk Lifestyle Choices: Participating in dangerous activities

- Irregular Driving Patterns: Inconsistent or high-mileage driving

The following summary table highlights how personal habits and characteristics impact your car insurance premiums. Use it to assess your own risk factors and identify areas for improvement.

| Habit or Characteristic | How It Impacts Premiums |

|---|---|

| Frequent traffic violations | Raises premiums, up to 50% for serious offences |

| Poor credit history | Higher perceived risk, increases costs |

| High-risk activities | Triggers higher rates due to greater claim probability |

| At-fault accident history | Seen as risky, leads to higher premiums |

| High driving frequency | More on road = higher risk, increases rates |

| Marital status (single) | Singles generally pay more than married |

Drivers can take proactive steps to manage their insurance costs by maintaining a clean driving record, improving credit scores, and demonstrating responsible behavior. Regular defensive driving courses, maintaining continuous insurance coverage, and choosing vehicles with lower risk profiles can help mitigate potential premium increases.

Understanding the intricate relationship between personal habits and insurance pricing empowers drivers to make more strategic decisions about their coverage and potentially reduce their financial burden.

Tips to Reduce Your Car Insurance Premium

Navigating the complex world of car insurance requires strategic thinking and proactive approaches to manage escalating premiums. By understanding and implementing targeted strategies, drivers can effectively mitigate the financial burden of increasing insurance costs.

Strategic Policy Management

The National Association of Insurance Commissioners recommends several key strategies for reducing car insurance premiums. One fundamental approach involves carefully evaluating and adjusting your current insurance policy. This means critically examining your coverage levels, deductibles, and potential unnecessary add-ons that might be inflating your monthly payments.

Raising your deductible is a proven method to lower monthly premiums. By agreeing to pay a higher out-of-pocket expense in the event of a claim, insurers typically reward policyholders with reduced rates. However, it is crucial to ensure you can comfortably afford the higher deductible if an accident occurs.

Vehicle and Personal Risk Management

The Insurance Information Institute emphasizes the importance of managing personal and vehicular risk factors. Installing additional safety devices such as advanced alarm systems, GPS trackers, and dashboard cameras can potentially qualify you for insurance discounts. Modern insurers increasingly value proactive risk mitigation.

Drivers can also explore usage-based insurance programs that track driving behavior. These innovative policies use telematics technology to monitor driving habits, rewarding safe drivers with lower premiums. Factors like smooth acceleration, consistent speed, and avoiding late-night driving can translate into meaningful cost savings.

Comprehensive Discount Strategies

Discover comprehensive strategies for reducing your insurance expenses to maximize your potential savings.

Key strategies for reducing car insurance premiums include:

- Bundle Policies: Combine auto insurance with home or other insurance for potential discounts

- Maintain Good Credit: Improve credit scores to potentially lower insurance rates

- Complete Defensive Driving Courses: Earn certifications that demonstrate reduced risk

- Review Annual Mileage: Lower annual driving distances can result in reduced premiums

Additionally, consider these nuanced approaches:

- Compare quotes from multiple insurers annually

- Ask about professional or membership-based discounts

- Consider the insurance cost before purchasing a new vehicle

- Maintain a clean driving record

Below is a checklist table summarising actionable steps you can implement to reduce your car insurance premium according to the strategies covered above.

| Strategy | Action Item | Benefit |

|---|---|---|

| Policy Management | Review/adjust policy, raise deductible | Lowers monthly payment potential |

| Risk Management | Install safety devices, use telematics | Can result in policy discounts |

| Discount Strategies | Bundle insurance, complete defensive driving course | Additional savings on premium |

| Credit Score | Maintain/improve credit | Lowers insurance expense |

| Mileage Review | Track and reduce annual kilometres | Lowers risk, saves money |

| Compare Offers | Shop around annually | Potential for best rate |

Drivers should approach insurance as a dynamic financial product, regularly reassessing their needs and exploring opportunities for optimization. By staying informed, proactive, and strategic, individuals can effectively manage and potentially reduce their car insurance expenses in an increasingly complex insurance landscape.

Remember that while cost is important, comprehensive coverage that adequately protects you remains the ultimate goal. Balance cost-saving strategies with ensuring sufficient protection for your specific driving circumstances.

Frequently Asked Questions

What causes car insurance premiums to increase in 2025?

Economic pressures such as inflation, rising repair costs, increased claim frequency, and stricter risk assessments are the main drivers of car insurance premium increases in 2025.

How does my driving behaviour affect my car insurance rates?

Your driving behaviour significantly impacts your insurance rates. Traffic violations, accident history, and overall driving frequency are critical factors that insurers consider when calculating premiums. A single serious violation can lead to a 50% increase in your premium.

Can I reduce my car insurance premium?

Yes, you can reduce your car insurance premium by raising your deductible, maintaining a good credit score, bundling your insurance policies, and taking defensive driving courses to qualify for discounts.

How do global trade issues affect car insurance costs?

Global trade issues can increase the cost of vehicle parts due to tariffs and import taxes, ultimately affecting car insurance premiums as insurers adjust their rates to cover higher repair costs.

Take Control of Your Rising Car Insurance Costs in 2025

Feeling anxious about increasing car insurance premiums in South Africa? You are not alone. This year, many drivers are worried as economic pressures, expensive repairs, and personal factors all combine to drive premiums higher. From unexpected claims to new risk assessment methods, these challenges put extra pressure on your wallet and peace of mind.

It is time to protect your finances and put yourself back in the driver’s seat. Explore expert advice and simple solutions designed for South Africans. Discover cost-saving tips with insurance tips and tricks in South Africa and arm yourself with real strategies to reduce your premium. If you are looking for extra savings or want to compare your options with confidence, visit the King Price Car Insurance page for clear answers and quick online quotes. Do not let rising insurance costs catch you off guard. Head to insurance.kingprice.co.za now and secure cover that puts your needs first.