Owning a swimming pool can turn any backyard into a summer paradise and instantly boost your home’s value and appeal. But surprisingly, that sparkling blue water also brings a hefty dose of hidden costs and legal headaches. Most homeowners do not realise that their insurance premiums can jump by as much as 25 percent once a pool enters the picture, and standard policies often fall short when it comes to real protection. The real shock comes when you discover just how crucial it is to rethink your cover, or risk huge financial fallout from a single poolside accident.

Table of Contents

- How Pools Affect Your Current Insurance

- Key Risks And Coverage For Pool Owners

- Tips For Lower Premiums And Safer Pools

Quick Summary

| Takeaway | Explanation |

|---|---|

| Increase liability coverage for pools | Standard homeowners policies may not cover pool-related incidents adequately, so enhancing coverage is essential. |

| Implement safety features to reduce rates | Installing secure fencing and alarms can lower insurance premiums and enhance safety. |

| Consider umbrella policies for extra protection | An umbrella policy provides additional liability coverage beyond standard limits, crucial for pool incidents. |

| Regularly maintain and inspect your pool | Routine maintenance can prevent accidents and demonstrate responsible ownership, which insurers appreciate. |

| Review insurance options periodically | Comparing quotes and coverage ensures that your insurance remains effective and cost-efficient over time. |

How Pools Affect Your Current Insurance

Owning a swimming pool transforms your home landscape and introduces significant insurance considerations that many homeowners overlook. Swimming pools represent more than just a recreational feature they fundamentally alter your property’s risk profile and insurance requirements.

Liability Risks and Insurance Coverage

Swimming pools dramatically increase potential liability exposure for homeowners. The Insurance Information Institute highlights that pools create substantial legal risks related to potential accidents and injuries. Individuals who suffer harm on or near your pool could potentially file claims against you, making comprehensive liability protection critical.

Homeowners must understand that standard home insurance policies often provide limited protection for pool-related incidents. You might need to significantly increase your liability coverage to adequately protect yourself financially. Typical scenarios requiring enhanced coverage include:

- Accidental drowning: Tragic incidents that could result in massive legal claims

- Slip and fall accidents: Injuries occurring around pool areas

- Child safety incidents: Potential legal challenges if proper safety measures are not implemented

Safety Requirements and Insurance Implications

The National Association of Insurance Commissioners emphasizes that insurers have specific safety requirements for properties with swimming pools. Insurance providers typically mandate:

- Secure fencing around the entire pool perimeter

- Self-closing and self-latching gates

- Minimum fence height specifications

- Clear safety signage

- Proper pool covers when not in use

Failing to meet these safety standards could result in increased premiums or potential policy cancellation. Insurers view pools as high-risk assets that require stringent safety protocols to mitigate potential accidents.

Additional Insurance Considerations

Beyond standard homeowners insurance, pool owners should consider supplemental coverage options. An umbrella insurance policy can provide additional liability protection extending beyond traditional home insurance limits. This extra layer of financial protection becomes crucial when facing potential legal claims related to pool incidents.

Insurance premiums for homes with pools typically increase between 10% to 25%, reflecting the elevated risk profile. Homeowners should proactively discuss their pool with their insurance provider, ensuring comprehensive coverage that addresses unique swimming pool related risks.

While pools offer tremendous recreational value, they simultaneously introduce complex insurance considerations. Responsible pool ownership means understanding and mitigating potential financial risks through appropriate insurance strategies.

Key Risks And Coverage For Pool Owners

Pool ownership introduces a complex landscape of potential risks that extend far beyond simple recreational enjoyment. Understanding these risks is crucial for homeowners to protect themselves financially and legally.

Comprehensive Liability Exposures

The Centers for Disease Control and Prevention reveals that drowning remains a significant risk, with residential pools being primary locations for potential accidents. Pool owners face substantial liability risks that can emerge from various scenarios. These risks are not limited to direct swimming incidents but encompass a broader range of potential legal challenges.

Key liability exposures include:

- Unauthorized entry accidents: Incidents involving individuals who enter the pool area without permission

- Child safety incidents: Potential legal claims related to inadequate supervision or safety measures

- Structural failure risks: Damages resulting from pool equipment malfunction or structural defects

Insurance Coverage Strategies

The Insurance Information Institute emphasizes that standard homeowners insurance provides limited protection for pool-related incidents. Pool owners need strategic approaches to comprehensive coverage. This often involves:

- Increasing standard liability coverage limits

- Purchasing additional umbrella insurance policies

- Implementing rigorous safety protocols to mitigate potential risks

Insurers typically assess multiple factors when determining coverage for pool owners, including:

- Pool type (in-ground vs above-ground)

- Safety features

- Surrounding landscape

- Proximity to residential structures

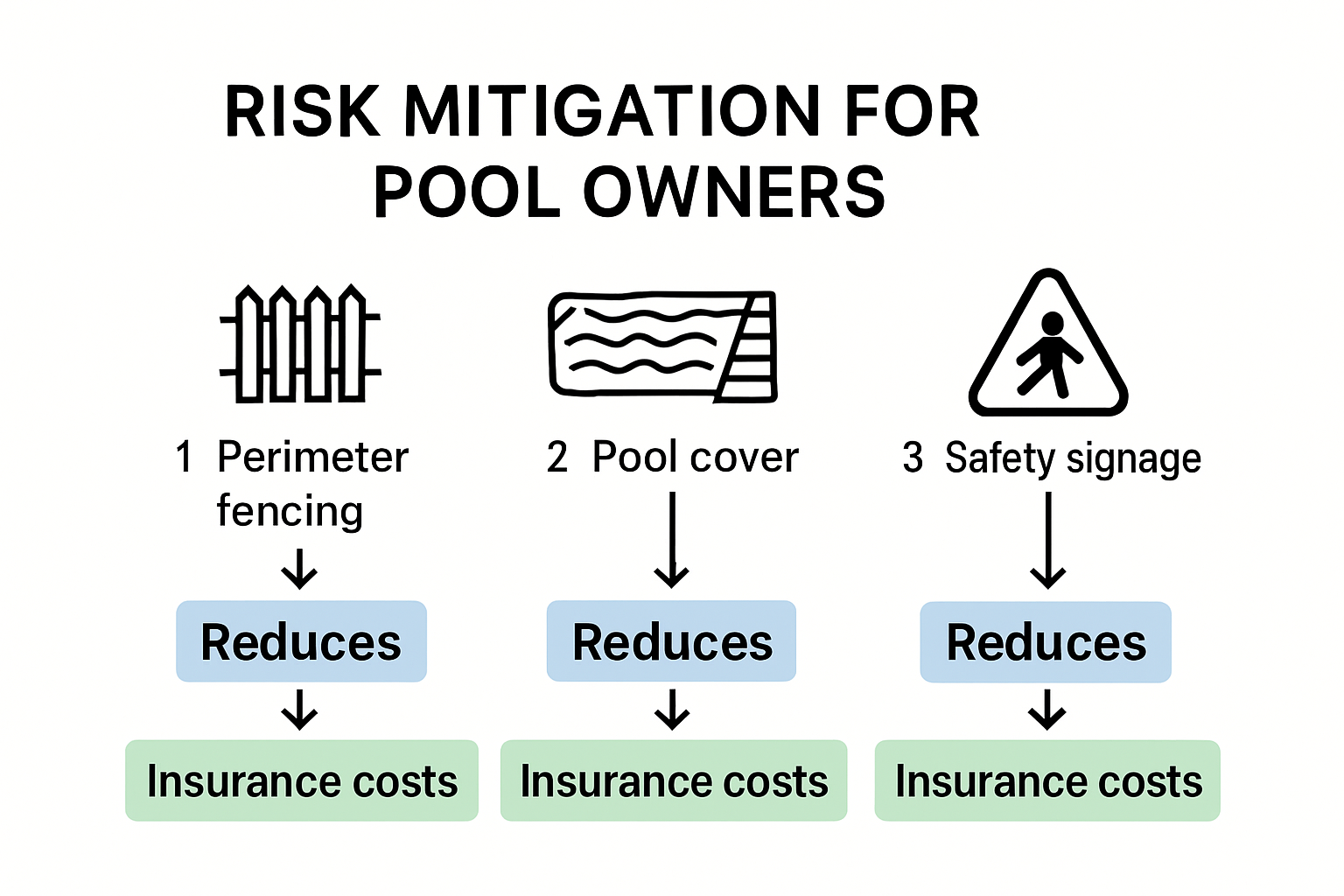

Risk Mitigation Techniques

The National Association of Insurance Commissioners recommends proactive risk management strategies for pool owners. These strategies go beyond insurance and focus on preventing potential incidents. Key risk mitigation techniques include:

- Installing high-quality perimeter fencing

- Implementing automatic pool covers

- Maintaining clear safety signage

- Regular equipment maintenance

- Professional safety inspections

Pool owners should understand comprehensive insurance options that provide robust protection. While pools offer recreational enjoyment, they simultaneously introduce significant financial and legal complexities. Responsible ownership means understanding these risks and implementing comprehensive protective strategies.

Statistically, pools increase homeowners insurance premiums by 10% to 25%, reflecting the elevated risk profile. Proactive communication with insurance providers and continuous risk assessment are essential for maintaining appropriate coverage and protecting your financial interests.

To clarify the main risk exposures, safety requirements, and premium impacts, here is a summary table bringing together these frequently mentioned elements:

| Risk, Requirement or Factor | Description/Impact | Typical Result/Implication |

|---|---|---|

| Pool installation | Adds recreational value, but raises liability exposure | Premium up 10–25% |

| Secure fencing | Physical barrier, usually a legal/insurance requirement | Reduces liability, may lower premium |

| Accidental drowning risk | Leading pool-related fatality, especially for children | Need increased liability coverage |

| Slip and fall accidents | Possible on slippery or wet decking around pool | Risk of claims, may need extra cover |

| Non-slip pool surrounds | Safety feature to prevent falls | Can reduce insurance risk |

| Umbrella policy | Extra liability cover that sits above standard home policy | Essential for higher payouts/claims |

| Documented maintenance & inspection | Keeps pool safe, demonstrates owner responsibility | Could influence insurer’s rates |

Tips for Lower Premiums and Safer Pools

Pool ownership requires strategic planning to balance safety and insurance affordability. Homeowners can implement multiple approaches to reduce insurance risks and potentially lower their premium costs.

Strategic Safety Installations

The Insurance Information Institute emphasizes that proactive safety measures directly impact insurance assessments. Critical safety installations can significantly reduce potential liability and insurance premiums. Recommended safety investments include:

- Four-sided perimeter fencing: Minimum four-foot height with self-closing gates

- Automatic pool covers: Preventing unauthorized access

- Alarm systems: Detecting unexpected pool area entry

- Non-slip decking: Reducing potential accident risks

Insurers assess these safety features carefully, often providing premium discounts for comprehensive protective measures. The initial investment in safety infrastructure can translate into long-term financial savings.

Below is a checklist-style table outlining essential steps and features for safer, more insurable pools, as discussed in this section:

| Safety Measure or Action | Purpose/Benefit | Insurance Impact |

|---|---|---|

| Four-sided perimeter fencing | Prevents unauthorised pool access | May reduce premium |

| Automatic pool cover | Restricts pool access when not in use | May reduce premium |

| Alarm system for pool area | Alerts to any unexpected entry | May reduce premium |

| Non-slip decking | Reduces risk of slips and falls | Safer environment |

| Documented professional equipment checks | Ensures all components function safely | Shows responsibility |

| Clear safety signage | Warns and educates pool users | Safer environment |

| Emergency protocol & supervision | Quickly addresses incidents | Demonstrates best practice |

Risk Reduction Strategies

Beyond physical installations, pool owners can implement comprehensive risk management strategies. Professional safety training and documented maintenance protocols demonstrate responsible ownership to insurance providers. Key strategies include:

- Regular professional pool equipment inspections

- Documented safety training for household members

- Maintaining clear emergency protocols

- Keeping detailed maintenance records

- Implementing strict supervision guidelines

Explore comprehensive insurance strategies that can help pool owners navigate complex liability landscapes. Understanding how insurers evaluate risk allows for more informed decision-making.

Financial Planning for Pool Insurance

Effective pool ownership requires understanding potential financial implications. Homeowners should consider:

- Requesting multiple insurance quotes

- Comparing coverage options

- Exploring umbrella liability policies

- Understanding specific pool-related coverage limitations

- Regularly reviewing and updating insurance provisions

Statistically, implementing comprehensive safety measures can reduce insurance premiums by 10% to 25%. Proactive risk management transforms pools from potential liability concerns into manageable recreational assets.

Responsible pool ownership means balancing enjoyment with strategic financial and safety planning. By understanding insurance complexities and implementing robust protective measures, homeowners can create a safer environment while potentially reducing their insurance costs.

Frequently Asked Questions

How does owning a pool affect my home insurance premiums?

Owning a swimming pool can increase your home insurance premiums by as much as 10% to 25% due to the added liability risks associated with pool ownership.

What types of insurance coverage do pool owners need?

Pool owners typically need to enhance their liability coverage, consider umbrella policies for additional protection, and ensure their standard homeowners insurance adequately covers pool-related incidents.

What safety measures can I put in place to lower my insurance premiums?

Implementing safety features such as secure fencing, self-closing gates, automatic pool covers, and non-slip decking can reduce both the risk of accidents and your insurance premiums.

Why is regular maintenance important for pool insurance?

Regular maintenance demonstrates responsible ownership and can prevent accidents, which may help lower your insurance rates and ensure you meet any requirements set by your insurance provider.

Is Your Pool Protected The Way It Should Be

Building the dream of a home pool comes with worries that can keep any South African homeowner up at night. The risks of accidental injury, higher insurance premiums and the strict requirements from insurance providers are real challenges. Many discover too late that standard cover just does not cut it once your backyard becomes a playground. From slip and fall claims to loss caused by lack of proper fencing or maintenance, leaving these gaps in your cover can cost you more than you bargained for.

Do not settle for hidden financial shocks or uncertainty. At insurance.kingprice.co.za, we specialise in helping South Africans secure the right protection for their unique home needs. Find advice on how your swimming pool impacts homeowners insurance, learn about umbrella liability solutions, and request a quote that matches your risk profile. Take charge of your peace of mind now by exploring your options and making your pool a safe asset, not a costly hazard.

Recommended

- Insurance for Rental Property in 2025: What Owners Need to Know – Savvy Insurance

- How to Avoid Underinsurance: Tips for SA Car and Home Owners 2025 – Savvy Insurance

- Annual Insurance Review Tips for Car and Home Owners 2025 – Savvy Insurance

- Insurance for New Drivers: Best Tips and Options 2025 – Savvy Insurance