A lot of South Africans are still driving without car insurance, with a whopping 65 percent of motorists remaining completely uninsured. Now here’s the wild part. While our law does not force everyone to get car insurance, the fallout when things go wrong is far worse than most people think. Before you take that next drive, see how one crash can ruin your finances for years and why skipping that insurance payment could cost more than you bargained for.

Table of Contents

- Legal Penalties Of Driving Uninsured

- Financial Consequences For Car And Home Owners

- Personal Liability And Accident Responsibilities

- How No Insurance Impacts Your Future Coverage

Quick Summary

| Takeaway | Explanation |

|---|---|

| Financial Liability Risks | Uninsured drivers can face overwhelming personal financial responsibility for all damages in accidents, leading to potential bankruptcy or long-term debt. |

| Legal Consequences of Uninsured Driving | Although not illegal in South Africa, driving uninsured can result in severe penalties, including license suspension and civil lawsuits for damages, creating significant long-term legal vulnerabilities. |

| Impact on Future Insurance Rates | Uninsured drivers are categorized as high-risk, resulting in substantially higher insurance premiums and difficulties acquiring coverage in the future, creating a long-lasting financial burden. |

| Psychological and Emotional Strain | The uncertainty and stress associated with potential lawsuits and financial repercussions from uninsured driving can lead to significant emotional distress that extends beyond the accident. |

| Comprehensive Coverage as Essential Protection | Investing in car insurance is crucial for financial protection, as it transforms potential financial catastrophes into manageable challenges, ensuring long-term economic stability. |

Legal Penalties of Driving Uninsured

Driving without car insurance exposes drivers to substantial legal and financial risks that can devastate personal finances and future driving opportunities. While South Africa does not legally mandate car insurance, the consequences of being uninsured extend far beyond simple monetary penalties.

Financial Liability and Personal Risk

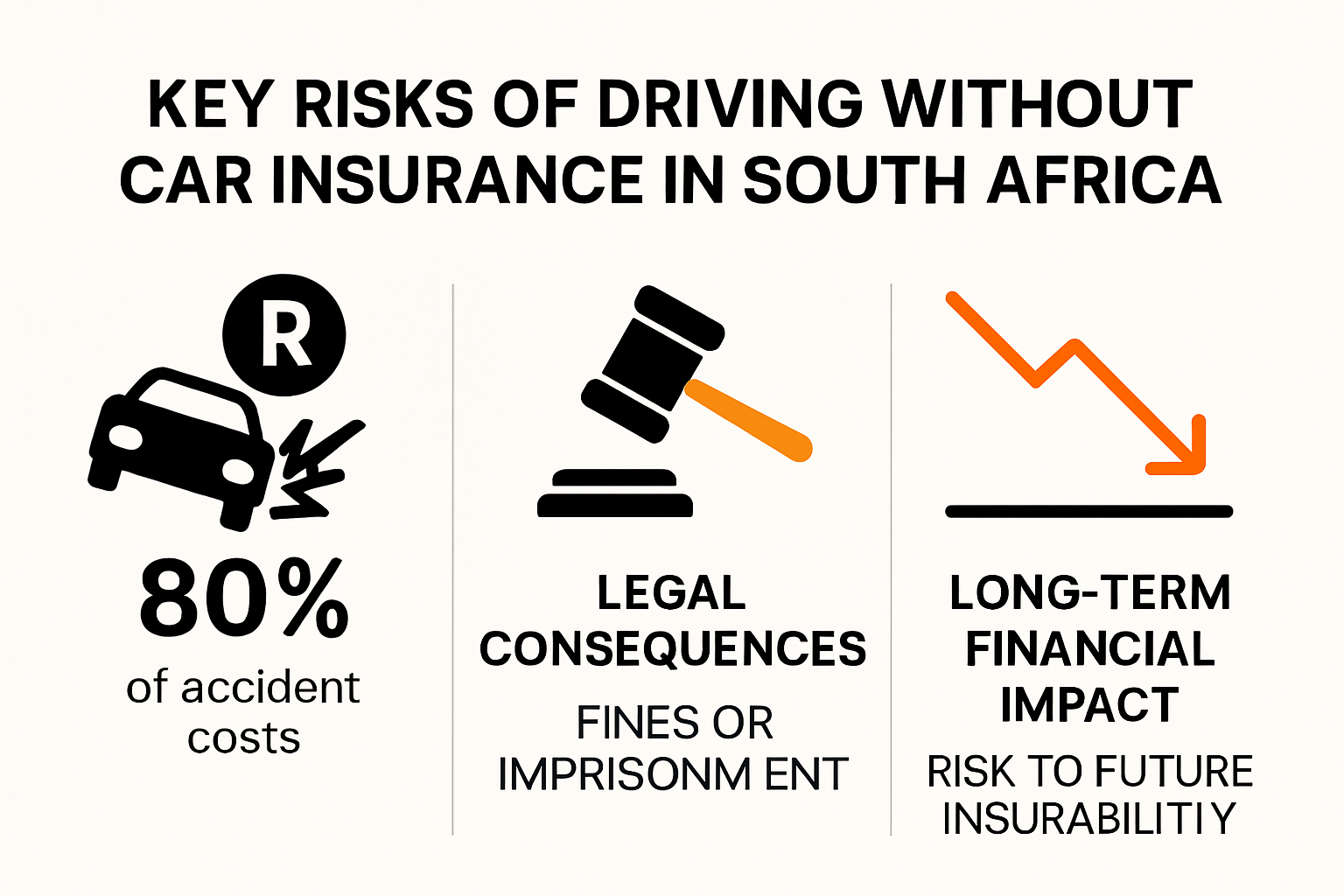

Uninsured drivers face overwhelming financial vulnerability in accident scenarios. The Automobile Association reports that approximately 65% of South African motorists remain uninsured, leaving themselves exposed to potentially catastrophic financial consequences. When an uninsured driver is involved in an accident, they become personally responsible for all repair costs, medical expenses, and potential legal claims.

The financial implications can be staggering. A single serious accident could result in repair costs ranging from tens of thousands to hundreds of thousands of rand. Without insurance coverage, these expenses must be paid directly out of pocket, potentially leading to personal bankruptcy or long-term debt. Moreover, if the uninsured driver is found legally at fault, they may face additional civil litigation from injured parties seeking compensation.

Legal Consequences and Potential Prosecution

Beyond financial risks, uninsured drivers confront significant legal challenges. The Arrive Alive campaign emphasizes that South Africa’s high accident and car theft rates make driving without insurance an extremely risky proposition. While not technically illegal, being uninsured creates substantial legal vulnerabilities.

Law enforcement and judicial systems can impose severe penalties on uninsured drivers involved in accidents. These may include:

- License Suspension: Drivers might face temporary or permanent license revocation

- Legal Proceedings: Potential criminal charges for negligence

- Asset Seizure: Courts could authorize seizure of personal assets to cover damages

- Increased Future Insurance Premiums: Insurers often charge significantly higher rates for drivers with uninsured accident histories

Long-Term Consequences of Uninsured Driving

The repercussions of driving without insurance extend beyond immediate legal and financial penalties. According to prabhhonda.com, recent regulatory changes in 2025 have increased penalties for traffic-related offenses, signaling a more stringent approach to road safety and driver accountability.

Uninsured drivers may find themselves permanently branded as high-risk, making future insurance acquisition challenging and expensive. Insurance providers typically maintain extensive databases tracking driver histories, and a record of uninsured driving can result in lifelong financial penalties through dramatically increased insurance premiums.

Moreover, the personal stress and potential legal complications can have profound psychological impacts. The uncertainty of potential lawsuits, financial ruin, and legal proceedings can create significant emotional strain that extends far beyond the initial incident.

While car insurance is not legally mandatory in South Africa, the risks of driving uninsured are overwhelmingly clear. Protecting oneself with comprehensive insurance coverage represents a critical financial and legal safeguard against unpredictable road incidents.

Financial Consequences for Car and Home Owners

Uninsured car and home owners face devastating financial risks that extend far beyond simple property damage. The potential economic impact of operating without proper insurance coverage can transform a single incident into a potentially catastrophic financial disaster.

Direct Financial Exposure in Vehicle Incidents

The financial vulnerability of uninsured motorists becomes dramatically apparent during accidents. According to BusinessLive, uninsured drivers may encounter substantial out-of-pocket expenses that can quickly escalate into financial hardship. A single moderate vehicle accident could generate repair costs ranging from R50,000 to R250,000, depending on the vehicles involved.

These expenses do not merely encompass vehicle repairs. Uninsured drivers might also become personally liable for medical expenses, property damage, and potential legal fees if they are found at fault. The Automobile Association highlights that approximately 65% of South African motorists remain uninsured, exposing themselves to significant financial risk with every journey.

Below is a summary table highlighting the potential expenses uninsured drivers face in a single accident scenario:

A summary table highlighting major financial risks faced by uninsured vehicle owners in the event of an accident:

| Expense Type | Description | Potential Cost Range |

|---|---|---|

| Vehicle Repairs | Out-of-pocket repair or replacement of own vehicle | R50,000 – R250,000 |

| Medical Costs | Hospital, treatment, or rehabilitation for any injury | Tens to hundreds of thousands of rand |

| Third-Party Damages | Compensation for damage to other party’s vehicle/property | Varies; potentially substantial |

| Legal Fees | Court and representation costs in case of lawsuit | Varies, may exceed R50,000 |

| Asset Seizure | Potential loss of property to cover awarded damages | Value of seized assets |

Compounding Economic Challenges

Beyond immediate accident-related expenses, uninsured car and home owners face additional economic complications. FAnews reports that the prevalence of uninsured vehicles contributes to higher insurance premiums for responsible, insured drivers. This creates a cascading economic effect where responsible policy holders ultimately bear the financial burden of systemic uninsured risk.

Moreover, being uninsured can create long-term financial repercussions. Insurance providers typically categorize previously uninsured individuals as high-risk, which translates into significantly elevated future insurance rates. For many car and home owners, this means potentially paying substantially higher premiums for years following an uninsured incident.

Comprehensive Protection Strategy

Navigating the complex landscape of insurance requires strategic planning. While the immediate cost of insurance might seem burdensome, the potential financial devastation of remaining uninsured far outweighs these expenses. Learn more about protecting your financial future with comprehensive coverage.

Homeowners face similar risks. Uninsured property damage from natural disasters, theft, or accidents can result in complete financial loss. The cost of rebuilding or replacing a home without insurance can easily run into hundreds of thousands of rand, potentially destroying years of financial investment and personal savings.

The economic wisdom is clear: comprehensive insurance is not an expense, but a critical financial protection mechanism. By investing in proper coverage, car and home owners transform potential financial catastrophes into manageable challenges, safeguarding their economic stability and peace of mind.

Personal Liability and Accident Responsibilities

Uninsured drivers face profound personal liability challenges that extend far beyond simple vehicle damage. The legal and financial responsibilities following an accident can transform a momentary incident into a life-altering financial catastrophe.

Legal Responsibility in Accident Scenarios

When uninsured drivers are involved in accidents, they become entirely responsible for all resulting damages and potential legal consequences. According to Arrive Alive, uninsured motorists are personally liable for repairs to their own vehicle, damages to other vehicles, and potential medical expenses for injured parties.

The legal implications can be staggering. If an uninsured driver is found at fault, they may face civil litigation seeking compensation for damages. This could include not just vehicle repair costs, but also medical treatments, lost wages for injured parties, and potential punitive damages. The Automobile Association reports that approximately 65% of South African motorists remain uninsured, exposing themselves to significant legal and financial risks with every journey.

Below is a summary table to clarify the responsibilities and consequences for uninsured drivers involved in an accident:

| Responsibility/Consequence | Description |

|---|---|

| Own Vehicle Repairs | Must pay all repair or replacement costs directly out-of-pocket |

| Third-Party Damages | Fully liable to compensate others for property and vehicle damage |

| Medical Expenses | Personally responsible for costs of medical treatment for self and possibly other parties |

| Legal Action | May be subject to lawsuits and court claims for recovery of damages |

| Asset Seizure | Risk losing personal property if unable to pay court-awarded damages |

| Liability for Civil Litigation | Recognized as high-risk, may face multiple claims in case of injuries & damages |

Financial Implications of Personal Liability

Personal liability in accident scenarios goes beyond immediate repair costs. Business Tech highlights the comprehensive financial exposure uninsured drivers face. A single serious accident could result in legal claims exceeding hundreds of thousands of rand, potentially leading to personal bankruptcy or long-term financial devastation.

The consequences extend to potential asset seizure. Courts may authorize the liquidation of personal assets to satisfy damages awarded in civil proceedings. This means uninsured drivers risk losing savings, property, and other valuable possessions to cover accident-related expenses.

Long-Term Legal and Financial Repercussions

Beyond the immediate aftermath of an accident, uninsured drivers face long-lasting legal challenges. Learn more about protecting yourself from comprehensive legal risks. Future insurance acquisition becomes significantly more difficult, with providers categorizing these individuals as high-risk drivers.

Moreover, the legal record of being an uninsured driver involved in an accident can impact employment opportunities, credit ratings, and personal reputation. Professional licenses, driving privileges, and future financial opportunities may be compromised by a single uninsured accident.

The personal responsibility of driving uninsured extends far beyond the road. It represents a comprehensive financial and legal risk that can potentially destroy years of personal and professional achievement. Comprehensive insurance is not merely a financial product but a critical shield protecting an individual’s entire economic future.

How No Insurance Impacts Your Future Coverage

The decision to drive without insurance creates a ripple effect that can dramatically reshape an individual’s future insurance landscape. What might seem like a short-term cost-saving measure can transform into a long-lasting financial burden with far-reaching consequences for future coverage and insurability.

Risk Profiling and Insurance Categorization

Insurance providers maintain comprehensive databases that track driver histories, creating detailed risk profiles for potential policyholders. According to BusinessLive, uninsured drivers who become involved in accidents are immediately categorized as high-risk individuals. This classification can persist for years, making future insurance acquisition challenging and significantly more expensive.

The Automobile Association highlights that approximately 65% of South African motorists remain uninsured, creating a systemic challenge for insurance providers. Insurers respond by implementing increasingly sophisticated risk assessment models that penalize gaps in insurance coverage and previous uninsured incidents.

Below is a table outlining how being uninsured influences your future insurance profile and costs:

| Factor | Effect on Insurance Profile | Duration/Extent |

|---|---|---|

| Uninsured Accident Record | High-risk categorisation, premium surcharges | Typically 3-5 years or longer |

| Lapses in Insurance Cover | Penalised by higher rates or limited options | Ongoing, until consistent cover |

| Asset/Salary Attachments | Increased risk profile and legal record | Can be permanent |

| Future Policy Restrictions | High excess, insurance exclusions, or required specialist policies | Several years, variable |

Long-Term Financial Consequences

The financial impact of being uninsured extends far beyond immediate accident risks. FAnews reports that insurance providers typically impose substantial premium increases for individuals with a history of uninsured driving. These increased rates can persist for multiple years, effectively transforming a temporary cost-saving decision into a long-term financial burden.

Uninsured drivers may encounter additional challenges, including:

- Significantly higher insurance premiums

- Difficulty obtaining comprehensive coverage

- Potential requirement for specialized high-risk insurance policies

- Limited options from mainstream insurance providers

Rebuilding Insurability

Recovering from a period of uninsured driving requires strategic approach and patience. Learn more about navigating insurance coverage challenges, as rebuilding your insurance profile demands consistent, responsible behavior.

To improve future insurability, individuals must demonstrate:

- Continuous insurance coverage

- Clean driving record

- Proactive risk management

- Gradual rebuilding of trust with insurance providers

The process of rehabilitating one’s insurance profile can take several years, during which individuals may face substantially higher costs and more restrictive coverage options. Insurance providers view consistent, responsible coverage as a critical indicator of future risk.

Ultimately, the decision to remain uninsured represents a complex risk calculation with potentially devastating long-term consequences. The temporary financial relief of avoiding insurance premiums pales in comparison to the sustained economic challenges created by a gap in coverage. Comprehensive, consistent insurance protection emerges as the most prudent financial strategy for protecting both immediate and future economic interests.

Frequently Asked Questions

What are the legal penalties for driving without car insurance in South Africa?

Driving without car insurance in South Africa can lead to severe legal penalties, including potential license suspension, civil lawsuits for damages, and increased future insurance premiums due to being classified as a high-risk driver.

What financial risks do uninsured drivers face in an accident?

Uninsured drivers are personally liable for all damages in an accident, including repair costs, medical expenses, and potential legal fees, which can lead to significant financial hardship or even bankruptcy.

How does not having car insurance impact future insurance rates?

Driving without car insurance can cause insurers to categorize you as a high-risk driver, resulting in substantially higher insurance premiums and increased difficulty in securing coverage in the future.

Why is comprehensive car insurance important for South African drivers?

Comprehensive car insurance is crucial for protecting against financial catastrophes resulting from accidents. It transforms potential financial burdens into manageable costs, ensuring long-term economic stability.

Protect Your Future With Reliable Car Insurance in South Africa

Reading about the real costs and personal risk of driving without car insurance in 2025 is a wake-up call for many South Africans. Whether it is the anxiety of paying out of pocket for a big accident or worrying that your entire savings could be wiped out, the article highlights exactly why these risks are simply too great to ignore. Without the right cover, one mistake on the road can become a burden that follows you for years, affecting both your finances and your peace of mind.

You do not have to face these uncertainties alone. Now is the time to shield yourself from unpredictable events and take the first step towards real financial security. Discover practical insurance solutions that are designed for South Africans just like you on the King Price Insurance website. Want to understand more about your options? Start by exploring the benefits of comprehensive car insurance or get tailored advice for your unique needs. Take control of your journey today by visiting https://insurance.kingprice.co.za and experience the peace of mind that comes with being covered.

Recommended

- Beyond Car Insurance: Extra Protection for Vehicles in 2025 – Savvy Insurance

- Top Car Insurance Tips South Africa 2025: Save and Stay Covered – Savvy Insurance

- What Is Car Insurance? A Simple Guide for 2025 – Savvy Insurance

- Understanding Insurance Coverage Limits for Cars and Homes 2025 – Savvy Insurance

- Saving Money on Car Insurance: Top Tips for 2025 – Savvy Insurance

- Insurance and Car Loans: What South Africans Need to Know in 2025 – Savvy Insurance