Vehicle insurance can feel like a maze of confusing options. Here is the surprise. Over 70 percent of South African drivers still have gaps in their cover that put their savings and even their homes at risk. Most people think a basic plan ticks the boxes, but the real risk is being underinsured when it matters most. Knowing the difference in cover types and how each one shields your assets could change how safe your future looks.

Table of Contents

- Main Types Of Vehicle Insurance Coverage

- Choosing The Right Insurance For Your Vehicle

- How Vehicle Insurance Protects Car And Home Owners

- Tips For Managing Your Vehicle Insurance Costs

Quick Summary

| Takeaway | Explanation |

|---|---|

| Understand your coverage types | Familiarize yourself with liability, comprehensive, and collision coverages to ensure adequate protection. |

| Assess personal risk factors | Evaluate your vehicle value, driving history, and assets to determine your insurance needs accurately. |

| Balance coverage and cost | Find a compromise between needed protection and affordable premiums by adjusting limits and deductibles. |

| Regularly review your insurance | Annually reassess your policy to adapt to changes in your life circumstances and ensure optimal coverage. |

| Utilize smart shopping strategies | Compare quotes and consider bundling policies for potential discounts and better rates. |

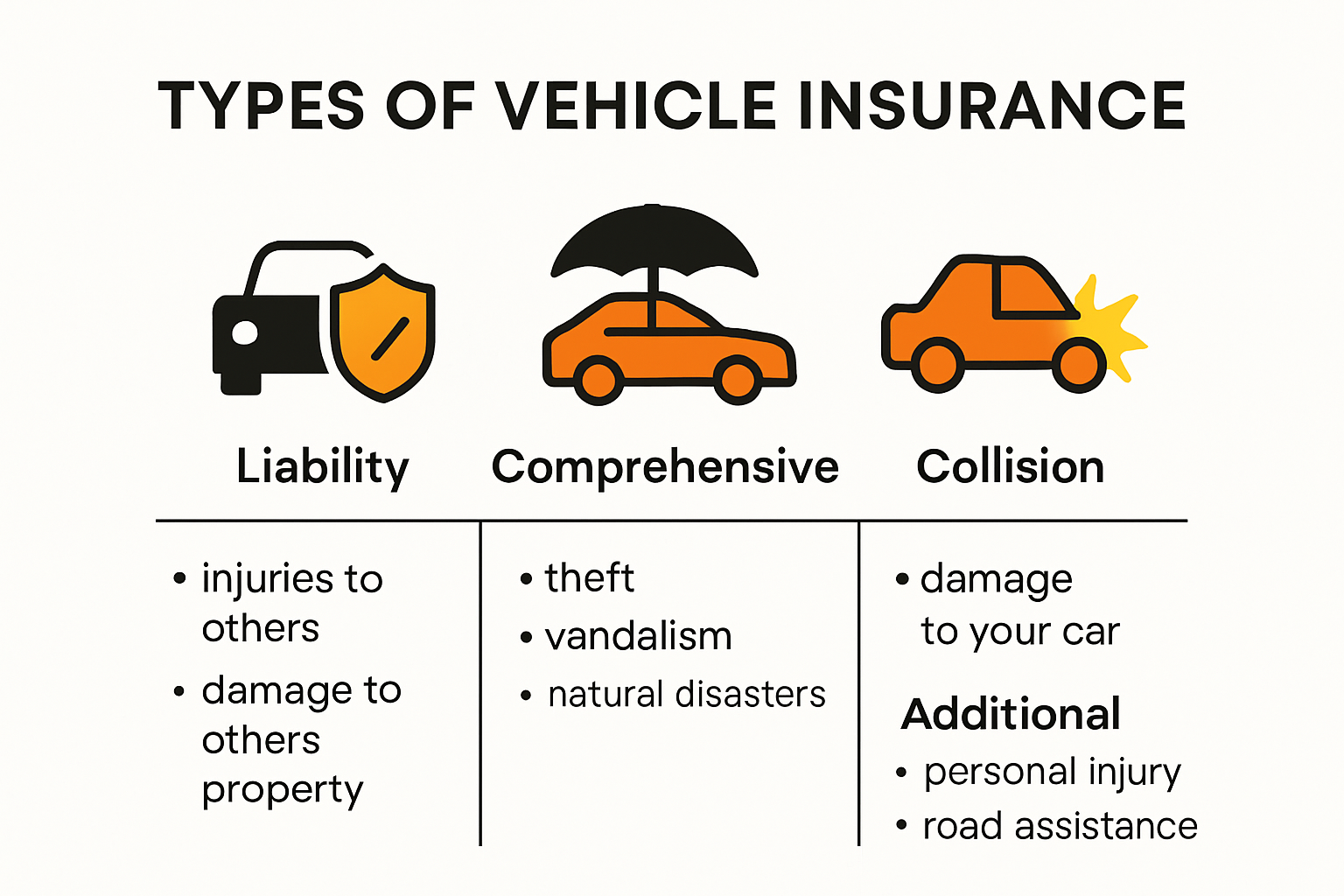

Main Types of Vehicle Insurance Coverage

Understanding the various types of vehicle insurance coverage is crucial for protecting yourself financially on the road. Vehicle insurance is not a one-size-fits-all solution, but rather a comprehensive system of protection designed to shield drivers from potential financial risks.

Liability Coverage: Your Financial Shield

Liability coverage forms the foundation of most vehicle insurance policies. According to the National Association of Insurance Commissioners, this critical coverage protects you financially if you are responsible for an accident that causes bodily injury or property damage to others. There are two primary components of liability coverage:

- Bodily Injury Liability: Covers medical expenses, rehabilitation costs, and potential legal fees if you injure another person in an accident.

- Property Damage Liability: Pays for repairs or replacement of another person’s vehicle or property damaged in an accident you caused.

It’s important to note that liability coverage does not protect your own vehicle. Experts recommend selecting coverage limits that adequately protect your personal assets in case of a significant accident.

Comprehensive and Collision Coverage: Protecting Your Vehicle

While liability coverage addresses damages to others, comprehensive and collision coverages protect your own vehicle. Research from the NAIC highlights the importance of these additional protections:

- Collision Coverage: Pays for damages to your vehicle resulting from a collision with another vehicle or object, regardless of who is at fault. This coverage is particularly valuable for newer or more expensive vehicles.

- Comprehensive Coverage: Covers damages to your vehicle from non-collision incidents such as theft, vandalism, natural disasters, falling objects, or animal-related accidents.

Additional Protection Options

Beyond the primary coverage types, drivers can consider supplementary insurance options to enhance their protection:

- Uninsured/Underinsured Motorist Coverage: Protects you if you’re involved in an accident with a driver who has insufficient or no insurance.

- Medical Payments Coverage: Helps cover medical expenses for you and your passengers, regardless of fault.

- Personal Injury Protection (PIP): Provides broader medical coverage and can include lost wages and other expenses related to an accident.

If you want to explore more about choosing the right insurance for your specific needs, read our comprehensive guide on car insurance options.

Choosing the right vehicle insurance coverage requires careful consideration of your personal circumstances, vehicle value, and potential financial risks. While the mandatory minimum might seem sufficient, investing in comprehensive coverage can provide peace of mind and substantial financial protection in unexpected situations.

Below is a summary table outlining the main types of vehicle insurance coverage mentioned above, helping you compare their core protections:

| Coverage Type | What It Covers | Who/What is Protected |

|---|---|---|

| Liability: Bodily Injury | Medical expenses, rehab, legal fees after an accident | Other people injured |

| Liability: Property Damage | Repair/replacement of someone else’s vehicle/property | Other people’s property |

| Collision | Your car after a crash with another vehicle/object | Your vehicle |

| Comprehensive | Non-collision incidents (theft, disaster, vandalism, etc.) | Your vehicle |

| Uninsured/Underinsured Motorist | Accidents caused by drivers with little/no insurance | You and your passengers |

| Medical Payments | Medical expenses (regardless of fault) | You and your passengers |

| Personal Injury Protection (PIP) | Broader medical, lost wages, accident-related expenses | You and your passengers |

Choosing the Right Insurance for Your Vehicle

Selecting the appropriate vehicle insurance requires careful consideration of multiple factors beyond simply comparing prices. Your choice of insurance should reflect your individual needs, financial situation, and risk tolerance.

Assessing Your Personal Risk Profile

Understanding your unique risk profile is the first step in choosing the right insurance. According to the Oklahoma Insurance Department, consumers should evaluate several key personal factors:

- Vehicle Value: The age, model, and current market value of your vehicle significantly impact the type and extent of coverage you need.

- Personal Assets: Consider the total value of assets you want to protect in case of a major accident, which helps determine appropriate liability coverage limits.

- Driving History: Your past driving record influences insurance rates and may suggest the need for more comprehensive protection.

Balancing Coverage and Cost

Finding the right balance between comprehensive protection and affordable premiums is crucial. The National Association of Insurance Commissioners recommends a strategic approach to selecting insurance:

- Deductible Considerations: Higher deductibles can lower monthly premiums but mean more out-of-pocket expenses during a claim.

- Coverage Limits: Opt for limits that provide adequate protection without overextending your budget.

- Additional Protections: Evaluate supplementary options like uninsured motorist coverage based on your specific risk factors.

Tailoring Insurance to Your Lifestyle

Your unique driving habits and personal circumstances should guide your insurance choices. Factors to consider include:

- Commute Distance: Longer daily drives might increase your risk of accidents, potentially requiring more comprehensive coverage.

- Vehicle Usage: Personal versus business use can impact insurance requirements.

- Living Environment: Urban areas with higher traffic and crime rates might necessitate more robust coverage.

Learn more about selecting the perfect insurance for your new vehicle to ensure you have the most suitable protection.

Remember that insurance is not a static product. Regularly review and adjust your coverage as your life circumstances change, such as purchasing a new vehicle, changing jobs, or experiencing significant life events. An annual insurance review can help ensure you always have the most appropriate and cost-effective protection for your specific needs.

How Vehicle Insurance Protects Car and Home Owners

Vehicle insurance extends far beyond simply protecting your car. It serves as a critical financial safety net that can safeguard both your vehicle and personal assets, including your home and other valuable possessions.

Financial Protection Beyond Vehicle Damage

According to the National Association of Insurance Commissioners, auto insurance provides comprehensive protection that goes well beyond basic vehicle repairs. Liability coverage, in particular, plays a crucial role in protecting homeowners from potential financial devastation.

- Asset Protection: If you are found legally responsible for an accident, your liability coverage can help protect your home and personal assets from potential lawsuits.

- Legal Defense: Insurance can cover legal expenses if you are sued as a result of an automotive incident, preventing potential personal financial ruin.

- Comprehensive Risk Management: The right insurance strategy helps mitigate risks that could otherwise threaten your financial stability.

Interconnected Property Protection

Many car owners do not realize how closely their vehicle insurance is linked to their overall financial security. Your auto insurance can provide critical protection that extends to your home and personal wealth:

- Lawsuit Prevention: Adequate liability coverage can prevent legal actions that might otherwise put your home and savings at risk.

- Uninsured Motorist Coverage: Protects you from financial losses if you are involved in an accident with an uninsured or underinsured driver.

- Medical Expense Coverage: Can help prevent medical bills from depleting your home equity or personal savings in the event of an accident.

Strategic Financial Planning

Effective vehicle insurance is a key component of broader financial planning. Explore our comprehensive guide to understanding how insurance protects your financial future.

Homeowners should view vehicle insurance as more than just a legal requirement or protection for their car. It is a strategic financial tool that provides a critical layer of protection for your entire financial ecosystem. By carefully selecting the right coverage, you create a safety net that can prevent a single automotive incident from causing catastrophic financial damage.

Remember that insurance needs evolve. Regularly reviewing your coverage ensures that your protection keeps pace with your changing life circumstances, property value, and potential risks. A comprehensive approach to vehicle insurance is not just about protecting your car it is about safeguarding your entire financial future.

The following table shows how vehicle insurance protects both your car and your broader financial assets, helping you understand the interconnected nature of these protections:

| Type of Protection | How It Works | What It Safeguards |

|---|---|---|

| Asset Protection | Shields personal assets from lawsuits after an accident | Home, savings, investments |

| Legal Defence | Covers legal fees in case you’re sued after a vehicle incident | Personal finances |

| Liability Coverage | Pays out for third-party bodily injury & property damage | Prevents loss of home & valuables |

| Medical Expense Cover | Helps pay medical bills to avoid large out-of-pocket expenses | Family, personal bank account |

| Uninsured Motorist Cover | Pays if you’re hit by a driver with no or insufficient insurance | Protects car & avoids tapping home equity |

| Comprehensive Coverage | Pays for theft & non-collision damages | Value of your own vehicle |

Tips for Managing Your Vehicle Insurance Costs

Managing vehicle insurance costs requires strategic planning and proactive approaches. While insurance is a necessary expense, there are multiple ways to optimize your coverage and reduce financial burden without compromising protection.

Smart Shopping and Comparison Strategies

According to the National Association of Insurance Commissioners, smart shopping is fundamental to managing insurance expenses. The key is to be a savvy consumer who understands the market and explores multiple options:

- Annual Policy Review: Compare quotes from different insurers every year, as rates can change significantly.

- Bundle Insurance Products: Consider combining vehicle insurance with home or other insurance for potential multi-policy discounts.

- Credit Score Management: Maintain a good credit record, as many insurers use credit information to determine premiums.

Reducing Risk and Lowering Premiums

Insurers assess risk when determining your insurance rates. By demonstrating you are a lower-risk driver, you can potentially reduce your premiums:

- Safe Driving Record: Maintain a clean driving history with no accidents or traffic violations.

- Vehicle Safety Features: Install anti-theft devices, advanced safety systems, and tracking technologies.

- Higher Deductibles: Opt for a higher deductible to lower monthly premium costs, but ensure you can afford the out-of-pocket expense if needed.

Strategic Coverage Optimization

Optimizing your coverage requires a careful balance between protection and cost. Explore our comprehensive guide to reducing car insurance expenses to understand nuanced strategies.

- Eliminate Unnecessary Coverage: For older vehicles, consider dropping comprehensive or collision coverage if the car’s value is low.

- Mileage Considerations: Some insurers offer lower rates for drivers who log fewer annual kilometers.

- Professional Memberships: Some organizations offer insurance discounts to their members.

Remember that while cost is important, the cheapest option is not always the best. Your goal should be finding comprehensive coverage that provides adequate protection at a reasonable price. Regularly reassess your insurance needs as your life circumstances change, such as purchasing a new vehicle, changing jobs, or experiencing significant life events.

By implementing these strategies, you can potentially save substantial amounts on your vehicle insurance while maintaining robust protection. The key is to be proactive, informed, and willing to explore different options that align with your specific needs and financial goals.

Frequently Asked Questions

What are the main types of vehicle insurance coverage?

The main types of vehicle insurance coverage include liability coverage, comprehensive coverage, and collision coverage. Liability coverage protects you if you’re at fault in an accident, while comprehensive coverage insures against non-collision incidents, and collision coverage pays for damages to your vehicle caused by a crash.

How can I assess my personal risk profile for vehicle insurance?

To assess your personal risk profile, consider factors like the value of your vehicle, your driving history, and the assets you want to protect. This evaluation will help you choose the right insurance coverage and limits based on your specific needs.

What additional protection options should I consider for vehicle insurance?

Additional protection options include uninsured/underinsured motorist coverage, medical payments coverage, and personal injury protection (PIP). These options can provide further financial security in case of accidents involving uninsured drivers or significant medical costs.

Why is vehicle insurance important for financial protection?

Vehicle insurance is crucial for financial protection as it safeguards not only your vehicle but also your personal assets. Adequate coverage can prevent financial ruin from lawsuits after an accident and help manage unforeseen events affecting your financial stability.

Ready to Close the Gaps in Your Car Insurance for 2025?

After reading about the different types of vehicle insurance, it is clear that many South African drivers risk financial losses by choosing cover that fails to protect both their cars and their wider financial security. If the idea of lawsuits threatening your home or underinsurance after an accident worries you, you are not alone. As the article explains, real peace of mind comes from aligning your policy with your risk profile and making sure every asset is protected, not just your vehicle.

Feel confident about the road ahead. Now is the time to review your insurance and take action for your future. For expert tips on choosing car insurance and getting tailor-made advice, head to Insurance King Price. You can also discover practical tips for cheaper car insurance in South Africa or find out more about the best insurance for new cars in 2025. Make your move today and enjoy protection that fits your life.

Recommended

- Best Insurance for New Cars in 2025: Top Picks and Tips – Savvy Insurance

- What Is Car Insurance? A Simple Guide for 2025 – Savvy Insurance

- Insurance and Buying a New Car: What South Africans Need for 2025 – Savvy Insurance

- Top Car Insurance Tips South Africa 2025: Save and Stay Covered – Savvy Insurance

5 Responses