Age is often the first thing insurers look at when you apply for car insurance. Most people know young drivers pay extra, and older drivers sometimes see their premiums climb again. But check this out. An 18-year-old in South Africa can pay up to 200 percent more than a 35-year-old for the same type of car insurance. Sounds harsh, right? The wild part is that these price swings aren’t just about age. There are hidden factors in the risk equation that can flip your expectations on their head.

Table of Contents

- The Relationship Between Age And Car Insurance Rates

- Why Age Is A Key Factor In Insurance Risk Assessment

- How Different Age Groups Are Treated By Insurers

- What Types Of Coverage Change With Age

- Real-World Examples Of Age Impact On Insurance Premiums

Quick Summary

| Takeaway | Explanation |

|---|---|

| Young drivers face the highest premiums. | Insurance costs for drivers aged 16-25 are significantly elevated due to high accident rates and limited experience. |

| Middle-aged drivers enjoy lower rates. | Those aged 26-55 generally benefit from the most favourable insurance rates due to stable and predictable driving behaviours. |

| Older drivers may see rates increase slightly. | Drivers over 55 may experience modest premium rises due to health-related concerns affecting driving capabilities, despite having more experience. |

| Insurance coverage needs change with age. | Insurance products should adapt as individuals age, reflecting changes in risk profiles, financial situations, and personal needs. |

| Statistical data underpins insurance pricing models. | Insurers rely on extensive historical data to assess risk and calculate premiums across different age demographics, informing their pricing strategies. |

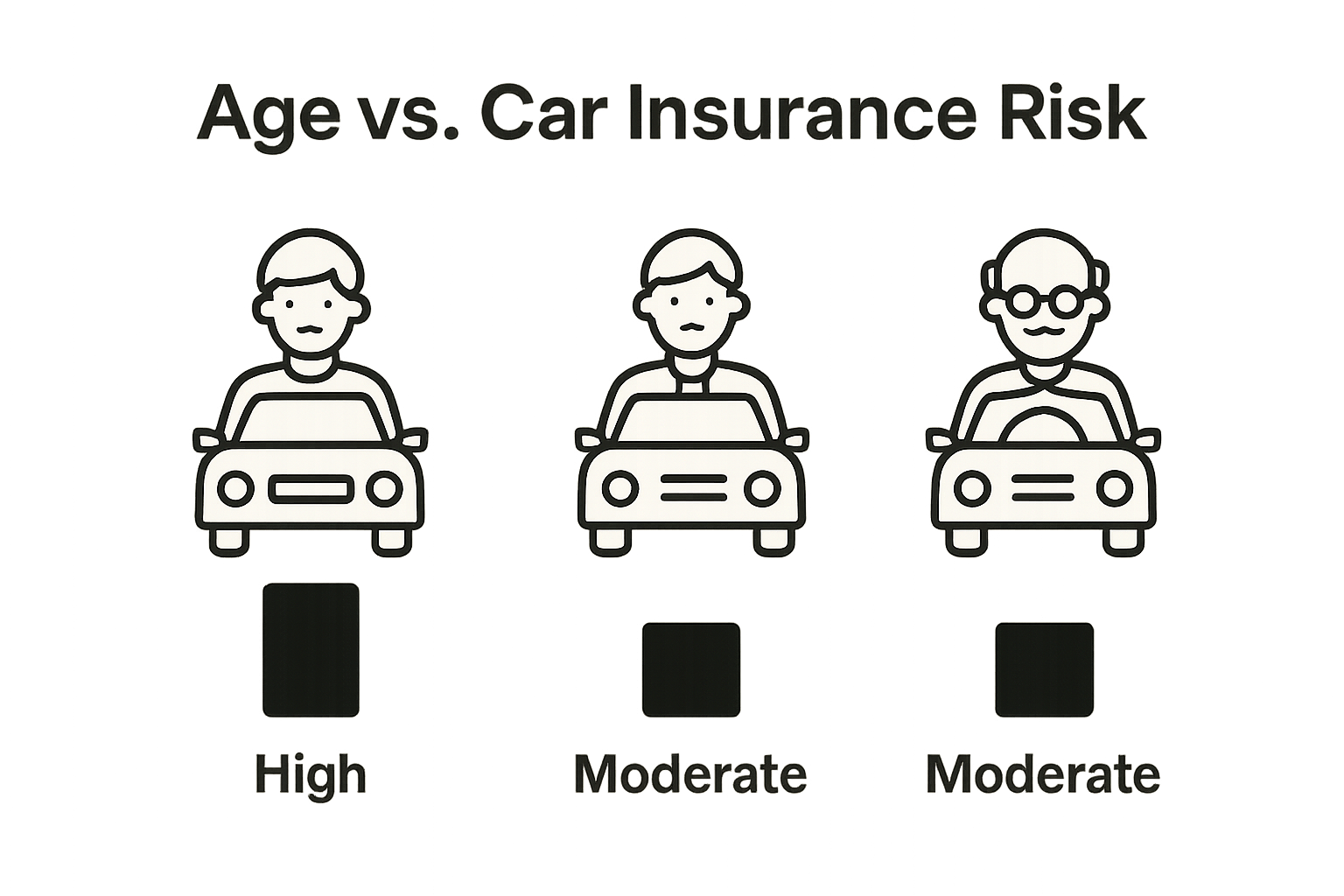

The Relationship Between Age and Car Insurance Rates

Understanding how age affects car insurance costs requires unpacking the complex risk assessment process insurers use when calculating premiums. Age is a critical factor that significantly influences insurance pricing, reflecting the statistical likelihood of accidents and claims associated with different age groups.

Risk Profiles Across Age Ranges

Insurance providers evaluate age as a key indicator of driving risk. Young drivers between 16 and 25 years typically face the highest insurance rates due to their limited driving experience and statistically higher probability of accidents. According to research published in the Potchefstroom Electronic Law Journal, young male drivers are considered particularly high-risk, with insurance calculations reflecting this elevated risk profile.

The risk assessment breakdown typically follows these patterns:

- Teenagers (16-19): Highest premium rates

- Young Adults (20-25): Gradually decreasing risk assessment

- Mid-Career Adults (26-55): Most favorable insurance rates

- Senior Drivers (55+): Slightly increased rates due to potential health and reaction time considerations

Factors Driving Age-Related Insurance Calculations

Multiple factors contribute to how insurers determine age-related pricing. Beyond accident statistics, insurers consider:

- Driving Experience: More years of driving typically correlate with safer driving behaviors

- Claims History: Younger drivers have less established driving records

- Vehicle Type: Younger drivers often choose higher-risk vehicles

- Personal Responsibility: Older drivers tend to demonstrate more cautious driving habits

For more comprehensive insights into insurance pricing strategies, check out our detailed guide on insurance cost factors.

Ultimately, age serves as a proxy for driving maturity and risk potential. While individual driving skills vary, statistical trends inform insurers’ pricing models, making age an unavoidable consideration in determining car insurance rates.

To help clarify how age groups affect car insurance in South Africa, the table below compares the key risk profiles and insurance treatment for each life stage.

| Age Group | Risk Level | Insurance Premiums | Key Characteristics |

|---|---|---|---|

| Teenagers (16-19) | Very High | Highest premiums | Little experience, highest accident rates |

| Young Adults (20-25) | High | Elevated premiums | Gradually safer, but still considered high-risk |

| Mid-Career (26-55) | Low | Most favourable rates | Stable behaviour, discounts, flexible coverage |

| Senior Drivers (55+) | Moderate/Increasing | Slight premium increases | Experienced, potential health and reaction concerns |

Why Age is a Key Factor in Insurance Risk Assessment

Insurance risk assessment involves complex mathematical models that quantify potential financial losses. Age serves as a critical predictive variable in these calculations, representing a statistical proxy for driving competence, potential accident likelihood, and overall risk exposure.

Statistical Foundations of Age-Based Risk

According to research from Stellenbosch University, age significantly influences insurance risk assessments through empirical data tracking driver behaviors and accident probabilities. Insurance actuaries develop sophisticated risk models that incorporate comprehensive datasets revealing distinct patterns across different age demographics.

Key statistical insights include:

- Accident Frequency: Younger drivers demonstrate higher incident rates

- Claim Complexity: Younger drivers tend to file more complicated and expensive claims

- Predictive Modeling: Age serves as a reliable indicator of potential future risks

Behavioral and Experiential Risk Factors

Beyond raw statistical data, insurers analyze behavioral characteristics associated with different age groups. Young drivers often exhibit higher-risk behaviors such as:

- Impulsive Decision Making: Less developed risk assessment capabilities

- Limited Driving Experience: Reduced situational awareness

- Technology Distractibility: Higher smartphone usage while driving

Older drivers, conversely, typically demonstrate more measured driving approaches, translating to lower insurance risks. Learn more about insurance pricing strategies.

Ultimately, age represents a nuanced combination of statistical probability, behavioral patterns, and potential financial liability. While individual experiences vary, insurers rely on comprehensive data models to create pricing frameworks that balance risk and fairness across different age segments.

How Different Age Groups are Treated by Insurers

Insurers employ nuanced strategies when determining insurance premiums across different age demographics, reflecting the complex relationship between age and driving risk. Each age group receives distinct treatment based on comprehensive statistical analysis and behavioral patterns.

Young Drivers: High-Risk Category

Drivers between 16 and 25 years face the most challenging insurance landscape. According to research from the South African National Treasury, insurers apply significantly higher premiums to this age group due to their elevated risk profile.

Key characteristics of young driver insurance treatment include:

- Premium Loading: Substantially higher insurance rates

- Restricted Coverage: More limited policy options

- Mandatory Additional Requirements: Often need advanced driver training certificates

Middle-Age Drivers: Preferred Risk Segment

Drivers between 26 and 55 years represent the most financially attractive segment for insurers. This age group demonstrates:

- Stable Driving Behaviors: Consistent and predictable risk patterns

- Comprehensive Coverage Options: More flexible insurance products

- Potential Discounts: Rewards for clean driving records

Explore strategies for reducing insurance costs and understanding risk assessment mechanisms.

Senior Drivers: Increased Scrutiny

Drivers over 55 experience a more complex insurance evaluation process. Insurers carefully balance age-related health considerations with driving experience. While seniors benefit from years of driving expertise, they may face slightly elevated premiums due to potential health-related driving risks.

Ultimately, age remains a critical but not exclusive factor in insurance risk assessment. Insurers continuously refine their models to create balanced, equitable pricing strategies that reflect individual driving capabilities beyond mere numerical age classifications.

What Types of Coverage Change with Age

Car insurance coverage requirements and recommendations shift significantly throughout an individual’s lifetime, reflecting changing risk profiles, financial circumstances, and personal needs. Understanding how insurance products adapt across different age stages helps consumers make informed decisions about their protection strategies.

Young Driver Coverage Characteristics

According to research from the South African Insurance Association, young drivers encounter the most restrictive and comprehensive insurance landscape. Their coverage typically includes:

- High-Risk Comprehensive Policies: More extensive protection due to elevated accident probabilities

- Mandatory Personal Liability Coverage: Significant emphasis on third-party protection

- Restricted Vehicle Options: Limited coverage for high-performance or expensive vehicles

Mid-Career Insurance Adaptations

Drivers between 26 and 55 years experience the most flexible insurance environment. This age group can typically access:

- Tailored Risk-Based Policies: More customizable coverage options

- Multi-Vehicle Discounts: Potential savings for multiple car ownership

- Enhanced No-Claims Bonuses: Rewards for consistent safe driving

Discover strategies for optimizing your insurance coverage as your life circumstances change.

Senior Driver Insurance Considerations

Older drivers face unique insurance challenges, with coverage modifications addressing age-related health and driving capability considerations. Their insurance often includes:

- Medical Emergency Additions: Enhanced personal accident and medical coverage

- Reduced Mileage Policies: Special rates for limited driving frequency

- Specialized Roadside Assistance: More comprehensive support services

Ultimately, insurance coverage is not a static product but a dynamic solution that must continuously adapt to an individual’s changing life circumstances, risk profile, and personal protection needs.

Below is a summary table outlining the typical features of car insurance coverage as you progress through different age stages in South Africa.

| Age Bracket | Coverage Focus | Typical Features |

|---|---|---|

| 16-25 (Young Driver) | High-risk comprehensive policies | Mandatory liability cover, restrictions on high-end cars |

| 26-55 (Mid-Career) | Flexible, tailored coverage | Multi-vehicle discounts, enhanced no-claims bonuses |

| 55+ (Senior) | Health and support considerations | Medical emergency, reduced mileage, roadside assistance |

Real-World Examples of Age Impact on Insurance Premiums

Insurance pricing models demonstrate dramatic variations in premium calculations based on age, reflecting complex risk assessment strategies. These real-world scenarios illustrate how insurers quantify and price risk across different life stages.

Young Driver Premium Scenarios

According to research from the Financial Intermediaries Association, young drivers experience the most significant premium disparities. Consider these practical examples:

- 18-Year-Old Driver: Potentially paying 200% more than a 35-year-old driver for identical vehicle coverage

- First-Time Insured Teenager: Initial premiums can be three to four times higher than experienced drivers

- High-Performance Vehicle for Young Driver: Often results in premium loadings exceeding 250% of standard rates

Mid-Career Premium Stability

Drivers between 26 and 55 years benefit from the most predictable and economical insurance pricing. Typical characteristics include:

- Consistent Risk Profile: Premiums stabilize and potentially decrease

- Safe Driver Discounts: Up to 40% reduction for clean driving records

- Comprehensive Coverage Options: More flexible and cost-effective policies

Explore detailed insights on insurance cost factors to understand how age influences pricing.

Senior Driver Premium Adjustments

Older drivers experience nuanced premium calculations that balance driving experience with potential health-related risks:

- 65-Year-Old Driver: May see modest premium increases of 10-20%

- Reduced Mileage Discounts: Potential savings for limited annual driving

- Advanced Safety Feature Credits: Potential premium reductions for vehicles with enhanced safety technologies

Ultimately, these examples demonstrate that age is not a static metric but a dynamic factor in calculating insurance risk, with premiums reflecting a sophisticated assessment of individual driving capabilities and potential liability.

Age Matters – So Should Your Car Insurance

If you feel frustrated about your car insurance rates climbing only because of your age, you’re not alone. Many South Africans discover that insurers often use age as a simple signal for driving risk. That means young drivers pay much more and experienced or older drivers can feel unfairly reassessed simply for another birthday. From accident statistics to changing coverage needs, these age-based calculations can leave you wondering if there’s a fairer way to protect yourself and your car.

It’s time to take control. Start by exploring practical insurance tips and tricks for South Africa and see how your unique needs and experience can work in your favour. Whether you’re a first-time driver or looking for more competitive car insurance as life moves forward, get a personalised quote that actually reflects your real life, not just your age. Visit insurance.kingprice.co.za now and discover car insurance that moves with you, every step of the way.

Frequently Asked Questions

How does age influence car insurance premiums?

Age is a significant factor in determining car insurance premiums, as insurers assess the statistical likelihood of accidents associated with different age groups. Generally, younger drivers face higher premiums due to less driving experience and higher accident rates, while mid-career adults usually enjoy lower rates.

What age group pays the highest car insurance rates?

Teenagers and young adults between the ages of 16 and 25 typically pay the highest car insurance rates due to their inexperience and higher likelihood of being involved in accidents.

Are there any discounts available for older drivers?

Yes, some insurers offer discounts for older drivers. While premiums may increase due to potential health-related risks, older drivers may also benefit from reduced mileage discounts and rewards for comprehensive safety features in their vehicles.

How can young drivers lower their insurance rates?

Young drivers can reduce their insurance costs by maintaining a clean driving record, completing advanced driver training, and opting for a vehicle that has a lower risk profile. Additionally, some insurers provide multi-vehicle discounts for families insuring multiple cars.