Every business counting on vehicles to keep operations rolling faces real risks on South African roads. Uninsured vehicle incidents can potentially bankrupt small to medium enterprises. It sounds harsh, but many assume a standard policy or taking a chance is good enough. That is where most people misjudge just how different and tailored company car insurance needs to be to keep a business safe and running.

Table of Contents

- What Is Insurance For Company Cars?

- Why Insurance For Company Cars Matters

- How Insurance For Company Cars Works

- Key Concepts In Company Car Insurance

Quick Summary

| Takeaway | Explanation |

|---|---|

| Company car insurance protects business assets | It helps safeguard against financial losses related to accidents, theft, or damage, ensuring business stability. |

| Coverage types are tailored to business needs | Options range from comprehensive to third-party policies, allowing businesses to select protections that suit their operations. |

| Understanding policy exclusions is crucial | Familiarising with exclusions prevents unexpected costs and ensures comprehensive risk management for businesses. |

| Insurance premiums are influenced by various factors | Elements like driver history and vehicle type affect premiums; managing these can optimize coverage costs. |

| Insurance supports legal compliance and employee safety | It meets regulatory requirements while protecting employees, enhancing your company’s credibility and operational efficiency. |

What is Insurance for Company Cars?

Insurance for company cars represents a specialized form of vehicle protection designed specifically for businesses that own and operate vehicles as part of their operational assets. According to the South African National Treasury, such insurance is critical for protecting business investments and managing potential financial risks associated with commercial vehicle ownership.

Understanding Company Car Insurance Fundamentals

Company car insurance goes beyond standard personal vehicle coverage, offering comprehensive protection tailored to business needs. Unlike personal auto insurance, these policies consider unique commercial risks such as multiple drivers, extensive mileage, and professional use scenarios.

Key characteristics of company car insurance include:

- Protection against damages sustained during business operations

- Coverage for multiple drivers within the organization

- Higher liability limits to address potential commercial risks

- Potential tax deductibility of insurance premiums

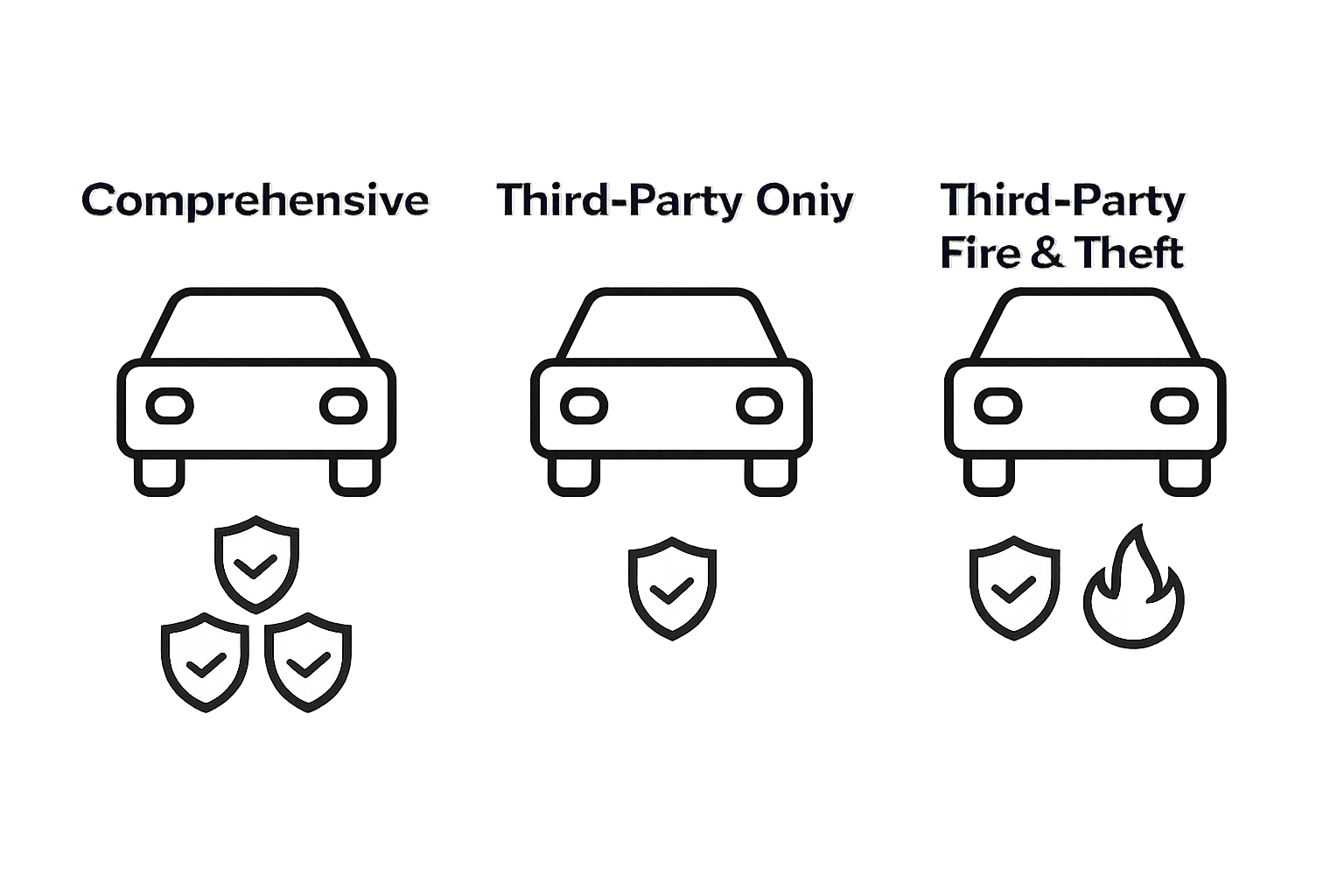

Types of Coverage for Business Vehicles

Businesses can select from various insurance approaches depending on their specific operational requirements. Read more about comprehensive car insurance options to understand the nuanced protection strategies available for company vehicles.

The primary insurance types include:

- Comprehensive Cover: Offers most extensive protection, covering theft, accidents, third-party damages, and vehicle replacement

- Third-Party Only: Provides minimal coverage focusing on damages caused to other vehicles or property

- Third-Party Fire and Theft: Intermediate coverage addressing specific risk scenarios beyond basic third-party protection

Understanding these insurance options allows businesses to make informed decisions that balance risk management with financial prudence, ensuring their mobile assets remain protected while maintaining operational efficiency.

To help clarify the choices, the following table compares the main types of insurance cover available for company vehicles in South Africa.

| Insurance Type | What It Covers | When It Suits a Business |

|---|---|---|

| Comprehensive Cover | Accidents, theft, third-party, fire, and vehicle replacement | Maximum protection for all scenarios |

| Third-Party Only | Damage to other vehicles or property | Legal minimum, low-budget cover |

| Third-Party Fire and Theft | Third-party damage, plus theft and fire | Balanced cover for specific risks |

Why Insurance for Company Cars Matters

Research from the South African insurance industry highlights that company car insurance is far more than a legal requirement—it is a critical financial protection mechanism for businesses operating in today’s complex commercial landscape.

Financial Risk Protection

Company car insurance serves as a robust financial shield against potentially devastating economic losses. When a business vehicle is involved in an accident, stolen, or damaged, the financial implications can be substantial. Uninsured vehicle incidents can potentially bankrupt small to medium enterprises, making comprehensive insurance not just advisable but essential.

Key financial risks mitigated by company car insurance include:

- Unexpected repair or replacement costs

- Legal liability for third-party damages

- Loss of business revenue during vehicle downtime

- Potential employee-related compensation claims

Legal and Operational Compliance

Beyond financial protection, company car insurance ensures businesses remain compliant with legal and operational standards. Learn more about insurance requirements for business vehicles, which can vary significantly across different industry sectors and vehicle types.

Company car insurance helps businesses:

- Meet regulatory insurance requirements

- Demonstrate responsible corporate risk management

- Protect employee welfare during business operations

- Maintain professional credibility and reputation

Strategic Business Asset Management

Insurance for company cars transforms vehicles from potential financial liabilities into strategically managed business assets. By transferring risk to insurance providers, businesses can focus on core operational objectives without constant worry about potential vehicle-related financial setbacks.

A comprehensive company car insurance strategy enables organizations to:

- Predict and control transportation-related expenses

- Provide safe and reliable transportation for employees

- Minimize unexpected financial interruptions

- Maintain business continuity in challenging scenarios

Ultimately, company car insurance represents a proactive investment in business stability, risk management, and long-term financial health.

How Insurance for Company Cars Works

Research from the South African automotive insurance sector reveals the complex mechanisms behind company car insurance, demonstrating how these specialized policies protect businesses through sophisticated risk management strategies.

Risk Assessment and Premium Calculation

Insurance providers evaluate multiple factors when determining coverage and pricing for company vehicles. The risk profile of a business directly influences insurance terms and costs. Insurers consider elements such as:

- Vehicle type and current market value

- Business industry and operational risk levels

- Driver history and employee driving records

- Geographic area of vehicle operation

- Annual mileage and vehicle usage patterns

These comprehensive assessments enable insurers to create tailored protection plans that reflect the specific risk landscape of each business.

Learn more about insurance evaluation strategies, which help businesses understand their coverage options.

Claims Processing and Support

When an incident occurs, company car insurance activates a structured claims process designed to minimize business disruption. The typical claims workflow involves:

- Immediate incident reporting to the insurance provider

- Comprehensive damage assessment

- Verification of coverage details

- Rapid repair or replacement authorization

- Potential temporary vehicle provision

Modern insurance providers increasingly offer digital platforms that streamline claims management, allowing businesses to track and manage claims efficiently.

Policy Customization and Flexible Coverage

Company car insurance is not a one-size-fits-all solution. Businesses can customize policies to address unique operational requirements. Customization options might include:

- Additional driver coverage

- Expanded geographical protection zones

- Specific equipment or cargo insurance

- Business interruption compensation

- Enhanced liability protection

By offering flexible coverage options, insurers enable businesses to create comprehensive protection strategies that align precisely with their specific risk management needs.

Key Concepts in Company Car Insurance

According to the South African Institute of Chartered Accountants, understanding the fundamental concepts of company car insurance is crucial for businesses seeking comprehensive protection and financial management.

Insurance Value and Coverage Types

Insurance value determines the financial protection level for company vehicles. Businesses must understand different valuation methods that directly impact potential compensation during claims. The primary insurance value categories include:

- Market Value: Current worth of the vehicle in the open market

- Retail Value: Dealership replacement price

- Agreed Value: Pre-negotiated fixed amount between insurer and business

Each valuation method carries distinct implications for potential payouts and premium calculations.

This table organises the different insurance value methods referenced in the guide, showing what they mean and how they can affect potential payouts or premium calculations.

| Insurance Value Type | Description | Impact on Claim Payout |

|---|---|---|

| Market Value | Current open market worth of the vehicle | Payout may be less than replacement |

| Retail Value | Price a dealership would charge for replacement | Generally higher payout than market |

| Agreed Value | Fixed amount agreed between business and insurer | Consistent payout, regardless of value |

| Learn more about insurance coverage options, which can help businesses make informed decisions. |

Policy Exclusions and Limitations

Company car insurance policies contain specific exclusions that businesses must thoroughly comprehend. Understanding these limitations prevents unexpected financial vulnerabilities. Typical policy exclusions often involve:

- Deliberate vehicle damage

- Normal wear and tear

- Mechanical failures

- Unauthorized driver incidents

- Personal use outside business parameters

Risk Management and Premium Factors

Several interconnected factors influence company car insurance premiums and risk assessments. Businesses can strategically manage these elements to optimize their insurance protection:

- Driver experience and driving record

- Vehicle safety features

- Geographic operational zones

- Annual mileage

- Industry-specific risk profiles

By comprehensively understanding these key concepts, businesses can develop robust insurance strategies that provide financial protection while managing operational risks effectively.

Protect Your Company Cars with Smart Insurance Solutions

Worried about financial setbacks, legal compliance, or gaps in your company car cover? You are not alone. Many South African businesses face the same difficulties discussed in this guide. Protecting against unexpected vehicle loss, ensuring proper liability cover, and keeping business assets safe often feels overwhelming. Understanding the difference between comprehensive cover and policy exclusions can be confusing when every business has unique needs. That is where practical and flexible protection becomes vital.

Why leave your business exposed to risk when there is a smarter way to manage your vehicles?

Move from uncertainty to peace of mind by exploring insurance that fits your company’s exact requirements. Visit insurance.kingprice.co.za to get expert tips and quick insurance quotes. Keep your operations running, your employees protected, and your finances secure. Act today to safeguard your business future. Go to insurance.kingprice.co.za to find the best plan for your company cars now.

Frequently Asked Questions

What is company car insurance?

Company car insurance is a specialized vehicle protection policy designed for businesses that own and operate vehicles. It goes beyond standard personal auto insurance by providing comprehensive coverage that addresses commercial risks such as multiple drivers and extensive vehicle use.

What types of coverage are available for company cars?

There are several types of coverage for company cars, including comprehensive cover, third-party only, and third-party fire and theft. Comprehensive cover offers extensive protection, while third-party options focus on minimal coverage requirements for legal compliance.

How is the premium for company car insurance calculated?

The premium for company car insurance is influenced by various factors, including vehicle type and market value, business industry risks, driver history, geographic area of operation, and annual mileage. Insurers assess these elements to tailor coverage plans accordingly.

What are policy exclusions in company car insurance?

Policy exclusions are specific conditions under which coverage may not apply, such as deliberate vehicle damage, normal wear and tear, mechanical failures, and incidents involving unauthorized drivers. Understanding these exclusions is vital for effective risk management.