Most people think car insurance covers everything, but that is not always true. Some South Africans are choosing to insure just the engine and leave the rest. It sounds strange, yet engine repairs can reach between R20,000 and R100,000, which is often more than what their entire car is worth. That changes how you think about insurance, does it not?

Table of Contents

- What Does Insuring Just An Engine Mean?

- Why Would Someone Want To Insure Only Their Engine?

- How Engine Insurance Works Within Vehicle Coverage

- Key Factors Influencing Engine Insurance Policies

- Real-World Applications Of Engine Insurance

Quick Summary

| Takeaway | Explanation |

|---|---|

| Engine insurance protects costly repairs | Focused coverage mitigates financial risk from engine failures, crucial for vehicle owners. |

| Ideal for older or high-mileage vehicles | This insurance is beneficial for cars with a higher likelihood of mechanical issues, such as vintage or heavily used vehicles. |

| Cost-effective alternative to full coverage | Engine-only policies can offer more affordable options for those unable to afford comprehensive insurance. |

| Focuses on specific mechanical vulnerabilities | Unlike comprehensive policies, it emphasizes protection against engine-related failures, enhancing targeted financial safety. |

| Essential for commercial vehicles | Businesses with high-use vehicles experience greater mechanical stress, making engine insurance a strategic choice for operational security. |

What Does Insuring Just an Engine Mean?

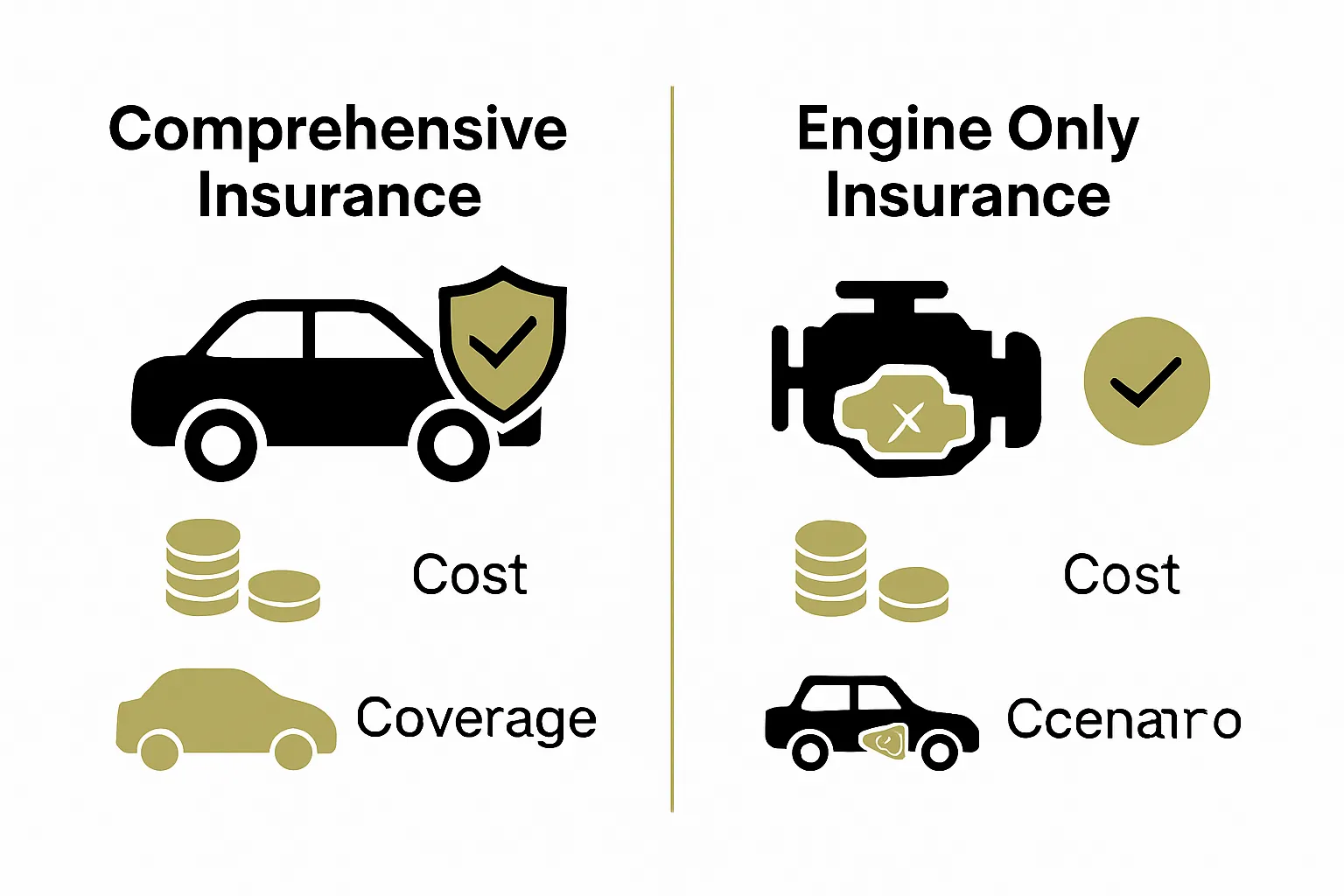

Insuring just an engine might sound peculiar, but it’s a specialized insurance option that addresses specific risks for vehicle owners. Unlike comprehensive car insurance that covers the entire vehicle, engine-only insurance focuses exclusively on protecting the most critical and expensive component of your vehicle.

The Fundamental Concept of Engine Insurance

Engine insurance is a targeted protection mechanism designed to cover repair or replacement costs specifically for your vehicle’s engine. Understanding types of vehicle insurance reveals that this niche coverage recognizes the engine as the most intricate and costly mechanical system in any vehicle.

The core purpose of this specialized insurance is to shield car owners from potentially astronomical expenses related to engine failures, which can occur due to various reasons such as:

- Manufacturing defects

- Mechanical breakdowns

- Unexpected internal component failures

- Severe wear and tear beyond normal maintenance

How Engine-Only Insurance Differs from Traditional Coverage

Traditional car insurance policies typically provide broad coverage that includes multiple vehicle components, accident damage, and third-party liabilities. Engine-only insurance, however, is a laser-focused alternative that zeroes in on the most critical mechanical component.

Below is a comparison table highlighting the key differences between traditional car insurance and engine-only insurance, making it easier to grasp how each protects your vehicle in South Africa.

| Insurance Type | Coverage Focus | Typical Cost | Key Benefit | Ideal For |

|---|---|---|---|---|

| Traditional Car Insurance | Whole vehicle (body, theft, third-party, accidents) | Higher | Broad protection against various risks | Newer vehicles, higher-value cars |

| Engine-Only Insurance | Engine (repairs/replacement) | Lower | Targeted financial safety for engine failure | Older/high-mileage, vintage, commercial cars |

This type of coverage is particularly attractive for vehicle owners who:

- Own older vehicles with higher mechanical risk

- Want more affordable insurance options

- Have limited financial resources for major repairs

- Prefer targeted protection over comprehensive packages

While not a universal solution, engine-only insurance represents an innovative approach to risk management for budget-conscious car owners who understand the potentially catastrophic financial implications of complete engine failure.

Why Would Someone Want to Insure Only Their Engine?

Insuring only an engine might seem counterintuitive, but several compelling reasons drive vehicle owners toward this specialized coverage. Understanding insurance for single car owners reveals that targeted protection can offer significant financial advantages for specific vehicle scenarios.

Cost Considerations and Financial Protection

The primary motivation behind engine-only insurance is financial risk management. Engines represent the most expensive single component in a vehicle, with replacement or major repair costs potentially ranging from R20,000 to R100,000 depending on the make and model.

Vehicle owners might choose engine-only insurance when:

- The vehicle is older and has limited comprehensive insurance options

- Comprehensive coverage is prohibitively expensive

- The car’s overall value is relatively low compared to potential engine replacement costs

- They want to mitigate specific mechanical failure risks

Strategic Insurance for High-Risk Vehicles

Some vehicles are more prone to mechanical failures due to age, usage patterns, or manufacturing history. Engine-only insurance becomes a strategic choice for owners who recognize their vehicle’s heightened mechanical vulnerability.

Key scenarios where engine-only insurance makes strategic sense include:

- Classic or vintage cars with irreplaceable engines

- High-mileage commercial vehicles

- Vehicles used in demanding work environments like construction or agriculture

- Cars with known manufacturer engine reliability issues

By focusing exclusively on engine protection, owners can create a targeted insurance strategy that addresses their most significant financial risk without the broader expenses of comprehensive coverage.

How Engine Insurance Works Within Vehicle Coverage

Engine insurance operates as a specialized subset of automotive protection, functioning differently from traditional comprehensive vehicle coverage. Beyond car insurance: extra protection highlights the nuanced approach to targeted mechanical protection.

Structural Mechanics of Engine Insurance

Engine insurance fundamentally differs from standard vehicle coverage by narrowing its protective scope exclusively to the engine system. This targeted approach means insurers assess and price policies based on specific engine-related risk factors rather than evaluating the entire vehicle.

Key structural components of engine insurance typically include:

- Precise definition of covered mechanical failures

- Specific assessment of engine condition prior to policy activation

- Clear documentation of potential repair or replacement scenarios

- Predefined limits on claim amounts and repair costs

Risk Assessment and Policy Determination

Insurers evaluate engine insurance through a complex risk assessment process that considers multiple technical and statistical factors. The evaluation process examines elements such as:

- Vehicle age and manufacturing history

- Previous maintenance records

- Engine model and manufacturer reliability statistics

- Typical usage patterns and environmental conditions

Unlike comprehensive insurance, which provides broad protection, engine insurance creates a laser-focused mechanism for addressing mechanical vulnerabilities. The policy essentially functions as a specialized warranty extension, protecting owners from potentially catastrophic financial exposure related to critical engine failures.

Key Factors Influencing Engine Insurance Policies

Engine insurance policies are far more complex than standard vehicle coverage, requiring nuanced assessment of multiple technical and financial variables. Car insurance basics for South African drivers provides fundamental context for understanding these intricate policy considerations.

Technical Evaluation Criteria

Insurers conduct exhaustive technical evaluations to determine engine insurance eligibility and premium structures. These assessments go beyond superficial examinations, diving deep into the vehicle’s mechanical integrity and potential risk profile.

Key technical factors that significantly influence policy determination include:

- Precise engine model and manufacturer reliability ratings

- Documented maintenance history

- Current mileage and overall vehicle condition

- Age of the vehicle and original manufacturing specifications

- Evidence of regular professional servicing

Financial Risk Assessment Mechanisms

The financial component of engine insurance involves sophisticated risk calculation models that transform technical data into actionable insurance strategies. Insurers meticulously analyze potential repair or replacement costs against the probability of mechanical failure.

This table outlines the main technical and financial factors insurers assess when evaluating eligibility and pricing for an engine-only insurance policy in South Africa.

| Evaluation Aspect | Technical Consideration | Financial Consideration |

|---|---|---|

| Engine Model & Reliability | Manufacturer and model risk profile | Projected repair/replacement costs |

| Maintenance History | Documented regular servicing | Past repair investments |

| Vehicle Age & Condition | Year of manufacture, current wear | Market value adjustment |

| Mileage & Usage | Total kilometres driven, use environment | Statistical failure likelihood |

| Previous Engine Problems | Record of past issues or failures | Impact on policy premium |

Critical financial considerations in engine insurance policies encompass:

- Potential repair cost projections

- Statistical likelihood of engine failure based on make and model

- Cost of comprehensive replacement versus targeted repair

- Current market value of the vehicle

- Owner’s historical maintenance investment

Unlike standard insurance products, engine insurance requires a granular approach that balances technical complexity with financial pragmatism. The goal remains creating a protection mechanism that provides meaningful coverage while maintaining economic feasibility for both the insurer and the vehicle owner.

Real-World Applications of Engine Insurance

Engine insurance transcends theoretical protection, offering tangible solutions for diverse vehicle ownership scenarios. Understanding insurance for company cars provides valuable context for how specialized coverage addresses specific automotive challenges.

Commercial and Fleet Vehicle Protection

For businesses relying on vehicles as critical operational assets, engine insurance represents a strategic financial safeguard. Commercial vehicles subjected to intense daily usage face significantly higher mechanical stress compared to personal automobiles.

Key scenarios where engine insurance becomes essential for commercial operations include:

- Long-haul transportation vehicles

- Construction and mining equipment

- Agricultural machinery

- Delivery and logistics fleet vehicles

- Vehicles operating in extreme environmental conditions

Individual Vehicle Owner Strategies

Private vehicle owners leverage engine insurance as a pragmatic risk management tool, particularly when dealing with aging or high-mileage vehicles. The coverage provides a financial buffer against potentially catastrophic mechanical failures that could render a vehicle unusable.

Typical individual scenarios benefiting from engine-specific insurance include:

- Vintage car collectors protecting irreplaceable engines

- Owners of vehicles approaching or exceeding manufacturer warranty periods

- Individuals with limited financial reserves for unexpected major repairs

- Car enthusiasts maintaining performance vehicles

- Budget-conscious drivers seeking targeted mechanical protection

Engine insurance ultimately bridges the gap between traditional comprehensive coverage and the specific mechanical vulnerabilities unique to different vehicle types and usage patterns. By offering precise, tailored protection, it enables vehicle owners to mitigate financial risks associated with critical engine failures.

Protect Your Engine and Your Wallet With Tailored Insurance

Engine failure can hit South African car owners hard. If you worry about the high costs of fixing or replacing your car’s engine, you are not alone. Many people, especially those with older vehicles or tight budgets, share this concern. General insurance often feels too broad or expensive, but the article shows how engine insurance gives you power to focus on the most expensive part of your car. Nobody wants to face a surprise garage bill or be left stranded with a dead car engine.

Why leave the heart of your car unprotected? Visit insurance.kingprice.co.za to see how you can get a solution designed for your needs. If you want advice on smarter cover for your unique situation, or want to know more about options like car warranty or comprehensive car insurance, you will find all the information and support you need. Act now, because the sooner you protect your engine, the safer your drive and your bank balance will be.

Frequently Asked Questions

Can I insure just my engine?

Yes, you can insure just your engine through a specialized insurance policy that focuses exclusively on protecting the engine against repair or replacement costs. This type of insurance is particularly useful for vehicle owners concerned about high repair expenses related to engine failures.

What are the benefits of engine-only insurance?

Engine-only insurance offers targeted financial protection against specific risks associated with engine failures. It is often more affordable than comprehensive car insurance and is ideal for owners of older vehicles or those looking to manage financial risks more effectively.

How does engine insurance differ from traditional car insurance?

Unlike traditional car insurance, which covers various aspects of the vehicle and liability, engine insurance concentrates solely on the engine. This means that it provides coverage specifically for repair or replacement of the engine rather than the entire vehicle.

Who should consider getting engine insurance?

Engine insurance is a smart choice for vehicle owners with older cars, high-mileage vehicles, classic or vintage cars, and those operating in demanding environments. It is designed for individuals who want to mitigate risks associated with engine reliability and avoid potentially high repair costs.

Recommended

- Understanding Types of Vehicle Insurance in 2025: A Guide for Car Owners – Savvy Insurance

- Understanding Insurance for Single Car Owners – Savvy Insurance

- Car Insurance and Roadworthiness: What Owners Need to Know 2025 – Savvy Insurance

- Insured Events Definition: What Car and Home Owners Need to Know – Savvy Insurance