Home insurance seems like a simple box to tick when you buy a house and most people think their policy has them covered for every disaster. But research shows nearly 70 percent of homeowners are actually underinsured without even realising it. The real risk is not in an accident or a storm but in not having a proper checklist that could be the difference between a smooth claim and a financial disaster.

Table of Contents

- What Is A Home Insurance Checklist?

- Why Having A Home Insurance Checklist Matters

- How Home Insurance Works: The Basics

- Key Concepts In Home Insurance Policies

- Real-World Applications Of Home Insurance Checklists

Quick Summary

| Takeaway | Explanation |

|---|---|

| Use a checklist for insurance assessment | A home insurance checklist helps identify coverage gaps and document essential property details for protection strategies. |

| Regularly update your insurance documents | Keeping your checklist current ensures that your coverage reflects any changes in property value or risks, preventing underinsurance. |

| Document valuable possessions comprehensively | Thorough inventory documentation simplifies the claims process and protects against financial loss during emergencies. |

| Understand your policy’s key terms | Familiarity with definitions like insured value and deductible enables informed decision-making about coverage needs and risks. |

| Utilise the checklist for proactive risk management | Regularly reviewing security features and potential hazards helps mitigate vulnerabilities and enhances financial security. |

What is a Home Insurance Checklist?

A home insurance checklist is a comprehensive document that helps homeowners systematically review and manage their property protection strategy. This strategic tool goes beyond a simple list, serving as a critical framework for understanding, evaluating, and maintaining adequate insurance coverage for your most valuable asset.

Understanding the Purpose of a Home Insurance Checklist

A home insurance checklist acts as a strategic roadmap that allows homeowners to thoroughly assess their property’s unique risk profile. By methodically documenting and reviewing key aspects of home protection, individuals can ensure they have comprehensive coverage that matches their specific needs.

Key objectives of a home insurance checklist include:

- Identifying potential coverage gaps

- Documenting valuable household possessions

- Assessing property-specific risks

- Tracking insurance policy details

- Ensuring regular policy updates

According to Insurance Expert Network, a well-prepared home insurance checklist can help homeowners reduce potential financial vulnerabilities by proactively managing their insurance strategy.

Key Components of an Effective Home Insurance Checklist

An effective home insurance checklist typically encompasses several critical areas of evaluation. Read our comprehensive guide on avoiding underinsurance to understand how a detailed checklist can protect your financial interests.

The checklist should include comprehensive documentation about:

- Property structural details

- Current market value of the home

- Detailed inventory of personal belongings

- Specific risks in your geographical area

- Current insurance policy specifications

By systematically addressing these elements, homeowners can create a robust protection strategy that adapts to changing circumstances and minimizes potential financial risks. The checklist is not a static document but a dynamic tool that requires regular review and updating to remain effective.

Why Having a Home Insurance Checklist Matters

A home insurance checklist is not merely a bureaucratic exercise but a critical financial protection strategy that can save homeowners significant stress and potential economic loss. Understanding why this document matters requires exploring its profound impact on property management and risk mitigation.

Financial Protection and Risk Management

Home insurance checklists serve as a proactive defense mechanism against unforeseen financial vulnerabilities. By comprehensively documenting property details and potential risks, homeowners create a robust shield against potential economic disruptions.

Key financial protection benefits include:

- Preventing underinsurance scenarios

- Establishing clear documentation for potential claims

- Identifying potential coverage gaps before they become critical

- Creating a systematic approach to asset valuation

- Simplifying insurance claim processes during stressful events

According to the Maine Bureau of Insurance, maintainin

g a detailed home inventory can significantly expedite insurance claims and ensure accurate compensation.

Comprehensive Property Awareness

Learn how to evaluate your unique insurance needs to understand the intricate relationship between documentation and protection. A home insurance checklist transforms abstract risk into tangible, manageable information.

Homeowners gain critical insights by systematically documenting:

- Property structural changes

- Value of personal possessions

- Potential geographical risk factors

- Home improvement investments

- Security system details

This comprehensive approach allows for more accurate insurance coverage, ensuring that homeowners are neither over-insured nor dangerously under-protected. The checklist becomes a living document that evolves with the property, reflecting its changing value and potential risks.

How Home Insurance Works: The Basics

Home insurance is a complex financial protection mechanism designed to shield homeowners from potential economic losses related to property damage, theft, and liability. Understanding its fundamental principles helps individuals make informed decisions about their coverage and risk management strategy.

Core Components of Home Insurance

Home insurance operates through a structured framework of coverage types that address different potential risks and scenarios. The policy essentially creates a financial safety net that protects homeowners from unexpected and potentially devastating economic challenges.

The following feature table compares the core components of home insurance policies, helping homeowners visualise different coverage areas and their purposes.

| Coverage Area | Description |

|---|---|

| Dwelling protection | Covers structural damage to the home |

| Personal property coverage | Protects belongings inside the home |

| Liability protection | Shields against legal claims from property-related incidents |

| Additional living expenses | Supports temporary housing if your home becomes uninhabitable |

| Detached structures coverage | Includes protection for garages, sheds, and other external buildings |

Typical home insurance policies encompass several critical coverage areas:

- Dwelling protection: Covers structural damage to the home

- Personal property coverage: Protects belongings inside the home

- Liability protection: Shields against legal claims from property-related incidents

- Additional living expenses: Supports temporary housing if home becomes uninhabitable

- Detached structures coverage: Includes protection for garages, sheds, and other external buildings

Learn about insured events and their implications to understand the nuanced landscape of home insurance protection.

Risk Assessment and Premium Calculation

Insurance providers evaluate multiple factors when determining home insurance premiums. This complex calculation considers the property’s inherent risks, location-specific challenges, and the homeowner’s individual risk profile.

Key elements influencing insurance pricing include:

- Home’s geographical location and potential natural disaster risks

- Property’s age and construction materials

- Security systems and risk mitigation features

- Homeowner’s claims history

- Credit score and financial stability

The goal of this detailed assessment is to create a fair and accurate pricing model that reflects the specific risk characteristics of each individual property. Homeowners can often reduce their premiums by implementing additional safety measures and maintaining a comprehensive risk management approach.

Key Concepts in Home Insurance Policies

Home insurance policies are intricate legal contracts that protect homeowners from financial risks. Understanding the fundamental concepts behind these agreements is crucial for making informed decisions about property protection and risk management.

Policy Definitions and Core Terminology

Every home insurance policy contains specific terminology that defines the scope, limitations, and conditions of coverage. Familiarizing yourself with these key terms helps homeowners navigate their insurance landscape more effectively.

Critical policy terms include:

Below is a definition table that organises key home insurance policy terms and their explanations for quick reference.

| Term | Definition |

|---|---|

| Insured value | The maximum amount an insurance company will pay for a claim |

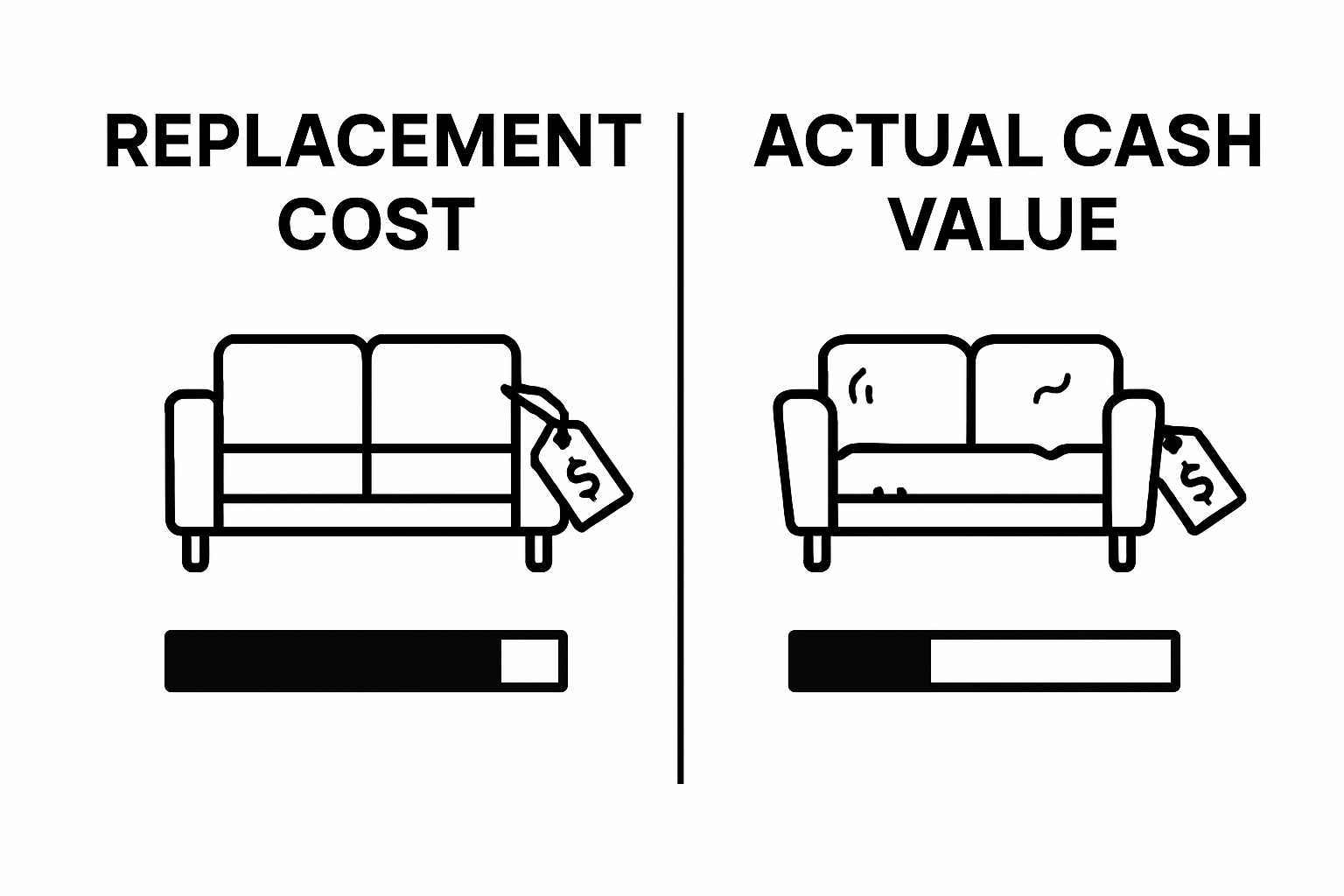

| Replacement cost | The expense of replacing damaged property with similar quality items |

| Actual cash value | The current market value of items, accounting for depreciation |

| Deductible | The amount homeowners pay out of pocket before insurance coverage begins |

| Peril | Specific risks or events covered under the insurance policy |

- Insured value: The maximum amount an insurance company will pay for a claim

- Replacement cost: The expense of replacing damaged property with similar quality items

- Actual cash value: The current market value of items, accounting for depreciation

- Deductible: The amount homeowners pay out of pocket before insurance coverage begins

- Peril: Specific risks or events covered under the insurance policy

Discover the details about insurance coverage limits to understand how these definitions impact your overall protection strategy.

Types of Coverage and Exclusions

Home insurance policies are not uniform and vary significantly in their coverage approaches. Homeowners must carefully understand what is included and excluded in their specific policy to avoid unexpected financial vulnerabilities.

Typical coverage categories encompass:

- Structural damage protection

- Personal property replacement

- Liability protection for third-party injuries

- Additional living expenses during home repairs

- Medical payments for guests injured on the property

Understanding these nuanced coverage types ensures homeowners can select policies that comprehensively address their unique risk profiles. The goal is to create a robust financial safety net that provides peace of mind and comprehensive protection against potential economic disruptions.

Real-World Applications of Home Insurance Checklists

Home insurance checklists transcend theoretical documentation, serving as practical tools that provide tangible benefits during critical moments of property management and unexpected incidents. These comprehensive documents become lifelines when homeowners face complex insurance scenarios.

Streamlining Insurance Claims Process

A meticulously maintained home insurance checklist dramatically simplifies the claims process by providing immediate, organized documentation of property assets and damage. When unexpected events occur, homeowners can rapidly provide insurers with precise, comprehensive information, reducing stress and accelerating compensation.

Key advantages during claims include:

- Faster claims processing

- Accurate documentation of property value

- Comprehensive evidence for insurance assessments

- Reduced likelihood of claim disputes

- Clear record of property improvements and modifications

Learn about essential insurance inspection requirements to understand how detailed documentation supports successful insurance interactions.

Proactive Risk Management

Home insurance checklists function as dynamic risk management tools that enable homeowners to anticipate and mitigate potential vulnerabilities. By systematically tracking property details, security features, and potential hazards, individuals can make informed decisions about risk reduction and insurance coverage.

Practical risk management strategies encompass:

- Regular property condition assessments

- Documenting security system installations

- Tracking home improvement investments

- Updating inventory of valuable possessions

- Identifying potential geographical risk factors

The checklist becomes a living document that evolves with the property, providing a comprehensive snapshot of the home’s changing risk profile and protection needs. Homeowners who consistently maintain and update their checklists create a robust framework for financial security and peace of mind.

Make Your Home Insurance Checklist Work For You in South Africa

It is easy to feel uncertain about your home insurance. Worrying about coverage gaps and knowing whether your most valuable possessions are actually protected can leave any South African homeowner uneasy. The insights from your home insurance checklist reveal just how important accurate documentation and policy understanding are. Creating your own checklist is the first step. Making sure you have the right partner for your insurance journey is just as vital. Our team understands the details of structural protection, home contents cover, and even the nuances of geographical risks mentioned in your checklist.

Take control of your peace of mind today. Visit insurance.kingprice.co.za to explore how our tailored solutions can fill those critical insurance gaps and give you complete clarity about your cover. Do not wait for a loss to expose where your protection ends. Get a proper safety net in place right now. Let your completed checklist become the start of your smarter home insurance plan with us.

Frequently Asked Questions

What is the purpose of a home insurance checklist?

A home insurance checklist helps homeowners systematically review and manage their property protection strategy, ensuring they have comprehensive coverage tailored to their unique needs and risks.

What key components should be included in an effective home insurance checklist?

An effective home insurance checklist should include details about the property structure, current market value, inventory of personal belongings, geographical risks, and specifics of the current insurance policy.

How does a home insurance checklist aid in the claims process?

A well-maintained home insurance checklist streamlines the claims process by providing organized and immediate documentation of property assets and damages, leading to faster claims processing and reduced likelihood of disputes.

Why is it essential to regularly update a home insurance checklist?

Regular updates to a home insurance checklist ensure it reflects any changes in property value, improved security measures, or newly acquired belongings, helping homeowners maintain adequate and relevant coverage over time.