Property insurance covers everything from your home and its contents to business buildings and inventory. In South Africa, buildings insurance covers damage from fires, floods, and storms, while home contents insurance protects everything inside, from TVs to couches. Most people think it only matters when disaster strikes. Fact is, property insurance can be the reason your family keeps a roof over their heads or your business keeps its doors open the day after disaster hits.

Table of Contents

- What Are The Types Of Property Insurance?

- Why Property Insurance Matters For Homeowners And Car Owners

- How Different Types Of Property Insurance Work

- Key Concepts And Features Of Property Insurance

- Real-World Examples Of Property Insurance Applications

Quick Summary

| Takeaway | Explanation |

|---|---|

| Understand different insurance types | Familiarize yourself with residential and commercial insurance types for comprehensive coverage. |

| Financial security from risks | Property insurance protects against unforeseen damages, financially stabilizing owners during crises. |

| Know your policy exclusions | Be aware of what is not covered in your insurance to avoid surprises at claim time. |

| Importance of accurate documentation | Maintain comprehensive records to expedite claims processing and ensure proper risk assessment. |

| Insurance boosts economic resilience | Effective property insurance supports quicker recovery and long-term financial stability for owners. |

What Are the Types of Property Insurance?

Property insurance represents a critical financial protection mechanism for South African property owners, offering comprehensive coverage against potential risks and unexpected damages. Understanding the various types of property insurance helps individuals make informed decisions about safeguarding their valuable assets.

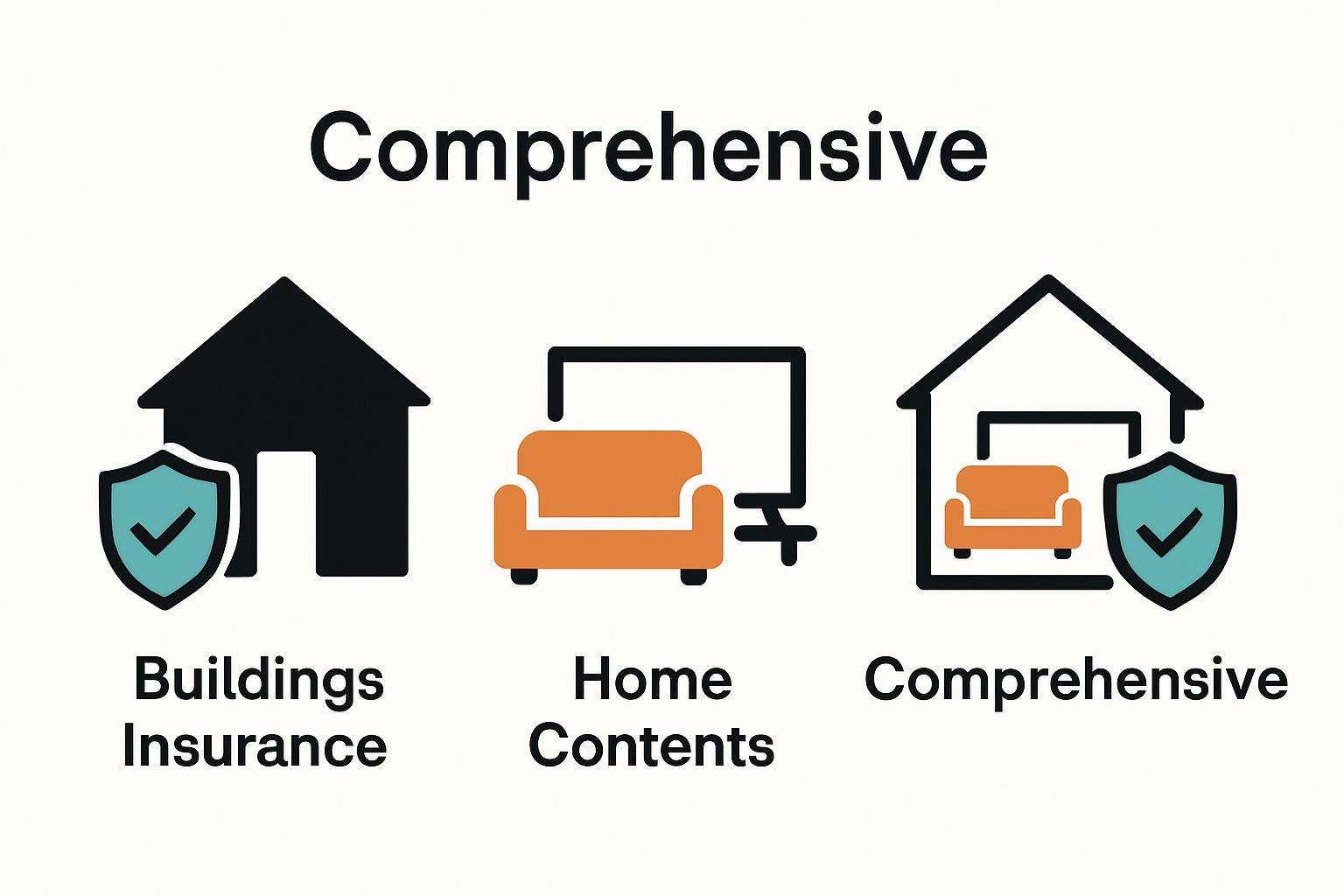

Residential Property Insurance Categories

Residential property insurance encompasses multiple coverage options designed to protect homeowners from financial losses. These insurance types address different aspects of property protection, ensuring comprehensive risk management.

Key residential property insurance categories include:

- Buildings Insurance: Covers the physical structure of the home, protecting against damage from events like fires, floods, storms, and structural collapse.

- Home Contents Insurance: Protects personal belongings inside the home, including furniture, electronics, clothing, and other valuable items.

- Comprehensive Home Insurance: Combines buildings and contents insurance, providing a more holistic protection approach for homeowners.

Commercial Property Insurance Overview

For businesses and commercial property owners, insurance needs become more complex and specialized. Our guide on insurance add-ons provides additional insights into comprehensive coverage options.

Commercial property insurance typically includes:

- Property Damage Coverage: Protects physical assets against damage from natural disasters, accidents, and other unforeseen events.

- Business Interruption Insurance: Provides financial support if business operations are temporarily halted due to property damage.

- Liability Protection: Covers legal expenses and potential compensation claims related to property-related incidents.

According to South African Insurance Association, property insurance is not just a financial product but a critical risk management tool that helps property owners mitigate potential economic losses. The right insurance strategy can provide peace of mind and financial stability in an unpredictable environment.

Why Property Insurance Matters for Homeowners and Car Owners

Property insurance serves as a crucial financial safety net, protecting individuals from potentially devastating economic losses arising from unexpected events. For South African homeowners and car owners, understanding the importance of comprehensive insurance coverage can mean the difference between financial stability and potential economic ruin.

Financial Protection Against Unforeseen Risks

Property owners face numerous risks that could result in substantial financial strain. Our guide to vehicle insurance highlights the critical nature of comprehensive protection strategies.

Key financial risks include:

- Property Damage: Natural disasters, accidents, and vandalism can cause significant structural or asset damage.

- Liability Claims: Legal expenses from property-related incidents can quickly escalate.

- Replacement Costs: Without insurance, replacing damaged property or vehicles becomes an immense personal financial burden.

Risk Mitigation and Economic Resilience

Insurance goes beyond mere financial compensation. According to Old Mutual’s Risk Management Report, property insurance provides critical economic resilience for South African families and businesses.

Risk mitigation strategies through property insurance offer:

- Immediate Financial Support: Rapid claims processing helps property owners recover quickly.

- Psychological Peace of Mind: Knowing potential losses are covered reduces stress and uncertainty.

- Long-term Financial Planning: Insurance enables more predictable personal and business financial management.

Legal and Practical Considerations

Many financial institutions and rental agreements require property insurance as a mandatory protection mechanism. Some mortgage providers will not approve financing without adequate insurance coverage, underscoring its critical importance in South African property ownership landscapes.

Property insurance represents more than a financial product. It is a strategic tool for managing risk, protecting assets, and ensuring economic stability in an increasingly unpredictable world.

How Different Types of Property Insurance Work

Property insurance operates through complex mechanisms designed to provide financial protection and risk management for property owners. Understanding how these insurance types function can help individuals make informed decisions about their coverage needs.

Claims Processing and Risk Assessment

The fundamental operation of property insurance revolves around comprehensive risk evaluation and strategic claims management. Our guide to rental property insurance provides additional context on specific insurance scenarios.

Key elements of insurance operational frameworks include:

- Risk Profiling: Insurers conduct detailed assessments of property characteristics, location, and potential vulnerability.

- Premium Calculation: Insurance costs are determined based on comprehensive risk evaluations and potential replacement values.

- Claim Verification: Detailed investigation processes ensure legitimate and accurate compensation for property damages.

Coverage Mechanisms and Compensation Strategies

According to the Ombudsman for Short-Term Insurance, property insurance compensation strategies are designed to restore property owners to their financial position before an incident occurred.

Compensation approaches typically involve:

- Replacement Cost Coverage: Provides funds to replace damaged items at current market prices.

- Actual Cash Value Coverage: Compensates for property value after depreciation is considered.

- Agreed Value Coverage: Establishes a predetermined compensation amount for specific high-value assets.

Documentation and Compliance Requirements

Successful property insurance relies on meticulous documentation and adherence to specific legal and procedural standards. Property owners must maintain comprehensive records, including property valuations, maintenance histories, and detailed inventories of insured assets.

Insurers require precise documentation to:

- Validate claims efficiently

- Prevent fraudulent submissions

- Ensure accurate risk assessment

Effective property insurance is not merely a financial product but a sophisticated risk management system that protects individuals and businesses from potential economic disruptions.

Key Concepts and Features of Property Insurance

Property insurance encompasses a complex network of protective mechanisms designed to shield property owners from financial vulnerabilities. Understanding the fundamental concepts and features helps individuals make informed decisions about their insurance strategies.

Core Insurance Terminology and Definitions

Our comprehensive coverage guide provides deeper insights into insurance terminology. Property insurance involves several critical technical concepts that property owners must comprehend:

Key insurance terminology includes:

Here is a table outlining key insurance terminology relevant to South African property insurance, alongside concise definitions to clarify each concept for readers.

| Term | Definition |

|---|---|

| Premium | The regular payment made to maintain insurance coverage |

| Deductible | The out-of-pocket amount the insured pays before an insurance claim is settled |

| Insured Value | The maximum amount the insurer will pay for a specific claim |

| Risk Assessment | Evaluation of property risks and factors to determine coverage and premiums |

| Exclusion | Specific situations or damages not covered by an insurance policy |

| Actual Cash Value | The value of the property after accounting for depreciation |

| Replacement Cost | Amount needed to replace damaged items at today’s prices |

- Premium: The regular payment made to maintain insurance coverage.

- Deductible: The amount an insured person pays out-of-pocket before insurance compensation begins.

- Insured Value: The maximum amount an insurance policy will pay for a specific claim.

Risk Assessment and Coverage Parameters

According to the South African Insurance Association, effective property insurance relies on sophisticated risk evaluation mechanisms. Insurers analyze multiple factors to determine appropriate coverage and pricing.

Risk assessment parameters typically involve:

- Property Location: Geographic risks like flood zones, crime rates, and natural disaster potential.

- Property Condition: Age, maintenance history, and structural integrity of the property.

- Replacement Cost: Current market value and potential reconstruction expenses.

Policy Exclusions and Limitations

Property insurance policies are not universal catch-all protections. Each policy contains specific exclusions and limitations that property owners must carefully understand. These restrictions define scenarios where insurance compensation will not apply.

Common policy exclusions often include:

- Deliberate damage or negligence

- Normal wear and tear

- Specific high-risk events not explicitly covered

Comprehensive property insurance represents a nuanced financial instrument that balances risk management, financial protection, and individual property characteristics. Successful insurance strategies require thorough understanding and proactive engagement with policy details.

Real-World Examples of Property Insurance Applications

Property insurance transforms theoretical protection into practical financial solutions for individuals and businesses facing unexpected challenges. Real-world scenarios demonstrate the critical role insurance plays in mitigating economic risks and providing financial stability.

Residential Property Scenarios

Our comprehensive guide to fire damage claims illustrates the complex nature of property insurance applications. Residential property insurance becomes particularly crucial in scenarios involving significant property damage.

Typical residential insurance scenarios include:

- Electrical Fire Recovery: A short circuit causes extensive damage to a home’s electrical system and surrounding structures, requiring comprehensive repair and replacement.

- Burst Pipe Damage: Water damage from a burst pipe destroys flooring, furniture, and electrical equipment, necessitating full property restoration.

- Storm Damage Restoration: Severe weather conditions result in roof damage, broken windows, and structural compromises requiring immediate intervention.

Commercial Property Protection

According to the South African Insurance Association, commercial property insurance plays a pivotal role in business continuity and economic resilience.

Commercial insurance application examples involve:

- Business Interruption Coverage: A manufacturing facility experiences equipment breakdown, with insurance covering lost income during repair periods.

- Inventory Protection: A retail store suffers significant stock loss due to unexpected flooding, with insurance compensating for the complete inventory replacement.

- Liability Coverage: A small business faces potential legal claims after an accident on its premises, with insurance providing financial protection against potential litigation.

Specialized Insurance Applications

Beyond standard coverage, property insurance adapts to unique and complex scenarios that require specialized protection strategies. These nuanced applications demonstrate the flexibility of modern insurance frameworks.

Specialized insurance scenarios include:

- High-value asset protection for unique properties

- Risk mitigation for properties in environmentally vulnerable locations

- Customized coverage for historical or architecturally significant structures

Property insurance represents more than a financial product. It is a sophisticated risk management tool that provides peace of mind and economic security in an unpredictable world.

Secure Your South African Property With Expert Insurance Solutions

The article highlights how unpredictable events like fires, floods, and theft can leave South Africans facing major financial strain. You have learned about terms like buildings insurance, home contents insurance, and the risks of being unprepared. Feeling anxious about replacing valuable assets or covering sudden repair costs is all too common. It is time to stop worrying and take control.

Protect your property and peace of mind with affordable, tailor-made protection from King Price Insurance. Our solutions cover everything you learned about, including home and car insurance, so you can safeguard your future. Ready to make sure you are covered before the next disaster strikes? Visit King Price Insurance now and get your quote in just a few clicks. Don’t wait until it’s too late. Take action now to keep your assets safe.

Frequently Asked Questions

What are the main types of property insurance available for homeowners?

The main types of property insurance for homeowners include Buildings Insurance, which covers the physical structure of the home; Home Contents Insurance, which protects personal belongings inside the home; and Comprehensive Home Insurance, which combines both buildings and contents coverage for complete protection.

Below is a comparison table outlining the main types of property insurance available in South Africa, highlighting who they are designed for, what they cover, and key coverage features.

| Insurance Type | Designed For | What It Covers | Key Features |

|---|---|---|---|

| Buildings Insurance | Homeowners | Physical structure of home | Structural damage from fire, flood, storms |

| Home Contents Insurance | Homeowners/Tenants | Personal belongings inside the home | Furniture, electronics, jewellery, appliances |

| Comprehensive Home | Homeowners | Both structure and contents | Combines building and contents cover |

| Commercial Property | Business Owners | Physical business assets | Damage from disasters, accidents or theft |

| Business Interruption | Business Owners | Loss of income from halted operations | Financial support during business downtime |

| Liability Protection | Property/Business Owners | Legal expenses, compensation claims | Protection against third-party liabilities |

How does commercial property insurance differ from residential property insurance?

Commercial property insurance is tailored for businesses and typically includes Property Damage Coverage to protect physical assets, Business Interruption Insurance to support financially during operational halts due to property damage, and Liability Protection for legal expenses relating to property-related incidents. In contrast, residential insurance focuses on protecting individual homes and personal belongings.

What factors influence the cost of property insurance premiums?

The cost of property insurance premiums is influenced by several factors, including the property’s location, its condition and age, the insured value, and the type of coverage selected. Insurers conduct detailed risk assessments to determine premium amounts.

Why is liability protection important in property insurance policies?

Liability protection in property insurance is crucial because it covers legal expenses and potential compensation claims that may arise from incidents related to the property. This protection helps safeguard property owners from the significant financial burden of liability claims.