Insurance premiums touch nearly every South African who wants protection from life’s curveballs. Most people just accept the amount listed on their bill and move on. But did you know that policy benefits in South Africa usually increase every year in line with the inflation rate, meaning your premium may quietly jump while offering the same cover? The real surprise is that these increases have little to do with your own actions and everything to do with a web of industry trends you might never notice.

Table of Contents

- What Are Insurance Premiums And How Are They Determined?

- Reasons Why Insurance Premiums May Increase Annually

- Factors Influencing Annual Premium Changes

- The Impact Of Claims History On Premium Rates

- Understanding Market Trends And Their Effect On Premiums

Quick Summary

| Takeaway | Explanation |

|---|---|

| Insurance premiums reflect personal risk and coverage level | Your premium amount is influenced by your individual characteristics and the type of protection you choose. |

| Annual premium increases depend on multiple factors | Changes in your life or economic conditions can cause your premium to rise each year. |

| Claims history influences future premium rates | A history of frequent or substantial claims can classify you as high-risk, leading to higher premiums. |

| Technological advancements shape pricing strategies | Modern tools like AI and data analytics allow insurers to assess risks more accurately, affecting how premiums are calculated. |

| Market trends affect premium calculations | Economic and regulatory changes, along with industry-specific risks, constantly alter how insurers set their prices. |

What Are Insurance Premiums and How Are They Determined?

An insurance premium represents the monetary amount you pay an insurance company in exchange for maintaining an active insurance policy. These financial contributions are essentially your ticket to risk protection and financial security against potential future losses.

Understanding the Basic Structure of Insurance Premiums

Insurance premiums are calculated using complex mathematical models that assess multiple risk factors unique to each policyholder. Insurers analyze several key elements to determine the precise amount you will pay:

- Personal Risk Profile: Your individual characteristics such as age, health status, driving record, or property location

- Coverage Level: The extent and comprehensiveness of protection you select

- Historical Claims Data: Statistical information about potential risks in your specific category

According to research from the South African National Treasury, policy benefits typically escalate annually based on the Consumer Price Index (CPI) inflation rate. This means your insurance premium might adjust yearly to maintain equivalent financial protection.

Factors Influencing Premium Calculations

Insurance companies employ sophisticated risk assessment techniques to calculate premiums. These calculations consider multiple variables that help predict potential future claims:

- Probability of an event occurring

- Potential financial impact of that event

- Administrative and operational costs of the insurance provider

For instance, a car insurance premium for a young driver with multiple traffic violations will likely be higher than for an experienced driver with a clean record. Similarly, a home located in an area with high crime rates might attract a different premium compared to a property in a statistically safer neighborhood.

If you want to read more about how car premiums are specifically calculated, our comprehensive guide provides deeper insights into the intricate processes insurers use to determine your specific rate.

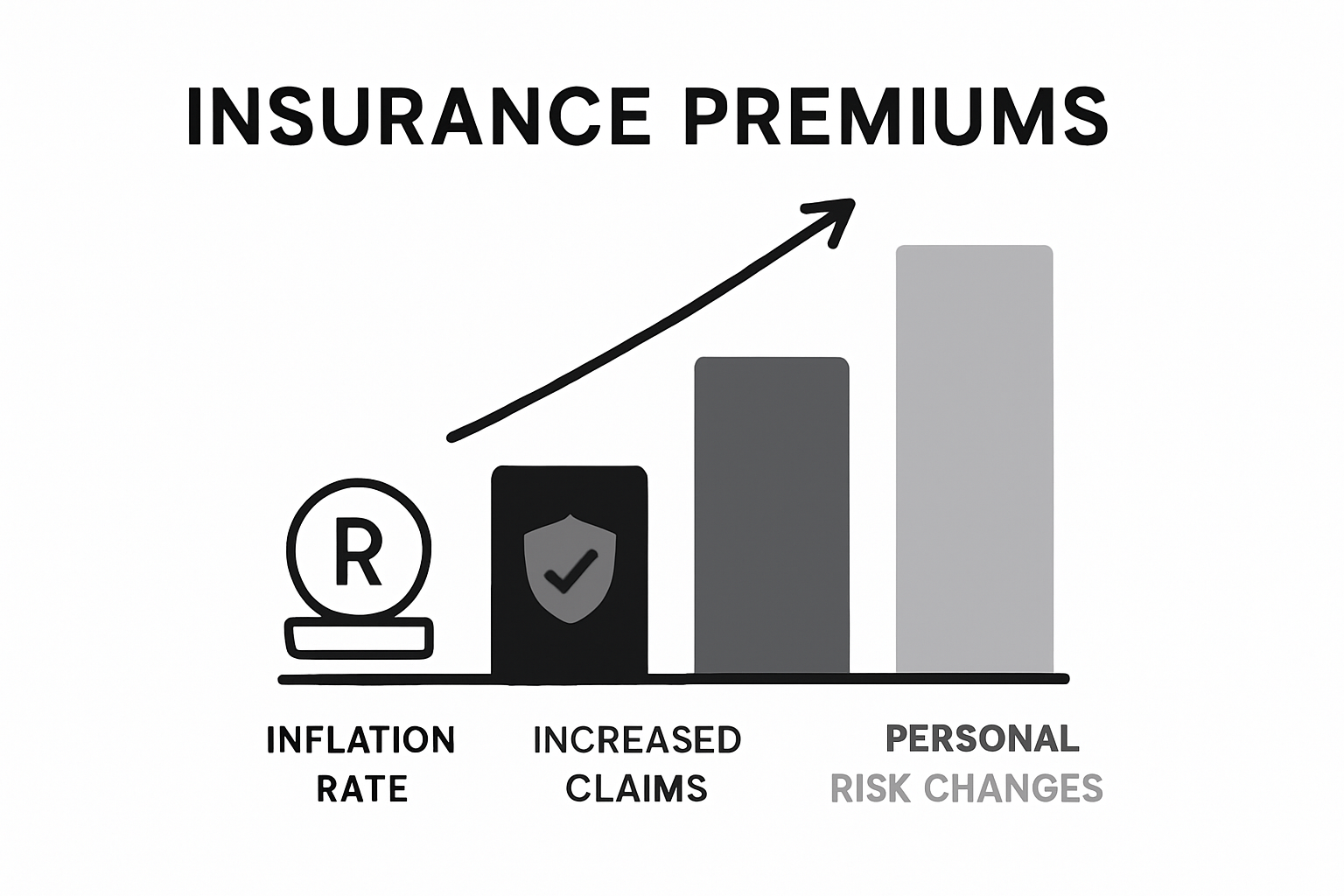

Reasons Why Insurance Premiums May Increase Annually

Insurance premiums are not static figures. They represent dynamic financial calculations that adapt to changing risk landscapes, economic conditions, and individual policyholder circumstances. Understanding the underlying reasons for annual premium increases can help you better manage your insurance expenses.

Below is a table outlining the main factors that lead to annual increases in insurance premiums, giving you a birds-eye view of how each aspect impacts your yearly costs.

| Factor | Description | Sample Impact |

|---|---|---|

| Inflation | General rise in prices, especially according to CPI | Adjustment to maintain cover value |

| Claims Paid Out | High total claims increase pressure on insurer finances | Possible premium recalibration |

| Change in Personal Risk Profile | Updates in health, driving record, or property risk | Higher risk can mean higher premiums |

| Economic Instability | Changes in national or international economy | Greater uncertainty forces pricing adjustments |

| Technological Advancements | Insurers using new data analytics and risk modelling | More accurate pricing for each individual |

| Regulatory and Policy Changes | Shifts in requirements from industry regulators | Insurers amend how premiums are set |

| Location-Based Risk Adjustments | Moving to or from high-risk areas | House or car premiums may shift notably |

External Economic Factors

External economic conditions play a significant role in driving insurance premium adjustments. Inflation, economic instability, and industry-wide trends contribute to annual premium increases:

- Rising repair and replacement costs

- Increased medical treatment expenses

- Broader economic inflationary pressures

Research from the Association for Savings and Investment South Africa indicates that insurers paid substantial claims in 2023, which necessitates periodic premium recalibration to maintain financial sustainability.

Individual Risk Profile Changes

Personal circumstances can dramatically impact your insurance premium. Insurers continuously reassess individual risk profiles based on recent events and behavioral patterns:

- Changes in personal health status

- Modifications to driving record

- Property location risk alterations

- Updated claims history

For example, a single traffic violation can trigger a premium increase, reflecting the insurer’s perception of heightened risk. Similarly, relocating to an area with higher crime rates might result in adjusted home insurance rates.

Technological and Industry Transformation

Technological advancements and industry shifts also contribute to premium adjustments. Modern risk assessment tools, enhanced data analytics, and evolving insurance models influence pricing strategies.

If you want to understand more about why car insurance rates change, our comprehensive guide offers deeper insights into these complex calculations.

Factors Influencing Annual Premium Changes

Annual insurance premium changes are complex calculations involving multiple interrelated factors. Understanding these nuanced elements helps policyholders comprehend why their insurance costs fluctuate and how insurers determine pricing strategies.

Risk Assessment and Predictive Modeling

Insurers utilize sophisticated statistical models to evaluate potential future risks. These advanced computational techniques analyze extensive datasets to predict potential claim probabilities:

- Historical loss patterns

- Statistical probability of specific events

- Geographic and demographic risk indicators

- Emerging technological and environmental trends

According to research analyzing South African general insurance firms, effective risk management practices are crucial for maintaining accurate premium pricing and overall financial sustainability.

Macroeconomic and Industry-Wide Influences

Broad economic conditions significantly impact insurance premium calculations. These external factors create ripple effects across the entire insurance ecosystem:

- National inflation rates

- Currency exchange rate fluctuations

- Overall economic stability

- Regulatory policy changes

- Global reinsurance market dynamics

Economic shifts can dramatically alter insurers’ risk calculations, necessitating periodic premium adjustments to maintain financial equilibrium.

Technological and Actuarial Innovations

Technological advancements are revolutionizing how insurers assess and price risk. Modern data analytics, artificial intelligence, and machine learning enable more precise risk evaluation:

- Enhanced predictive modeling capabilities

- Real-time risk assessment tools

- More granular individual risk profiling

- Improved claims prediction algorithms

If you want to review your insurance coverage annually, understanding these dynamic factors can help you make more informed decisions about your insurance portfolio.

The Impact of Claims History on Premium Rates

Your insurance claims history serves as a critical financial fingerprint that insurers meticulously analyze when determining your premium rates. This comprehensive record provides insurers with profound insights into your risk profile and potential future claim likelihood.

Understanding Claims History Evaluation

Insurers conduct an intricate assessment of your past insurance claims to predict future risk potential. This evaluation encompasses multiple dimensions of your insurance interaction:

- Frequency of previous claims

- Total monetary value of past claims

- Nature and severity of reported incidents

- Time elapsed since last claim

- Pattern of claim submissions

Research from the Association for Savings and Investment South Africa indicates significant industry challenges with fraudulent claims, which further emphasizes the importance of thorough claims history analysis.

Risk Classification and Premium Calculation

Your claims history directly influences your risk classification, which subsequently determines your premium rates. Insurers categorize policyholders into risk tiers based on their claims behavior:

- Low-risk tier: Minimal or no claims history

- Standard-risk tier: Average claim frequency

- High-risk tier: Frequent or substantial claims

Each tier corresponds to a specific premium range, with higher-risk classifications attracting more expensive insurance rates. A single significant claim can potentially shift your risk classification and increase your premium.

This table categorises how insurers use your claims history to classify risk and determine premiums, helping you see the link between past behaviour and future costs.

| Risk Tier | Claims Behaviour Description | Typical Premium Impact |

|---|---|---|

| Low-risk | Minimal or no prior claims | Lower premiums |

| Standard-risk | Average frequency and value of claims | Standard market rate premiums |

| High-risk | Frequent or high-value claims | Higher, sometimes substantially raised |

| Claims-free Bonus | Long periods without any claims | Can qualify for further discounting |

| Recent Large Claim | Significant single recent claim | Might trigger an immediate rate increase |

| Patterned Claims | Multiple small but consistent claims | May flag risk, lead to reduced benefits |

Long-Term Impact of Claims Behavior

Claims history is not just a snapshot but a longitudinal record that can have lasting consequences on your insurability. Insurers use advanced predictive models to extrapolate future risk based on historical patterns:

- Multiple small claims might indicate higher risk than one major claim

- Consistent claim-free periods can help reduce premium rates

- Certain types of claims carry more weight in risk assessment

If you want to understand the claims process better, our comprehensive guide provides valuable insights into navigating insurance claims effectively.

Understanding Market Trends and Their Effect on Premiums

Market trends are powerful forces that shape insurance premium calculations, creating a complex ecosystem of interconnected economic and industry-specific dynamics. These trends represent more than just numerical fluctuations they reflect broader economic narratives and risk landscape transformations.

Global and Local Economic Influences

Economic conditions play a pivotal role in determining insurance premium trajectories. Insurers must continuously adapt their pricing strategies to reflect broader economic shifts:

- National inflation rates

- Currency exchange rate fluctuations

- Unemployment levels

- Overall economic stability

- Investment market performance

Research from the Association for Savings and Investment South Africa reveals that insurers maintain robust financial buffers, enabling them to navigate complex market environments while managing premium adjustments.

Technological and Regulatory Disruptions

Technological advancements and regulatory changes fundamentally reshape insurance market dynamics. These transformative elements introduce new variables into premium calculation methodologies:

- Emergence of artificial intelligence in risk assessment

- Blockchain technology in claims processing

- Enhanced data analytics capabilities

- Stricter regulatory compliance requirements

- Digital transformation of insurance platforms

Each technological innovation provides insurers with more sophisticated tools for understanding and pricing risk, potentially leading to more nuanced premium structures.

Industry-Specific Risk Landscape

Industry trends specific to insurance create unique pressures that directly influence premium calculations. These specialized market dynamics require continuous adaptation:

- Increasing frequency of extreme weather events

- Changes in medical treatment costs

- Emerging cybersecurity risks

- Population demographic shifts

- Evolving consumer behavior patterns

If you want to explore strategies for reducing your insurance costs, our comprehensive guide offers practical insights into navigating these complex market trends.

Take Control of Your Annual Premium Increases with Personalised Solutions

Worried about why your insurance premiums keep rising each year? You are not alone. Many South Africans face higher costs due to shifting risk assessments, changes in claims history and broader market trends. If you want real answers about managing your premium or how claims and inflation can impact your budget, you deserve tailored support that understands the local insurance landscape.

At King Price, you get more than just basic coverage. Our team uses insights from your unique risk profile and changing needs to find ways to help you save on car, home or contents insurance. Ready for advice that turns uncertainty into savings? Redirect your journey now by visiting the King Price homepage to see your personalised options and get tips that put you back in charge. Do not wait for your next premium spike. Discover how the right plan can help you protect more and pay less. See all our insurance solutions today.

Frequently Asked Questions

Do insurance premiums always rise every year?

Insurance premiums can increase annually due to various factors, including inflation, changes in an individual’s risk profile, and external economic conditions.

What factors contribute to an increase in insurance premiums?

Insurance premiums may rise due to rising repair costs, medical expenses, changes in claims history, economic inflation, and adjustments in risk assessment by insurers.

How does my claims history affect my insurance premium?

Your claims history influences your risk classification, and insurers may increase your premium if you’ve made frequent or significant claims, reflecting a higher perceived risk.

Are there ways to keep my insurance premiums from rising?

You can potentially keep your premiums steady by maintaining a clean claims history, regularly reviewing your coverage, and making adjustments based on your current risk profile.