Figuring out how car insurance premiums are set can feel like guesswork, especially with so many factors at play. Here is something that will surprise you. Newer cars in South Africa can have up to 25 percent lower insurance premiums compared to older models, mainly due to advanced safety features and lower theft risk. That turns the usual thinking on its head. Sometimes paying extra upfront for a safer car actually means saving more on your monthly budget than you might expect.

Table of Contents

- Key Factors Affecting Your Premium

- How Insurers Assess Risk For Cars

- Ways To Lower Your Car Insurance Costs

- Frequently Asked Questions About Premiums

Quick Summary

| Takeaway | Explanation |

|---|---|

| Vehicle Characteristics Impact Premiums | Vehicle value, safety features, and age significantly influence insurance rates, with newer and safer vehicles generally offering lower premiums. |

| Driver Profiles Matter | Individual factors such as driving experience, claims history, and demographics play a crucial role in premium calculations, with less experienced and younger drivers typically facing higher costs. |

| Location Influences Costs | Geographic factors, including crime rates and urban living, can lead to varying premiums, with urban areas typically incurring higher rates due to increased risks. |

| Proactive Cost Reduction Strategies | Implementing strategies like policy bundling, installing security systems, and maintaining a clean driving record can help lower insurance costs effectively. |

| Understanding Premium Variability | Awareness of how changes in risk factors, vehicle type, and individual circumstances can affect premiums encourages informed decisions during policy renewals. |

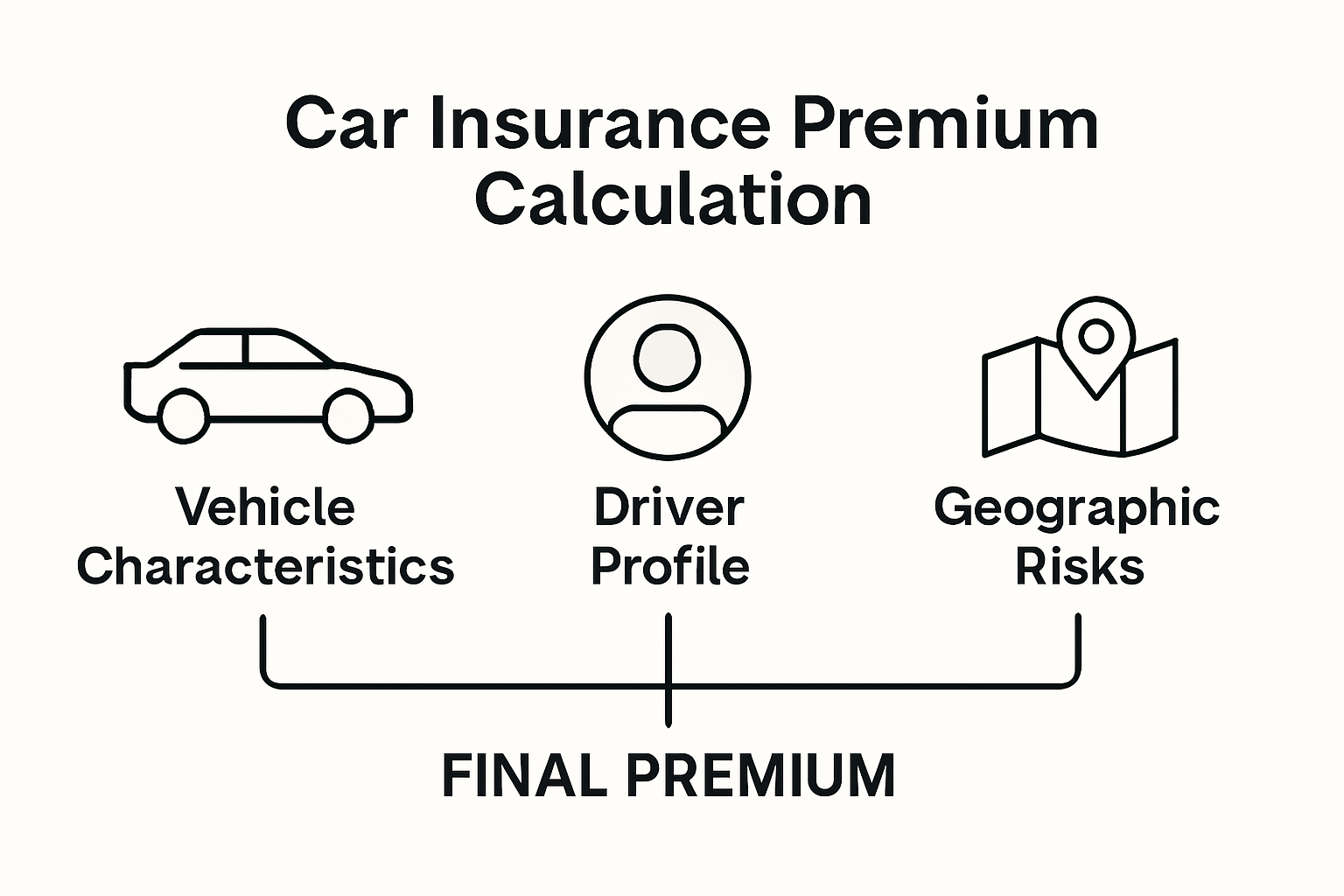

Key Factors Affecting Your Premium

Calculating car insurance premiums is a complex process involving multiple interconnected variables that insurers carefully evaluate to determine risk and appropriate pricing. Understanding these key factors can help you comprehend why your insurance costs are set at a specific rate and potentially identify opportunities for reducing your premiums.

Vehicle Characteristics and Risk Assessment

The specific details of your vehicle play a crucial role in premium calculations. Insurers conduct detailed assessments that go far beyond simple make and model considerations. Learn more about vehicle risk factors that impact your insurance costs.

According to research from FanNews, several vehicle-specific factors significantly influence premium pricing:

- Vehicle Value: Higher-value vehicles typically require more expensive comprehensive coverage and have higher repair or replacement costs.

- Safety Features: Modern vehicles with advanced safety technologies like anti-lock braking systems, lane departure warnings, and collision prevention systems may qualify for lower premiums.

- Age of Vehicle: Newer vehicles often have lower insurance rates due to superior safety features, while older vehicles might incur higher premiums due to increased maintenance and repair risks.

Personal Driver Profile and Risk Evaluation

Money Magazine highlights that individual driver characteristics are equally critical in premium calculations. Insurers conduct comprehensive risk assessments based on multiple personal factors:

- Driving Experience: Less experienced drivers typically face higher premiums due to statistically higher accident probabilities.

- Claims History: Drivers with previous insurance claims or traffic violations are considered higher-risk and may encounter increased premium rates.

- Age and Demographic Factors: Young drivers under 25 and senior drivers over 65 often experience higher insurance costs due to perceived increased driving risks.

Geographic and Environmental Risk Factors

Where you live and park your vehicle can substantially impact your insurance premium. FanNews research indicates that geographic considerations play a significant role in risk assessment:

- Urban vs Rural Areas: Densely populated urban regions typically have higher insurance premiums due to increased traffic congestion, higher accident rates, and greater theft risks.

- Crime Rates: Areas with elevated crime statistics may result in higher comprehensive coverage costs.

- Parking Conditions: Secure parking facilities, such as locked garages or monitored parking areas, can potentially reduce insurance premiums by minimizing theft and damage risks.

By understanding these intricate factors, drivers can make informed decisions about their vehicle choices, driving behaviors, and insurance selections. While some factors remain beyond individual control, awareness enables more strategic approaches to managing insurance costs.

Here is a table summarising the key factors affecting your car insurance premium in South Africa:

| Factor Type | Specific Factors | Impact on Premiums |

|---|---|---|

| Vehicle Characteristics | Vehicle Value, Safety Features, Age | Higher value/older cars can increase premiums; advanced safety features lower them |

| Driver Profile | Driving Experience, Claims History, Age | Young/inexperienced drivers and claims history raise premiums |

| Geographic/Environmental | Urban vs Rural, Crime Rates, Parking | Urban areas/higher crime raise premiums; secure parking can lower them |

How Insurers Assess Risk for Cars

Risk assessment is the cornerstone of how insurers determine car insurance premiums. This complex process involves sophisticated data analysis and predictive modeling to evaluate the potential financial risk associated with insuring a specific vehicle and driver. Explore the fundamentals of car insurance risk assessment to understand how insurers make these critical decisions.

Statistical Modeling and Data Analysis

Insurers employ advanced statistical techniques to quantify and predict potential risks. According to research from actuarial science experts, the process involves multiple layers of data evaluation:

- Predictive Analytics: Sophisticated algorithms analyze historical claims data, identifying patterns and correlations that help predict future risk probabilities.

- Comprehensive Risk Profiling: Each vehicle and driver receives a comprehensive risk score based on multiple interconnected factors.

- Machine Learning Techniques: Advanced computational models continuously refine risk assessment methods by learning from new data and emerging trends.

Vehicle-Specific Risk Evaluation

Insurance industry reports reveal that vehicles themselves are subject to detailed risk assessments. Insurers meticulously examine several key characteristics:

- Repair and Replacement Costs: The potential expense of repairing or replacing a specific vehicle model significantly impacts its risk profile.

- Safety Ratings: Vehicles with higher safety ratings and advanced safety technologies are typically considered lower-risk.

- Theft Vulnerability: Some vehicle models are more prone to theft, which increases their overall risk assessment.

Driver Behavior and Technological Monitoring

Modern risk assessment has evolved beyond traditional demographic evaluations. Technological innovations now enable more precise risk monitoring:

- Telematics Devices: Advanced tracking devices can monitor driving behavior in real-time, providing insurers with precise data about individual driving patterns.

- Usage-Based Insurance: Some insurers now offer policies that dynamically adjust premiums based on actual driving behavior and risk exposure.

- Digital Risk Profiling: Comprehensive digital profiles help insurers create more personalized and accurate risk assessments.

The risk assessment process is a continuous evolution of data analysis, technological innovation, and predictive modeling. By understanding these intricate evaluation methods, drivers can better comprehend how insurers determine their premiums and potentially take steps to reduce their perceived risk.

Ultimately, insurers aim to create a fair and sustainable pricing model that accurately reflects the potential risk associated with insuring a specific vehicle and driver. This approach protects both the insurance provider and the policyholder by ensuring more precise and equitable premium calculations.

Ways to Lower Your Car Insurance Costs

Reducing car insurance costs requires strategic planning and proactive approaches. Car owners can implement multiple tactics to potentially decrease their premium expenses without compromising essential coverage. Discover smart strategies for insurance savings to manage your insurance budget effectively.

Here is a table outlining actionable strategies to lower your car insurance premiums and their corresponding potential impacts:

| Strategy | Description | Potential Impact |

|---|---|---|

| Policy Bundling | Combine multiple policies with one provider | Up to 25% discount, lower premiums |

| Increase Voluntary Excess | Opt for a higher excess to lower monthly payments | Reduced monthly premiums, higher out-of-pocket if claiming |

| Enhanced Security Systems | Install tracking devices, alarms, anti-jamming tech | Can qualify for premium reductions |

| Secure Parking | Use locked garages or monitored areas | Lowers theft/damage risk and premiums |

| Maintain Clean Driving Record | Avoid violations and at-fault accidents | Can result in significant savings |

| Take Defensive Driving Course | Complete certified defensive driving programmes | May qualify for lower premiums |

| Annual Policy Review | Revisit coverage every year | Ensures optimal, non-overpriced cover |

Strategic Policy Management

According to IOL financial advice, smart policy management can significantly impact insurance costs:

- Policy Bundling: Combining multiple insurance policies with a single provider can yield substantial discounts, potentially reducing premiums by up to 25%.

- Adjust Excess Levels: Increasing your voluntary excess can lower monthly premium payments, though it’s crucial to select an amount you can comfortably afford during a claim.

- Annual Policy Review: Regularly reassessing your coverage ensures you’re not overpaying for unnecessary protections.

Vehicle Security and Risk Reduction

King Price insurance blog highlights several vehicle-related strategies for reducing insurance costs:

- Enhanced Security Systems: Installing advanced tracking devices, anti-jamming technologies, and comprehensive alarm systems can demonstrate reduced theft risk.

- Parking Considerations: Secure parking in locked garages or monitored areas can potentially lower insurance premiums.

- Regular Vehicle Maintenance: Keeping your vehicle in excellent condition reduces the likelihood of mechanical failures and potential claims.

Personal Risk Management

Drivers can actively manage their personal risk profile to influence insurance pricing. Research from insurance experts suggests several effective approaches:

- Clean Driving Record: Maintaining a history without traffic violations or accidents can significantly reduce premium costs.

- Defensive Driving Courses: Completing certified defensive driving programs can demonstrate lower risk to insurers.

- Usage-Based Insurance: Consider telematics-based policies that reward safe driving behaviors with reduced premiums.

Insurers continuously evolve their risk assessment methodologies, making it essential for drivers to stay informed and proactive. By understanding and implementing these strategies, car owners can potentially achieve meaningful savings on their insurance expenses.

Remember that while cost reduction is important, maintaining adequate coverage remains crucial. Always balance potential savings with comprehensive protection that meets your specific needs and provides financial security in unexpected situations.

Frequently Asked Questions About Premiums

Navigation through the complex world of car insurance premiums can be challenging for many drivers. Understanding the most common questions helps demystify the process and empowers consumers to make informed decisions. Explore essential car insurance insights to gain comprehensive knowledge about premium calculations.

Understanding Premium Calculation Basics

According to FanNews insurance research, drivers frequently seek clarity on how premiums are determined:

- Why do premiums vary so much?: Each vehicle and driver represents a unique risk profile, with factors like age, driving history, vehicle type, and location significantly influencing pricing.

- Can my premium change during my policy period?: Typically, premiums remain stable during a policy term, but annual renewals may reflect changes in risk assessment.

- How often should I review my insurance policy?: Experts recommend an annual review to ensure your coverage remains appropriate and competitively priced.

Common Premium Calculation Misconceptions

Insurance industry experts highlight several persistent misconceptions about car insurance premiums:

- Myth: Older cars always cost less to insure: While older vehicles might have lower replacement values, they can sometimes incur higher premiums due to increased maintenance risks and fewer safety features.

- Myth: Color affects insurance rates: Despite popular belief, a vehicle’s color does not directly impact insurance premiums. Risk assessment focuses on technical specifications and historical data.

- Myth: Personal credit score does not matter: In many regions, credit scores can influence insurance pricing, reflecting potential financial responsibility.

Here is a table debunking some of the most common misconceptions about car insurance premiums:

| Misconception | Reality |

|---|---|

| Older cars are always cheaper to insure | Can sometimes have higher premiums due to higher maintenance risks and lack of safety features |

| Vehicle colour affects insurance rate | Colour has no direct effect; assessments are based on specs and history |

| Credit score does not matter | Credit score can impact premium pricing in many regions |

Strategic Premium Management

Drivers seeking to optimize their insurance costs should consider several strategic approaches:

- Comprehensive vs Third Party Coverage: Understanding the difference helps in selecting appropriate coverage that balances protection and affordability.

- Impact of Additional Security Measures: Installing tracking devices, immobilizers, and parking in secure locations can potentially reduce premium costs.

- Voluntary Excess Considerations: Choosing a higher voluntary excess can lower monthly premiums, but requires careful financial planning.

Navigating car insurance premiums requires ongoing education and proactive management. While the calculation process might seem complex, understanding the fundamental principles empowers drivers to make informed choices.

Remember that insurance is ultimately about financial protection. The lowest premium is not always the best option if it compromises essential coverage. Always prioritize comprehensive protection that meets your specific needs and provides peace of mind in unexpected situations.

Frequently Asked Questions

What factors influence my car insurance premium in South Africa?

Vehicle characteristics, such as make, model, age, safety features, as well as your personal driver profile, including experience and claims history, and geographic factors like location and crime rates all play significant roles in determining your car insurance premium.

Can I lower my car insurance premium?

Yes, you can lower your premium by implementing strategies like bundling policies, increasing your voluntary excess, enhancing vehicle security, maintaining a clean driving record, and regularly reviewing your insurance coverage for competitive pricing.

Why do newer cars have lower insurance premiums?

Newer cars often come with advanced safety features and lower theft risks, which reduce the overall risk for insurers, resulting in lower premiums compared to older models, which may lack these safety technologies.

How often should I review my car insurance policy?

It is advisable to review your car insurance policy annually to ensure you have optimal coverage and to take advantage of any potential savings as your risk profile and market conditions may change over time.

Take Control of Your Car Premium in 2025

Confused about how your car insurance premium is really calculated? You are not alone. Many South Africans often feel at a disadvantage when faced with rising costs and unclear risk assessments. Trying to keep your premium down can feel overwhelming, especially with all the personal, regional and vehicle-related factors influencing your price. The strategies outlined in this article show you how understanding your risk profile and proactive management can lead to real savings.

Ready to move from confusion to confidence? Discover simple, local solutions tailored for South Africans by visiting King Price Insurance. You will get hands-on advice and smarter cover options for every vehicle, plus tips to immediately start lowering your premium. Want more practical ways to save? Get all the details you need and start securing a better deal for your car in 2025 today on King Price Insurance.

Recommended

- Car Insurance Basics 2025: Simple Guide for SA Drivers – Savvy Insurance

- Saving Money on Car Insurance: Top Tips for 2025 – Savvy Insurance

- What Is Car Insurance? A Simple Guide for 2025 – Savvy Insurance

- Top Tips for Cheaper Car Insurance in South Africa 2025 – Savvy Insurance

- Top Car Insurance Tips South Africa 2025: Save and Stay Covered – Savvy Insurance

- Top Tips for Cheaper Car Insurance in South Africa 2025

4 Responses