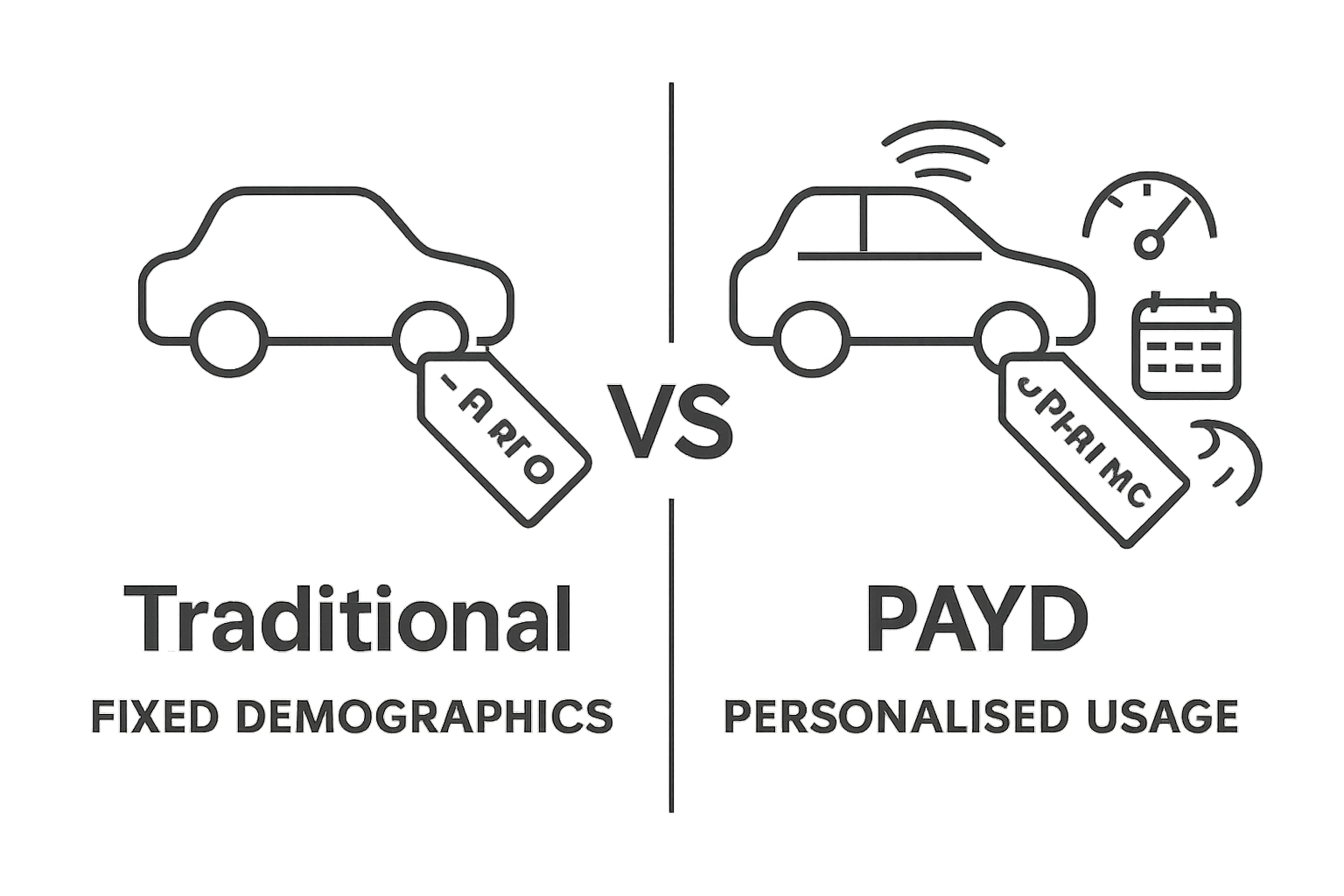

Pay As You Drive insurance is popping up everywhere and people are starting to question if old-school car insurance still makes sense. Now here is the wild stat. Drivers using PAYD models can save up to 30 percent compared to traditional insurance premiums. That sounds like a win already, right? But what really shakes things up is how this insurance model looks beyond age and job title. Instead, it puts your own driving on the stage and rewards you in ways that might surprise most South Africans.

Table of Contents

- What Is Pay As You Drive Insurance?

- Why Does Pay As You Drive Insurance Matter?

- Key Concepts Of Pay As You Drive Insurance

- Real-World Applications And Examples

Quick Summary

| Takeaway | Explanation |

|---|---|

| Lower premiums for safe drivers | PAYD insurance rewards safe driving behaviour with reduced insurance costs for conscientious drivers. |

| Cost savings for low-mileage drivers | Individuals who drive less frequently can significantly lower their insurance premiums through usage-based pricing. |

| Real-time driving behaviour tracking | Telematics technology allows insurers to monitor individual driving habits and adjust premiums accordingly. |

| Incentives for responsible driving | The PAYD model encourages safer driving practices as insurance costs directly reflect personal driving behaviour. |

| Transparent and personalised pricing | PAYD insurance provides a clear understanding of how premiums are calculated based on specific driving metrics. |

What is Pay As You Drive Insurance?

Pay As You Drive (PAYD) insurance represents a revolutionary approach to car insurance that transforms how premiums are calculated by tracking actual vehicle usage. Unlike traditional insurance models where rates are determined through broad demographic factors, this innovative model uses precise technological measurements to create personalised insurance pricing.

Understanding the Core Concept

Telematics technology enables insurers to monitor real driving behaviour and mileage, allowing for more accurate risk assessment. The fundamental principle is simple: the less you drive and the more safely you drive, the lower your insurance premium.

Key characteristics of Pay As You Drive insurance include:

- Direct correlation between driving habits and insurance costs

- Usage-based pricing model

- Real-time tracking of vehicle movement and driver behaviour

- Potential significant cost savings for low-mileage and safe drivers

How PAYD Insurance Works

Insurers typically implement PAYD insurance through telematics devices installed in vehicles or smartphone applications that track:

- Total kilometres driven

- Time of day driving occurs

- Driving speed and acceleration patterns

- Braking intensity and consistency

- Location and route characteristics

According to research from the Public Library of Science, these advanced monitoring systems provide insurers with unprecedented insights into individual driving risks. By collecting granular data, insurance companies can offer more precise and fair pricing strategies that reward responsible driving behaviour.

This innovative insurance approach benefits both insurers and policyholders by creating a more transparent, data-driven model that incentivizes safer driving and provides more personalised insurance experiences.

Below is a table summarising the main features and characteristics that distinguish Pay As You Drive (PAYD) insurance from traditional car insurance, as highlighted in the article.

| Feature | Pay As You Drive (PAYD) Insurance | Traditional Car Insurance |

|---|---|---|

| Premium Calculation Basis | Based on actual driving behaviour and distance driven | Based on demographic factors (age, occupation, etc.) |

| Technology Required | Utilises telematics devices or smartphone apps | None required (generally paper-based or online forms) |

| Data Collection | Real-time tracking of speed, braking, mileage, time of day, and routes | Little to no driving data collected |

| Pricing Transparency | Transparent link between driving habits and premium | Less transparent, relies on statistical averages |

| Driver Incentives | Rewards safe and low-mileage drivers with reduced premiums | Few or no direct incentives for safer driving |

| Environmental/Safety Impacts | Encourages reduced road use and safer driving, lowering accidents/emissions | No direct impact on individual behaviour |

| Adjustment Frequency | Premiums can be adjusted frequently based on ongoing driving data | Typically adjusted only at renewal or upon claim |

Why Does Pay As You Drive Insurance Matter?

Pay As You Drive (PAYD) insurance matters because it represents a fundamental shift in how car insurance is perceived and priced, offering significant advantages for both consumers and insurance providers. This innovative approach addresses long-standing inefficiencies in traditional insurance models by creating a more transparent, fair, and personalised pricing mechanism.

Financial Benefits for Drivers

Understanding drivers license and insurance becomes more nuanced with PAYD insurance. The model provides tangible financial incentives for responsible driving behaviour. Drivers who travel less frequently or demonstrate safer driving habits can significantly reduce their insurance costs, making car ownership more affordable.

Key financial advantages include:

- Potential premium reductions for low-mileage drivers

- Direct correlation between driving behaviour and insurance costs

- Transparent pricing mechanism

- Opportunity for cost savings through responsible driving

Environmental and Safety Implications

According to research from the Public Library of Science, PAYD insurance offers broader societal benefits beyond individual cost savings. By incentivising safer and more mindful driving, these insurance models contribute to reduced road traffic injuries and decreased vehicle emissions.

The environmental and safety impact includes:

- Encouragement of more responsible driving behaviour

- Potential reduction in overall road accidents

- Lower carbon emissions through reduced unnecessary driving

- Enhanced awareness of personal driving patterns

Moreover, PAYD insurance empowers drivers with greater understanding of their driving habits. The data collected through telematics devices provides insights that can help individuals improve their driving skills, potentially leading to long-term safety improvements and more conscious transportation choices.

How Pay As You Drive Insurance Works

Pay As You Drive (PAYD) insurance operates through sophisticated technological systems that transform traditional insurance approaches by precisely tracking individual driving behaviour. This innovative model utilises advanced telematics technology to create a dynamic and personalised insurance experience.

Technological Infrastructure

How car premiums are calculated becomes significantly more sophisticated with PAYD insurance. Insurers implement this system through two primary technological mechanisms:

- Dedicated telematics devices installed directly in vehicles

- Smartphone applications that track driving metrics

These technological tools collect comprehensive data about driving patterns, enabling insurers to develop highly customised risk assessments. The tracking systems monitor multiple critical parameters that collectively determine insurance pricing.

Data Collection and Risk Assessment

According to research from transportation risk management experts, the core data points collected typically include:

- Total kilometres driven per month

- Time of day and specific driving routes

- Acceleration and braking patterns

- Average driving speed

- Frequency of hard braking or sudden acceleration

By analysing these detailed metrics, insurers can create more accurate risk profiles for individual drivers. This granular approach allows for pricing that directly reflects actual driving behaviour rather than relying on broad demographic assumptions.

Premium Calculation Mechanism

The final premium calculation involves a complex algorithm that weighs various factors. Safer, less frequent drivers receive lower premiums, while those demonstrating higher-risk driving characteristics might face adjusted rates. This system incentivises responsible driving by directly linking insurance costs to individual performance, creating a transparent and fair pricing model that benefits conscientious drivers.

The following table outlines the key technological, data, and pricing components of PAYD insurance, making it easier to understand how these elements fit together in practice.

| Component | Description |

|---|---|

| Telematics Technology | Devices or apps that track real-time driving data (e.g. speed, mileage) |

| Data Points Collected | Kilometres driven, time of day, speed, braking, routes |

| Risk Assessment | Uses driving data for individual risk profiling |

| Premium Calculation Algorithm | Adjusts costs based on behaviour; safer/low-mileage = lower premium |

| Driver Feedback | Provides insights for drivers to improve habits and reduce risks |

| Personalisation Level | Highly tailored premiums reflecting actual driver behaviour |

Key Concepts of Pay As You Drive Insurance

Pay As You Drive (PAYD) insurance introduces several groundbreaking concepts that fundamentally transform traditional insurance models. Understanding these key principles helps drivers appreciate the nuanced approach this innovative insurance strategy offers.

Personalised Risk Assessment

Top tips for cheaper car insurance become more sophisticated with PAYD insurance. The core concept revolves around creating individualised risk profiles based on actual driving behaviour rather than generalised demographic predictions.

Key elements of personalised risk assessment include:

- Dynamic pricing based on real-time driving data

- Granular evaluation of individual driving patterns

- Continuous monitoring of risk factors

- Immediate feedback on driving performance

Behavioural Incentive Mechanisms

According to transportation safety research, PAYD insurance fundamentally transforms driver motivation by directly linking insurance costs to personal driving habits. This approach creates a powerful incentive structure that encourages safer and more responsible driving.

Critical behavioural incentive components involve:

- Financial rewards for low-risk driving behaviour

- Transparent cost-performance relationship

- Real-time performance tracking

- Potential premium reductions for consistent safe driving

Technology-Driven Insurance Model

The technological infrastructure underpinning PAYD insurance represents a paradigm shift in how insurance risk is calculated and managed. By leveraging advanced telematics and data analytics, insurers can develop more accurate, fair, and responsive insurance products that adapt to individual driver characteristics.

This technology-driven approach ensures that insurance becomes a more dynamic, interactive, and personalised service, moving beyond the traditional one-size-fits-all insurance models of the past.

Real-World Applications and Examples

Pay As You Drive (PAYD) insurance has transitioned from a theoretical concept to a practical reality, with numerous innovative implementations demonstrating its effectiveness across different driving contexts and user profiles. These real-world examples showcase the versatility and potential of this transformative insurance approach.

Personal Vehicle Usage

Best youth driver insurance tips become particularly relevant when exploring PAYD applications. Individual drivers can benefit significantly from tailored insurance models that reward responsible driving habits.

Typical personal vehicle applications include:

- Commuters with predictable, low-mileage driving patterns

- Young drivers seeking to demonstrate safe driving skills

- Professionals working from home with minimal vehicle usage

- Retirees with limited weekly driving distances

Commercial and Fleet Management

According to transportation sector research, PAYD insurance has emerged as a game-changing tool for businesses managing vehicle fleets. Companies can leverage detailed driving data to optimize operational costs and enhance driver safety.

Commercial fleet applications encompass:

- Tracking and reducing fuel consumption

- Monitoring driver performance and safety metrics

- Implementing targeted driver training programs

- Reducing overall insurance expenditure

Specialized Sector Implementations

Beyond personal and commercial applications, PAYD insurance demonstrates remarkable adaptability across specialized sectors. Ride-sharing platforms, delivery services, and transportation companies are increasingly adopting these data-driven insurance models to create more efficient and transparent risk management strategies.

The continuous evolution of PAYD insurance suggests a future where insurance becomes increasingly personalized, fair, and directly linked to individual driving behavior, benefiting both insurers and policyholders through improved risk assessment and incentive mechanisms.

Transform How You Insure Your Drive in South Africa

You are learning how Pay As You Drive insurance can make car cover fairer and more affordable, especially if you drive less or value safer roads. But making sense of personalised risk assessments and finding a policy that truly fits your lifestyle can feel overwhelming. If you want pricing that rewards your real driving habits and usage, traditional insurance might be leaving you paying too much or not recognising your efforts to drive safely.

It is time to take control of your own risk profile. Visit King Price Insurance now to see how you can get a quote tailored to how you actually drive, not how the averages drive. We understand the unique needs of South African drivers seeking savings, safety, and flexibility. Looking for more smart insurance tips? Browse our expert advice on car insurance and discover practical ways to lower premiums while enjoying total peace of mind. Make your next move today and drive your insurance costs down.

Frequently Asked Questions

What is Pay As You Drive insurance?

Pay As You Drive (PAYD) insurance is a type of car insurance that calculates premiums based on actual vehicle usage and driving behaviour, rather than relying solely on demographic factors.

How does Pay As You Drive insurance work?

PAYD insurance operates using telematics technology to track driving metrics, such as distance driven, speed, acceleration, and braking patterns. This data is then used to assess risk and determine premium pricing.

What are the benefits of Pay As You Drive insurance for drivers?

The key benefits include potential cost savings for low-mileage drivers, a transparent pricing model, and rewards for safe driving habits. It encourages responsible driving and can lead to reduced insurance premiums.

How is the premium calculated in Pay As You Drive insurance?

Premiums in PAYD insurance are calculated using a complex algorithm that considers various driving behaviour metrics collected through telematics, rewarding safer, lower-risk drivers with lower rates.

Recommended

- Best Youth Driver Insurance Tips for 2025: Save and Stay Safe – Savvy Insurance

- Car Insurance Basics 2025: Simple Guide for SA Drivers – Savvy Insurance

- Car Insurance Terms Guide 2025: Simple Tips for SA Drivers – Savvy Insurance

- How Car Premiums Are Calculated in 2025: Simple Guide – Savvy Insurance